When a customer defaults on payment for goods or services provided on credit, your business’s cash flow can be disrupted. Trade credit insurance (TCI) helps protect businesses by covering losses from customer insolvency or non-payment. If you’re filing a claim, here’s what you need to know:

- What TCI Covers: Typically, TCI covers 80%-95% of unpaid debts due to insolvency or protracted default.

- Claims Process: Notify your insurer promptly (usually within 30-60 days of a missed payment). Gather key documents like invoices, contracts, and proof of delivery to support your claim.

- Deadlines: For non-payment, claims must be filed within 3-6 months of the due date. For insolvency, you often have just 30 days to file.

- Settlement Timelines: Protracted default claims can take 5-9 months from the invoice due date to payment. Insolvency claims are typically resolved within 1-2 months.

Preparation and timely action are critical. Ensure your documentation is complete and undisputed, adhere to policy timelines, and stop shipments to delinquent customers. By maintaining proper records and working closely with your insurer, you can protect your cash flow and minimize risks.

Preparing to File a Trade Credit Claim

If you’re dealing with a potential non-payment situation, time is of the essence. Start by gathering all the necessary documents – like invoices, signed contracts, and proof of delivery – to back up your claim. Then, carefully review what’s required to ensure you can clearly demonstrate your loss.

Required Documentation

Having the right paperwork is essential for a smooth claims process.

Collect all evidence of the transaction, including invoices, purchase orders, contracts, promissory notes, or bills payable, which outline the terms of sale and repayment. Add proof of performance, such as shipping logs, delivery receipts, or records showing the service was completed, to confirm that the conditions triggering your policy have been met.

Also, keep a record of your collection efforts. Save emails, letters, and call logs that document your attempts to recover the debt. An updated accounts receivable ledger is also key – it should clearly show the unpaid balance, including any partial payments or proceeds you’ve already received.

Establishing Proof of Loss

Calculating your loss accurately is critical – it not only supports your claim but also helps speed up the assessment process.

To calculate your loss, go beyond the total invoice amount. Focus on the net price, which is the invoice amount minus any trade discounts provided. For example, if you made $50,000 in sales but offered a 10% discount, your net loss would be $45,000. Most insurers cover 75% to 95% of this net loss, after deducting any applicable policy deductible. Be sure that the loss doesn’t exceed the buyer’s approved credit limit.

Before submitting your claim, confirm that the debt is legitimate and undisputed. Any disagreements with the buyer – whether about the amount owed or the quality of goods delivered – should be resolved beforehand, as insurers typically require these issues to be settled first. Organize all your documentation in chronological order, making sure it aligns with your policy’s specific terms, including any agreed-upon credit periods. Proper preparation like this ensures your claim is complete and reduces the risk of delays.

Once you have all the required documents and your loss is calculated, you’ll be ready to move on to filing your claim.

sbb-itb-2d170b0

Submitting the Trade Credit Claim

Once you’ve calculated your loss and gathered the necessary documents, it’s crucial to notify your insurer without delay. You need to inform them as soon as you’re aware of a potential default or customer insolvency. Typically, you must notify your insurer within 30–60 days of the payment due date. For non-payment cases, claims must be filed within 3–6 months, while insolvency cases require filing within 30 days. Missing these deadlines can lead to a denied claim, as delays might hinder the insurer’s ability to recover the debt. After notifying your insurer, make sure to submit your claim with complete and accurate information.

Filing a Complete Claim

A complete claim includes all required forms and supporting documentation submitted together. These documents often include unpaid invoices, signed sales contracts, proof of delivery, communication records with the customer, and evidence of your attempts to collect the debt. Double-check that your invoices match your ledger and shipping documents – errors can cause delays in processing.

"The business must provide detailed documentation of the debt, including invoices, contracts, and communication with the customer." – Freeths

It’s also critical that the debt is undisputed. Claims should only be submitted when there are no disputes over the debt. Familiarize yourself with your policy’s specific requirements, like deductibles, coverage limits, and exclusions, to ensure your claim meets all conditions. Finally, follow the claim submission timelines outlined in your policy.

Claim Submission Timelines

Timing is everything when it comes to filing your claim. For non-payment cases without insolvency, your claim must be filed within 3–6 months of the original due date. If your buyer is declared insolvent, you have only 30 days from the insolvency event to file. Missing these deadlines is a common reason claims are denied.

"Failure to report an overdue account or file a claim within the specified policy timelines is one of the most common reasons for claim denial." – Trade Treasury Payments

To avoid missing deadlines, consider setting up automated alerts for 30- and 60-day overdue marks. These reminders can help you meet the "Notification of Overdue" requirements and protect you from uninsured exposure. Keep in mind that most policies stop covering new shipments once a buyer is a certain number of days overdue, so staying on top of these thresholds is essential to minimize risk.

Claims Assessment and Evaluation Process

Once you submit a claim, insurers carefully review it against the policy’s criteria and the documentation you’ve provided.

How Insurers Evaluate Claims

Insurers follow specific steps to determine if your claim meets their requirements. First, they confirm a direct trade transaction took place – essentially, verifying that you delivered goods or services as agreed. Claims must also fall within the approved credit limit. For discretionary limits, insurers check if you’ve followed policy rules, like obtaining a recent credit report or showing a positive payment history.

The type of loss must align with a covered risk. Common risks include insolvency (e.g., bankruptcy), protracted default (failure to pay within a set period after the due date), or political risks like currency restrictions or government intervention. Additionally, the debt must be undisputed – if your buyer raises a valid complaint about product quality or delivery, the claim will be paused until the issue is resolved.

"A trade credit insured risk is always directly related to an underlying trade transaction, which is either the delivery of goods or of services. The correct fulfilment of this trade transaction is essential for trade credit cover to exist." – ICISA

Adjusters then examine supporting documents, such as invoices, shipping records, and account statements, to confirm delivery and validate the outstanding balance. They also check whether you took steps to minimize potential losses. For example, continuing to ship goods despite knowing your buyer was in financial trouble could jeopardize your claim. Any irregularities during this review may lead to claim denial.

Common Reasons for Claim Denials

Certain pitfalls can frequently result in claim denials. One major issue is insufficient shipping documentation. Insurers often require third-party verification, like a bill of lading from an independent carrier, rather than internal records. Inconsistent buyer details across invoices, bills of lading, and purchase orders is another red flag that can invalidate a claim.

"While uncommon, claim denials can occur for a variety of reasons… including inadequate shipping documents, inconsistent buyer names on the face of the buyer obligation documents… and failure to file a claim on time." – EXIM’s Claims Processing Division

Missing filing deadlines is another common issue. For instance, if your buyer files for bankruptcy, you might have only 30 days to submit your claim. To avoid these issues, always use third-party documents to prove delivery, ensure consistency in buyer information across all paperwork, and set up alerts to track overdue invoices nearing critical deadlines.

Specialized support services can help businesses navigate these challenges effectively.

Role of Accounts Receivable Insurance in Claims Management

Accounts Receivable Insurance (ARI) helps businesses tackle the complexities of claims management with expert guidance. ARI offers pre-claim support, helping address potential problems before they escalate into formal claims. This early intervention can resolve disputes and ensure policy compliance.

ARI also provides detailed policy guidance, helping you understand your credit limits, reporting deadlines, and other key terms. Their brokers assist with preparing documentation and submitting claims, ensuring accuracy and completeness. By working with a global network of credit insurance carriers, ARI can speed up claim processing and share best practices for maintaining claim eligibility. This hands-on approach is particularly helpful for businesses managing both domestic and international accounts receivable, where varying documentation and deadlines can complicate the process.

Resolution and Payment of Claims

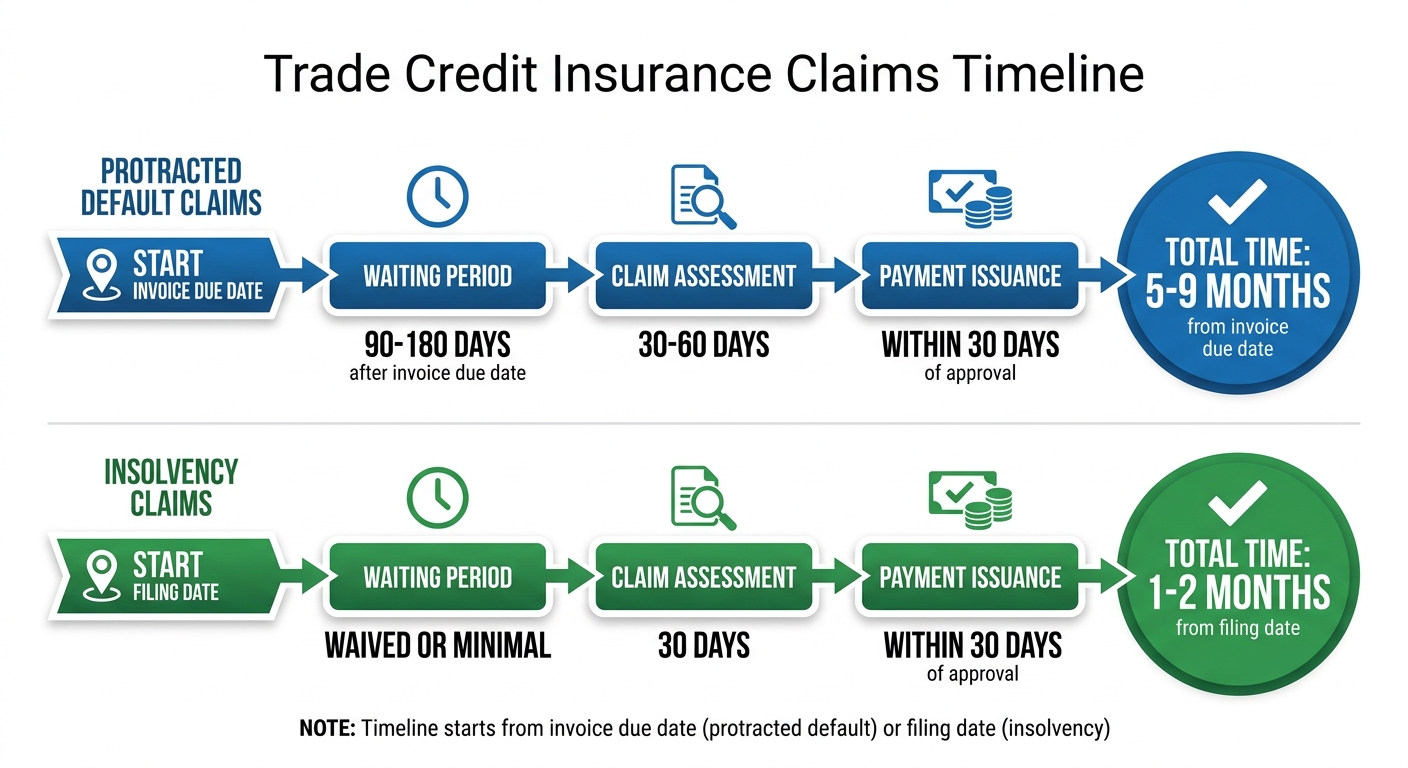

Trade Credit Insurance Claims Timeline: Protracted Default vs Insolvency

Once your claim has been evaluated, the insurer moves forward with settling it. This stage naturally follows the detailed assessment process we discussed earlier. Understanding the timelines involved can help you plan your finances and reduce potential disputes.

Claim Settlement and Payment Timelines

The time it takes to settle a claim depends on the type of loss. For protracted default claims, where a buyer fails to pay, there’s usually a waiting period of 90 to 180 days after the invoice due date before you can even file a claim. Once you submit the required documentation, insurers generally take 30–60 days to assess the claim and issue payment within 30 days of approval. From the invoice due date to receiving the payment, the process typically spans 5 to 9 months.

In insolvency cases, the timeline is shorter. If a buyer declares formal bankruptcy, the waiting period is often waived. You can file your claim as soon as you provide legal proof of insolvency. These claims are usually resolved within 30 days, meaning the entire process – from filing to payment – can be completed in just 1 to 2 months.

| Stage of Process | Timeline (Protracted Default) | Timeline (Insolvency) |

|---|---|---|

| Waiting Period | 90–180 days | Waived or minimal |

| Claim Assessment | 30–60 days | 30 days |

| Payment Issuance | Within 30 days of approval | Within 30 days of approval |

| Total Estimated Time | 5–9 months from due date | 1–2 months from filing |

To help speed up the process, submit all necessary documentation upfront. This includes invoices, delivery records, account statements, and any communication with the debtor. Providing a detailed system-generated debtors ledger in Excel format, listing individual transactions, invoice dates, and credit notes, can also make it easier for insurers to review your claim. With complete documentation, insurers may notify you of the payment amount within 30 days.

Appeals and Dispute Resolution

If your claim doesn’t go as planned, the first step is to carefully review the denial letter to identify the exact reason. Common reasons for denial include late filing, failure to disclose prior defaults, or continuing to ship to customers with overdue payments [13, 14]. If you haven’t received a written explanation of benefits, request one. Then, gather your insurance policy, proof of loss, and any relevant correspondence to support your case.

Write a formal appeal letter that includes your policy and claim numbers, a clear request for a reversal, and references to the specific policy language that supports your claim. Submit this appeal through the insurer’s preferred method – whether by mail, fax, or online – while ensuring you meet the deadlines outlined in your policy. Keeping a detailed communication log with dates, names, and confirmation of receipt is also a good practice.

"When insurance says ‘no,’ that doesn’t mean the fight is over. In fact, it’s often just the beginning." – American College of Rheumatology

Interestingly, while fewer than 1% of denied claims are appealed, over half of those appeals succeed. If an internal appeal doesn’t work, you can request a peer-to-peer review, file a complaint with your state insurance commissioner, or consult legal counsel, especially for higher-value claims.

Conclusion

Every step of the claims process reflects the core principles of effective risk management. Successfully managing trade credit claims requires careful preparation, precise execution, and strong collaboration. This isn’t just about best practices – it’s about meeting contractual obligations. You need to stick to notification deadlines, maintain detailed documentation (like signed delivery notes and invoices), and immediately stop shipments to delinquent debtors. Failing to do so could jeopardize your coverage entirely.

Knowing the distinction between insolvency and protracted default is another critical piece of the puzzle. Insolvency claims are often resolved quickly after the debt is verified. On the other hand, claims stemming from protracted default usually involve a waiting period of 3 to 6 months. During this time, insurers use their resources and expertise to pursue outstanding debts and validate claims.

Keeping a claim-ready file is essential. Many policies provide high indemnity levels, but only if you have the right documentation in place. This includes maintaining digital copies of delivery proofs and signed contracts for key customers, monitoring aging reports weekly to catch potential issues early, and ensuring that credit limits were active at the time of sale. Without proper credit limits, claims won’t be honored. These details can make the difference between a smooth claim process and a denied one.

Partnering with a reliable insurance provider can transform the claims experience. As Trade Treasury Payments aptly puts it, "The claim is the ‘moment of truth’ for any insurance policy". Accounts Receivable Insurance offers valuable support, including specialized claims management, access to a global network of credit insurers, and expertise in debt collection and legal matters. They also handle post-claim recovery efforts, such as subrogation, which can help recover additional funds and reduce uninsured losses.

The bottom line: treat claims management as an ongoing discipline. Stick to deadlines, keep thorough records, halt credit for overdue accounts, and work closely with your insurer at every step. With proper preparation and a dependable insurance partner, trade credit insurance becomes a powerful tool for safeguarding cash flow and managing risk effectively.

FAQs

What should I do first when a customer misses a payment?

The first thing to do is figure out why the customer missed their payment. It could be due to financial struggles, a misunderstanding, or even an administrative mistake. Understanding the cause helps you assess whether the problem is short-term or if it’s time to involve your trade credit insurance provider by filing a formal claim.

How do I calculate my claim amount after discounts and deductibles?

To figure out your claim amount, begin with the original invoice total owed by the buyer. Take away any discounts that were applied, then subtract the deductible outlined in your policy. After that, account for any recoveries or partial payments you’ve already received. For the most precise calculation, it’s a good idea to review your policy and reach out to your insurer or claims adjuster if you need further clarification.

Will my claim be denied if the buyer disputes the invoice or delivery?

If the buyer raises a dispute over the invoice or delivery, it could lead to your claim being denied. Most insurers require any disputes to be fully resolved before they’ll process a claim. Common reasons for denial include unresolved disagreements over invoices or problems with documentation, like mismatched buyer names or incomplete shipping records. To reduce the risk of denial, resolve any issues with the buyer promptly and double-check that all your documents are accurate and complete before submitting your claim.