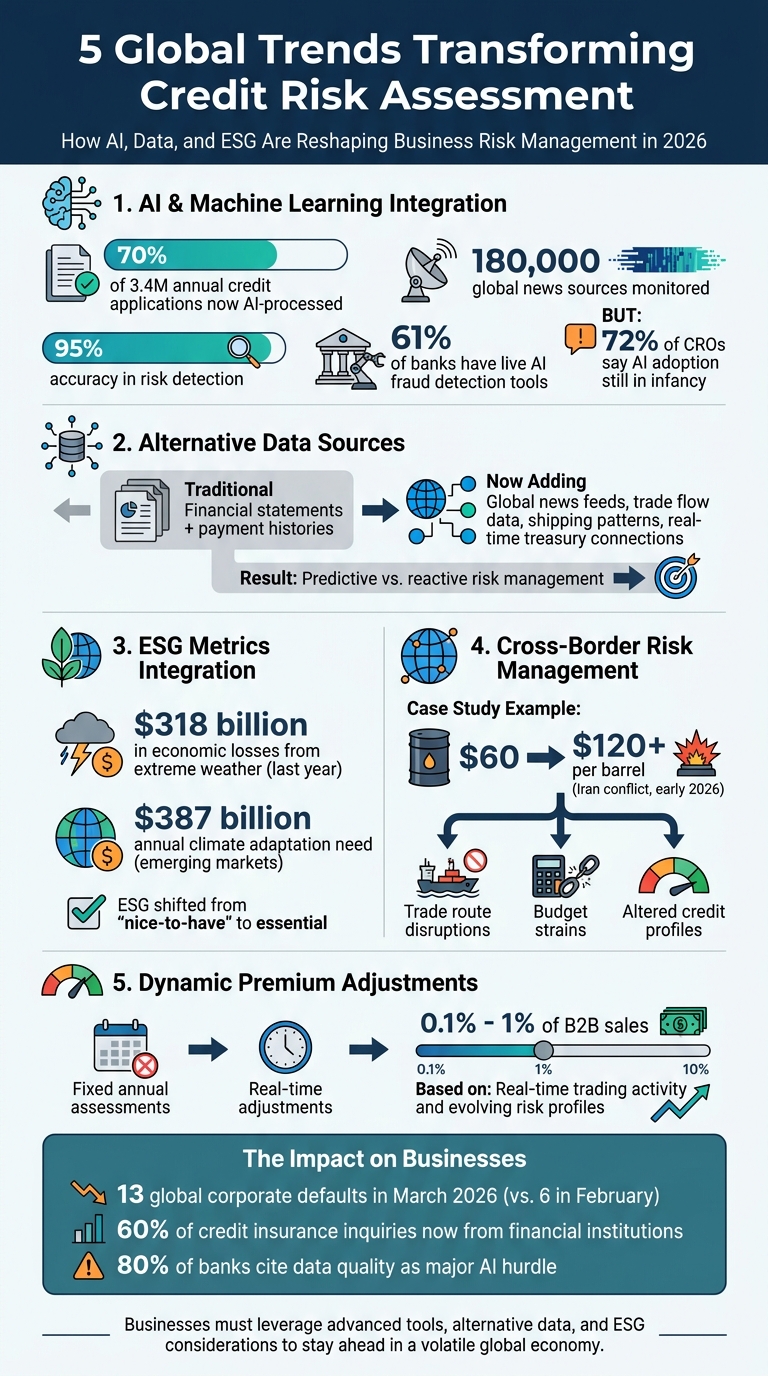

Credit risk assessment is evolving rapidly due to economic instability, geopolitical events, and advances in technology. Here’s what you need to know:

- AI and Machine Learning: These tools are transforming credit evaluations by processing vast amounts of data in minutes, improving accuracy and speed.

- Alternative Data Sources: Beyond financial statements, credit models now use trade flow data, shipping patterns, and real-time treasury connections to predict risks.

- ESG Metrics: Environmental and social factors are now key in assessing creditworthiness, especially with extreme weather causing $318 billion in losses last year.

- Cross-Border Challenges: Political instability, currency fluctuations, and regulatory differences complicate international trade, requiring sophisticated monitoring.

- Dynamic Premiums: Insurers are shifting to real-time premium adjustments based on evolving risks, supported by AI and big data.

The rise of accounts receivable insurance (ARI) highlights how businesses are managing these challenges. ARI policies now offer tailored coverage, real-time updates, and global insights to protect against credit risks at home and abroad.

Key takeaway: Businesses must leverage advanced tools, alternative data, and ESG considerations to stay ahead in a volatile global economy.

5 Global Trends Transforming Credit Risk Assessment in 2026

Major Global Trends in Credit Risk Assessment

Artificial Intelligence and Machine Learning Integration

AI and machine learning have reshaped how credit decisions are made, turning processes that once took days into tasks completed in minutes. For example, in April 2026, Atradius revealed that its AI and machine learning models now handle over 70% of its 3.4 million annual credit limit applications across 140 countries. Aaron Rutstein, Director of Risk Services for Atradius North America, shared:

Our goal was not to replace human judgment, but to augment it. By embedding AI into our underwriting and risk services, we’ve created a digital ecosystem that delivers greater transparency, consistency, and speed.

This technology processes vast amounts of data in real time. AI-driven news monitoring systems, for instance, track 180,000 global sources with 95% accuracy, offering early warnings about negative developments affecting buyers, sectors, or even entire countries. Through API integrations, insurers can embed AI-generated credit data directly into platforms like Microsoft Dynamics 365 Business Central, streamlining credit checks into automated workflows.

Despite these advancements, adoption remains uneven. A February 2026 survey of 101 banks across 31 countries revealed that while 61% have live AI tools for detecting fraud and financial crimes, 72% of chief risk officers admit their AI adoption in risk management is still in its infancy. A significant 80% of respondents pointed to data quality and availability as major hurdles. Marc Henstridge, Chief Market Officer at Atradius, emphasized:

Achieving a fully automated SME solution is no longer optional, and AI can help us finally deliver it.

This AI-driven transformation relies heavily on a wide range of data sources to improve risk evaluations.

Big Data and Alternative Data Sources

Traditional credit assessments focused on financial statements and payment histories. Today’s models incorporate an array of alternative data – global news feeds, trade flow data, shipping patterns, and even real-time connections to clients’ treasury systems. This shift enables predictive, rather than reactive, risk management.

Atradius, for example, processes millions of credit applications annually using systems that integrate these diverse data sources. This not only speeds up decision-making but also improves accuracy. For businesses involved in international trade, such capabilities allow real-time credit limit adjustments during geopolitical disruptions. A case in point: firms monitoring trade route changes through Oman during instability in the Strait of Hormuz.

The push for hyper-automation is especially vital in the SME sector, where seamless onboarding and fast decision-making are critical. This has driven companies to hire data specialists who can structure alternative datasets for effective AI processing.

ESG Metrics in Credit Risk Assessment

Credit risk models are increasingly incorporating non-financial data, especially environmental and social metrics, to address emerging risks. Environmental, social, and governance (ESG) factors have shifted from optional considerations to essential components of credit evaluations. For instance, extreme weather events caused an estimated $318 billion in economic losses last year, damaging property, reducing tax revenues, and destabilizing entire regions. Jarred Lloyd, Head of Analytics at 4most, remarked:

The ESG landscape in the UAE’s financial services sector is shifting from ‘nice-to-have’ to essential.

As a result, insurers are raising premiums and restricting coverage in high-risk areas. Financial institutions are also integrating ESG metrics into credit assessments to align with global net-zero goals, modeling both the physical risks of climate change and the transition risks tied to a low-carbon economy. In emerging markets, the annual need for climate adaptation spending has been estimated at $387 billion.

Cross-Border Credit Risk Management

International trade presents unique challenges – currency fluctuations, political instability, and varying regulatory landscapes – that add complexity to traditional credit risks. Early 2026 provided a stark example: conflict in Iran caused oil prices to spike from $60 to over $120 per barrel. This ripple effect extended beyond energy costs, disrupting trade routes, straining government budgets, and altering credit profiles across entire regions.

Sophisticated monitoring systems are essential to manage these risks. AI-powered platforms can now track multiple variables simultaneously, offering early alerts about country-level risks. This allows businesses to adjust their exposures before conditions deteriorate. Integrated systems also provide proactive updates on debtor health across borders, enabling swift responses to changing international conditions. For businesses operating globally, access to credit insurance carriers with strong local expertise is crucial for navigating these complexities and securing comprehensive coverage both at home and abroad.

sbb-itb-2d170b0

How These Trends Affect Premium Setting

Data-Driven Premium Customization

Advancements in AI and big data are reshaping how insurance premiums are calculated. Instead of sticking to fixed annual assessments, insurers now have the tools to adjust premiums dynamically based on a business’s real-time trading activity. This approach results in pricing that mirrors actual risks as they evolve, rather than relying on outdated historical averages.

The key to this transformation lies in the quality of data. Marc Henstridge, Chief Market Officer at Atradius, emphasized this point:

We are prioritising data experts because without reliable data in the correct structure, AI cannot deliver accurate results.

Atradius has introduced a modular policy system called "Atradius Modula", which links pricing directly to real-time exposure. This system uses tailored modules designed for various customer needs, markets, and trading setups, enabling premiums to reflect evolving risks for businesses operating across multiple regions. Typically, credit insurance premiums range from 0.1% to 1% of insured business-to-business sales, with pricing heavily influenced by the likelihood of non-payment and the potential loss size.

Alternative data is also becoming a game-changer, revealing risks that traditional metrics might miss. For example, in Canada, hidden fraud in credit portfolios is estimated to reach $1.3 billion, bypassing standard security measures. By integrating alternative data sources, insurers can pinpoint creditworthy applicants and uncover risks that conventional financial data might overlook. In the U.S., Equifax’s Market Pulse Index tracked economic shifts in Q4 2025, showing an increase in the high-resilience segment (Index 80+) from 7.96% to 10.47% of the population. This granular data allows insurers to tailor credit offers based on specific resilience scores rather than broad economic trends.

This shift toward data-driven insights is paving the way for incorporating non-financial risks into premium models.

ESG Risks in Premium Calculations

Environmental, social, and governance (ESG) factors are now playing a direct role in determining insurance premiums. With extreme weather events becoming more frequent and severe, insurers are raising premiums and limiting coverage for businesses in high-risk areas. Economic losses from such events recently reached about $318 billion in one annual reporting period, forcing insurers to account for these risks to maintain financial stability.

Emerging markets face unique challenges, where the annual need for climate adaptation spending is projected at $387 billion – far exceeding current investments. This funding gap contributes to higher risk levels in these regions. Industries like chemicals and transportation are under increasing scrutiny due to their exposure to environmental regulations and geopolitical uncertainties.

AI and advanced analytics are helping insurers integrate ESG metrics into their underwriting processes. This enables a more detailed assessment of risks that traditional financial data might miss. Businesses that proactively manage cyber, environmental, and social risks can offset rising insurance costs and secure more favorable credit terms.

Risk Monitoring and Claims Management

Insurers are also using predictive monitoring to enhance risk management and claims handling. This shift from reactive to proactive strategies allows insurers to adjust premiums before financial stress becomes apparent in official reports. For instance, rising interest rates and currency fluctuations often lead to longer payment cycles and weaker recovery rates, prompting insurers to revise premiums upward even before defaults occur.

AI-driven tools are also optimizing credit recovery processes. By prioritizing accounts and streamlining collections, insurers can stabilize premiums by reducing the volume of claims. Businesses that maintain disciplined credit limits and closely monitor their financial health inspire more confidence in insurers, often resulting in better pricing. Transparency and visibility are critical – when uncertainty decreases, premium rates tend to stabilize.

Whiteboard series – How AI and ML are revolutionizing credit risk modeling?

How Accounts Receivable Insurance Addresses Credit Risks

Accounts Receivable Insurance (ARI) has become a key tool for managing the shifting landscape of global credit risks. By leveraging advanced data and adaptive solutions, ARI helps businesses navigate emerging challenges with confidence.

Customized Policies for Emerging Risks

Modern ARI policies are designed to tackle unpredictable risks head-on. Non-cancelable policies are a standout feature, ensuring uninterrupted coverage throughout the policy term – even when a buyer’s risk profile changes due to economic or geopolitical upheavals. For instance, during the early 2026 Middle East conflicts that caused oil prices to double, these policies proved essential.

Insurers also play a proactive role in mitigating disruptions. When instability in the Strait of Hormuz threatened trade, companies were able to reroute shipments through alternative hubs in Oman with the support of their ARI providers. For large, high-value transactions, insurers use syndication and coinsurance to spread risk, ensuring capacity remains available.

Another game-changer is the integration of AI-driven adaptive coverage, which adjusts policies in real time based on trading behaviors. This automation makes ARI accessible and efficient for businesses of all sizes, offering a seamless way to manage credit risks.

But ARI doesn’t stop at policy customization – it also benefits from a strong global network that provides unparalleled risk intelligence.

Global Network of Credit Insurance Carriers

A well-connected global network of credit insurance carriers is crucial for U.S. businesses operating in today’s volatile markets. This network delivers valuable insights into regional credit conditions across Asia-Pacific, Europe, North America, and emerging markets. Its importance was evident during March 2026, when global corporate defaults surged to 13, more than double the six defaults from the previous month.

The network excels in tracking risks by industry. Sectors like chemicals, petrochemicals, steel, and transportation have faced heightened vulnerabilities due to trade disruptions, while industries like technology and utilities have remained relatively stable. Local teams stationed in high-risk regions, such as Saudi Arabia and the UAE, provide real-time updates on trade route disruptions and debtor stability. Their on-the-ground knowledge helps businesses identify alternative supply chains and develop mitigation strategies. This localized expertise enhances underwriting accuracy and equips businesses to handle the complexities of an increasingly transactional global economy.

Armed with these insights, ARI solutions offer seamless coverage for both domestic and international markets.

Coverage for Domestic and International Markets

ARI policies are tailored to meet the unique needs of businesses operating within the U.S. and abroad. These solutions not only protect receivables but also improve financing options like factoring, invoice discounting, and stock finance.

For domestic operations, insurers use big data and alternative data sources to identify risks that traditional financial metrics might miss. This approach helps uncover hidden vulnerabilities and pinpoint creditworthy partners – an essential capability for navigating the uneven recovery of a K-shaped economy.

Internationally, ARI addresses challenges like geopolitical tensions and regulatory changes. For example, insurers help businesses adapt to tariff shifts amid U.S.-China trade tensions or comply with laws such as the UK’s anti-greenwashing regulations. When primary coverage falls short, top-up solutions fill the gaps, ensuring full protection for high-value accounts.

Conclusion

Key Takeaways for U.S. Businesses

Credit risk assessment today is shaped by the growing challenges of political polarization, climate disruptions, and rapid technological changes. In the U.S.’s uneven, K-shaped economy, some sectors remain steady while others face mounting financial pressures. This landscape calls for a new, more dynamic approach to managing risk.

Relying solely on traditional credit data is no longer enough. Businesses must now incorporate alternative data sources to uncover hidden risks and identify reliable partners. At the same time, proactive portfolio monitoring has become crucial for spotting early warning signs of financial stress. For example, global corporate defaults surged to 13 in March 2026, more than doubling February’s total of six.

Credit insurance has evolved into a critical financial tool. Around 60% of inquiries about credit insurance now come from financial institutions aiming to secure capital relief and better financing terms. The unpredictability of geopolitical events – like oil prices doubling from $60 per barrel due to Middle Eastern conflicts in early 2026 – further emphasizes the need for businesses to diversify trade routes and maintain flexible supply chains.

These shifts highlight the urgency for businesses to adapt their strategies, as the future of credit risk management will require even greater agility and technological integration.

The Future of Credit Risk Assessment

The growing pressures of geopolitical instability and climate-related risks mean that full automation for small and medium-sized enterprise (SME) solutions is no longer optional. As Henstridge stated:

Achieving a fully automated SME solution is no longer optional, and AI can help us finally deliver it.

Most credit limit applications are now automated, and this trend continues to grow as businesses increasingly demand instant onboarding and flexible coverage that adapts to real-time trading patterns.

Climate risks are also reshaping the industry, influencing premium calculations and coverage options. With extreme weather events causing an estimated $318 billion in economic losses last year, insurers have started raising premiums and restricting coverage in high-risk areas. Businesses should prepare for more detailed ESG (Environmental, Social, and Governance) evaluations, as sustainability metrics are becoming directly tied to credit terms. Addressing climate adaptation needs – estimated at $387 billion annually for emerging markets – will present both obstacles and opportunities for companies ready to embrace these changes.

FAQs

What data should we add beyond financial statements to spot credit risk earlier?

Alternative data sources, alongside financial statements, play a key role in spotting credit risks sooner. These sources include third-party credit data, buyer behavior trends, payment habits, and even factors like cybersecurity and ESG ratings. By analyzing digital footprints, transaction patterns, and trade credit performance, businesses can gain a more complete understanding of risk. Additionally, advanced predictive tools in trade credit insurance underwriting help identify signs of financial instability or potential defaults earlier.

How do ESG and climate risks change credit limits and insurance premiums?

Environmental, Social, and Governance (ESG) factors, along with climate-related risks, can directly impact financial outcomes. For instance, they may result in higher credit limits and increased insurance premiums. Why? Because as environmental and physical risks grow, so do the chances of significant losses. This heightened risk profile influences both creditworthiness and insurability, prompting lenders and insurers to adjust their terms. The result? Credit insurance becomes more expensive to reflect these elevated risks.

How can accounts receivable insurance support cross-border credit decisions in real time?

Accounts receivable insurance helps businesses navigate cross-border trade by offering real-time risk assessments and credit limit information. With this support, companies can make quick, informed decisions, reducing the risks tied to non-payment or geopolitical challenges in international transactions.