Solvency II is the EU’s regulatory framework for insurers, designed to ensure financial stability and reduce insolvency risks. It focuses on three key areas: capital requirements (Pillar 1), governance and risk management (Pillar 2), and transparency through public disclosures (Pillar 3). For international credit insurers, compliance involves managing complex reporting standards, meeting strict deadlines, and navigating multi-jurisdiction regulations, especially post-Brexit.

Key highlights:

- Capital Requirements: Insurers must meet Solvency Capital Requirement (SCR) and Minimum Capital Requirement (MCR) thresholds, ensuring a 99.5% and 85% probability of adequacy, respectively.

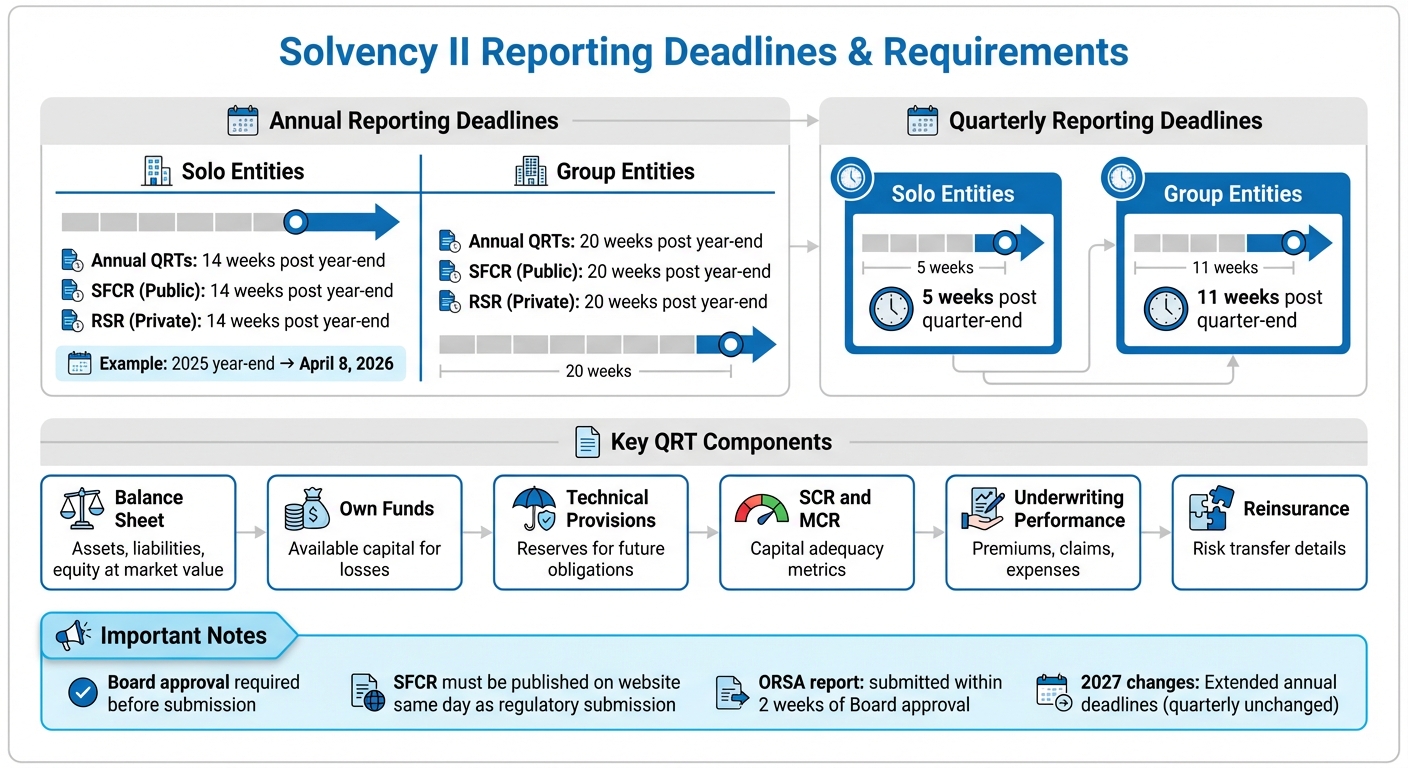

- Reporting Obligations: Annual reports, including QRTs and the Solvency and Financial Condition Report (SFCR), are due 14 weeks after the year-end for solo entities. Quarterly QRTs are due within 5 weeks.

- 2025 Revisions: Updates include climate risk integration, reduced reporting for smaller firms, and new deadlines starting in 2027.

- Brexit Impact: Insurers face dual compliance with Solvency II in the EU and Solvency UK, which introduces different capital and reporting standards.

To comply effectively, insurers must focus on accurate data management, risk assessments, and timely submissions. Accounts Receivable Insurance (ARI) can also help reduce credit risk and streamline compliance with Solvency II requirements.

The SFCR and Other Public Reporting: A Solvency II Cornerstone

sbb-itb-2d170b0

Core Solvency II Reporting Requirements

Solvency II Reporting Deadlines and Requirements for Credit Insurers

International credit insurers must meet specific reporting standards under Solvency II to demonstrate their financial stability and risk exposure. These regulations focus on three primary areas: Quantitative Reporting Templates (QRTs), strict submission timelines, and public disclosure via the Solvency and Financial Condition Report (SFCR).

Quantitative Reporting Templates (QRTs)

QRTs are standardized forms designed to capture detailed data about an insurer’s financial health, risk exposure, and capital reserves. They provide insights into assets, liabilities, technical provisions, and capital requirements, ensuring consistency across the industry by using market-consistent valuation for all entries.

| QRT Component | Description | Key Data Points |

|---|---|---|

| Balance Sheet | Overview of financial position | Assets, liabilities, and equity at market value |

| Own Funds | Available capital for losses | Basic and ancillary funds, including their quality and quantity |

| Technical Provisions | Reserves for future obligations | Present value of policyholder obligations |

| SCR and MCR | Capital adequacy metrics | Risk-based requirements and minimum safety net |

| Underwriting Performance | Contract profitability | Premiums, claims, and expenses by business line and location |

| Reinsurance | Risk transfer details | Reinsurance treaties and their effectiveness |

These templates also assess risks specific to credit insurance, like counterparty and non-life underwriting risks. Insurers can calculate the Solvency Capital Requirement (SCR) using either a standard formula or an approved internal model tailored to their operations.

FasterCapital highlights that QRTs allow insurers to evaluate and manage risks proactively. To ensure accuracy, companies should integrate cross-validation checks across data sources and automate data collection from systems like accounting software and actuarial models. Larger insurers often establish dedicated data quality teams to minimize errors during QRT preparation.

Once QRT data is structured, insurers must meet the reporting deadlines.

Reporting Deadlines: Annual and Quarterly

Adhering to reporting timelines is a critical aspect of Solvency II compliance. Solo undertakings are required to submit quarterly QRTs within five weeks of the quarter-end, while group undertakings have up to 11 weeks. For annual reporting, solo entities must submit QRTs, the SFCR, and the Regular Supervisory Report (RSR) within 14 weeks of the financial year-end. For example, the 2025 year-end deadline fell on April 8, 2026.

| Reporting Requirement | Solo Entity Deadline | Group Entity Deadline |

|---|---|---|

| Annual QRTs | 14 weeks post year-end | 20 weeks post year-end |

| Quarterly QRTs | 5 weeks post quarter-end | 11 weeks post quarter-end |

| SFCR (Public) | 14 weeks post year-end | 20 weeks post year-end |

| RSR (Private) | 14 weeks post year-end | 20 weeks post year-end |

The Own Risk and Solvency Assessment (ORSA) report, meanwhile, must be submitted to regulators within two weeks of Board approval. Katrina Monaghan and Aisling Barrett from Milliman note:

"The narrative reports and QRTs typically need to be drafted well in advance of the reporting deadlines, as the Board must approve them before publication/submission to the regulator".

Starting with the 2027 reporting cycle, annual deadlines for QRTs, RSRs, and SFCRs will be extended, though quarterly deadlines will remain unchanged. To prepare, insurers are encouraged to conduct mock reporting exercises to identify potential challenges in data collection and workflow efficiency.

These strict timelines ensure accountability and operational rigor across the insurance sector.

Public Disclosure Through SFCR

The SFCR is the primary public-facing document under Solvency II, offering transparency to policyholders and market stakeholders. Insurers must publish the SFCR on their website the same day it is submitted to regulators. The report includes five mandatory sections: Business and Performance, System of Governance, Risk Profile, Valuation for Solvency Purposes, and Capital Management.

For credit insurers, the Business and Performance section must highlight underwriting results in credit and suretyship lines, along with investment outcomes. The Risk Profile section focuses on exposures to credit, market, and operational risks – key areas for credit insurers. The Capital Management section outlines available funds and SCR, showing the insurer’s ability to meet its obligations.

Unlike the SFCR, the RSR is a private document submitted to regulators, containing more detailed insights into the insurer’s operations and governance. While the RSR is typically required every three years, regulators may request it annually. The SFCR’s public nature promotes market discipline by allowing external analysts to assess the insurer’s risk and financial performance.

Multi-Jurisdiction Compliance Issues

Navigating the complexities of Solvency II reporting becomes even more challenging in a world of varying international regulations. For credit insurers operating across borders, the post-Brexit regulatory landscape has introduced significant differences. The UK has established "Solvency UK", which will be fully effective by December 31, 2024, while the EU has rolled out its 2025 revision under Directive (EU) 2025/2, requiring member states to adopt the changes by January 30, 2027. These diverging frameworks complicate operations for insurers active in both the UK and EU.

Third-Country Equivalence and Post-Brexit Changes

Third-country equivalence plays a key role in determining whether a non-EEA country’s regulatory framework can be considered comparable to Solvency II. This impacts how insurers manage group solvency and reporting. The European Commission assesses equivalence in three main areas: Reinsurance (Article 172), Group Solvency (Article 227), and Group Supervision (Article 260).

A positive equivalence decision under Article 227 allows EU-based insurance groups to apply local capital requirements and balance sheet rules for their non-EEA subsidiaries when calculating group solvency. Without this designation, insurers must align all international activities with Solvency II standards to avoid supervisory arbitrage. Switzerland has achieved equivalence across all three areas, while the United States and Bermuda are recognized only for group solvency purposes. These decisions are typically granted for renewable 10-year periods.

Since Brexit, the UK’s regulatory framework has diverged significantly from the EU’s, creating disparities in capital deployment. For instance, in December 2023, the UK reduced its Risk Margin Cost of Capital from 6% to 4%, while the EU’s revised rate stands at 4.75%. Additionally, the UK has relaxed third-country branch requirements, removing local capital mandates for branches from "broadly equivalent" jurisdictions. Meanwhile, the EU continues to enforce stricter rules, requiring third-country branches to meet local capital standards and maintain assets within the host state.

"The EU’s equivalence assessments must be forward-looking, given the UK’s stated intention to diverge from EU rules."

- Michel Barnier, Chief Brexit Negotiator

This forward-looking stance means insurers cannot depend on past equivalence decisions when planning cross-border activities. The UK has also eliminated the Regular Supervisory Report (RSR) requirement, while the EU now demands more detailed and frequent solvency and risk exposure reporting.

| Feature | Solvency UK | EU Solvency II (2025 Revision) |

|---|---|---|

| Cost of Capital (Risk Margin) | 4% | 4.75% |

| Third-Country Branches | No local capital required if "equivalent" | Must adhere to local capital/regulatory standards |

| Reporting (RSR) | Requirement removed | Retained; more detailed/frequent reports required |

| GWP Threshold | £25 million | €15 million |

Given the uncertainties around equivalence, insurers are advised to prepare contingency plans. For example, under Article 260, EEA regulators may require the establishment of an EU-based holding company if a third-country jurisdiction is not deemed equivalent.

These regulatory differences also affect how reinsurance and risk transfers are reported, as outlined below.

Reporting Reinsurance and Risk Transfer

The challenges of equivalence extend into the accurate reporting of reinsurance arrangements. Proper reporting ensures that risk transfer across borders is accurately reflected. To maximize capital credit under Solvency II, insurers must confirm that their reinsurers meet one of the following criteria:

- Are Solvency II-authorized

- Operate in an "equivalent" jurisdiction like Bermuda or Switzerland

- Have a credit quality step of three or better if located in a non-equivalent jurisdiction

Contracts must be enforceable across jurisdictions. Insurers should avoid clauses that could undermine the effective transfer of risk, such as termination conditions beyond their control. As noted in the Skadden Encyclopaedia of Prudential Solvency:

"The contractual arrangements for risk transfer to and from the SPV must be effective in all circumstances, clearly defining the extent of the risk transferred"

The table below highlights the credit requirements for reinsurers in different jurisdictions:

| Reinsurer Category | Requirement for Maximum Capital Credit |

|---|---|

| EEA (Solvency II) | Must comply with its own SCR |

| Equivalent Third Country | Must comply with home country solvency requirements (e.g., Bermuda, Switzerland) |

| Non-Equivalent Third Country | Must have credit quality step 3 or better, or provide qualifying collateral |

| Special Purpose Vehicle (SPV) | Must be "fully funded" and assets must exceed aggregate maximum risk exposure |

Post-Brexit, the UK is classified as a third country under EU Solvency II. To qualify, UK reinsurers must meet specific credit ratings or provide adequate collateral. Bilateral agreements between the US and both the EU and UK simplify certain requirements, such as waiving collateral mandates for reinsurers under specific conditions.

Insurers must also address basis risk, which occurs when protection levels and liability characteristics do not align. This must be incorporated into Solvency Capital Requirement (SCR) calculations. For risk mitigation techniques to qualify for full SCR credit, they must remain in effect for at least 12 months; otherwise, credit is applied proportionately to the exposure period. Additionally, all third-country branches are required to submit reports in XBRL format.

Compliance Challenges and Practical Solutions

Meeting the demands of Solvency II involves more than just cross-border reporting – internal operational efficiency plays a crucial role. International credit insurers face significant hurdles, particularly in maintaining data quality and reliability throughout the reporting process. A common issue is the reliance on manual spreadsheet aggregation, which introduces delays, errors, and poor traceability. During the Solvency II preparation phase (QIS5), company actuaries required anywhere from 5 to 13 months to process data and assess changes in solvency ratios.

Data Management and Reporting Accuracy

Functional silos between risk management, actuarial, and finance teams often lead to inconsistencies in risk assessments and capital calculations. Regulators demand detailed audit trails to document data collection, processing, and usage, but manual systems make this level of traceability nearly impossible. As Gunther Schwarz, Partner at Bain & Company, explained:

"Insurers will need to upgrade information technology systems and replace their improvised risk‐measurement tools with robust automated solutions that can accommodate both their audit and risk‐reporting demands".

By adopting integrated platforms that link actuarial models, risk-data warehouses, and finance ledgers, insurers can eliminate these inconsistencies. Creating a unified source of truth across departments also reduces fragmented decision-making and enhances operational efficiency.

Aligning Reporting with Risk Management

Solvency II compliance shouldn’t exist in a vacuum; it must align with an insurer’s broader business strategy. A key component of this alignment is the Own Risk and Solvency Assessment (ORSA), which EIOPA describes as:

"the entirety of the processes and procedures used to identify, assess, monitor, manage, and report the short- and long-term risks an insurance company faces or may face and to determine the own funds necessary to ensure that the company’s overall solvency needs are met at all times".

To make ORSA more than just a regulatory requirement, insurers should integrate its outcomes into strategic planning and capital allocation. This involves setting clear board-level risk appetites and using ORSA as a dynamic management tool. Real-time monitoring and frequent stress-testing can enhance responsiveness to emerging risks. Given that Solvency II mandates insurers to hold enough capital to meet all future claims with a 99.5% probability, accurate and forward-looking risk assessments are critical for long-term sustainability. These strategies help insurers address both external compliance requirements and internal risk management challenges effectively.

How Accounts Receivable Insurance Supports Risk Management

Accounts Receivable Insurance (ARI) offers practical solutions for addressing challenges in data management and risk alignment. It plays a key role in mitigating risks by protecting against non-payment and insolvency, which are critical components of Solvency Capital Requirement (SCR) calculations. This protection helps maintain stable technical provisions and aligns well with international reporting strategies, especially in complex regulatory landscapes.

Trade Credit Insurance Coverage

ARI provides tailored coverage for both domestic and international markets, safeguarding businesses from counterparty defaults. This is an essential factor in SCR calculations, as it reduces both the loss-given default and the probability of default – key parameters in capital requirement formulas. The mechanism of risk transfer offered by ARI is acknowledged under Solvency II, which emphasizes the importance of risk mitigation techniques like guarantees and collateral.

The upcoming 2025 Solvency II revision (Directive (EU) 2025/2) will require the integration of sustainability and climate risks into the standard formula. ARI’s detailed, data-driven risk assessments provide debtor-level insights, which are crucial for the look-through approach in SCR calculations. For insurers in the UK, the Matching Adjustment Investment Accelerator (MAIA), effective October 27, 2025, allows for self-assessment of asset eligibility and immediate application of capital benefits. ARI complements these frameworks by reducing capital volatility and contributing to more consistent risk management practices.

In addition to providing coverage, ARI enhances operational risk management through its specialized risk assessments and proactive claims management.

Risk Assessments and Claims Management Services

ARI providers deliver comprehensive risk assessments and claims management services that align with Pillar 2 governance and ORSA (Own Risk and Solvency Assessment) requirements. These services offer real-time insights into debtor health and market trends, enabling insurers to refine their assumptions about the timing and amount of claim settlements. This is particularly important for accurate Best Estimate Liabilities (BEL) calculations. As highlighted by Solvency II Solutions:

"The Own Risk and Solvency Assessment (ORSA) adds a forward-looking perspective, compelling insurers to assess how their risks and solvency positions might evolve under different scenarios".

Continuous monitoring through ARI enhances Pillar 3 transparency, providing granular data for Quantitative Reporting Templates (QRTs). Recent reforms (PS3/24) have streamlined these templates to focus on non-life product obligations and reinsurance. For smaller credit insurers with gross premium volumes under $100 million, the 2025 revisions introduce "small and non-complex enterprises" (SNCE) status, which reduces reporting requirements. However, accurate risk data from ARI remains critical for demonstrating compliance with proportionality principles.

This alignment ensures ARI’s support across all three regulatory pillars, as summarized below:

| Requirement Pillar | Focus Area | ARI Support Mechanism |

|---|---|---|

| Pillar 1 | Quantitative (SCR/MCR) | Reduces credit risk; stabilizes technical provisions |

| Pillar 2 | Governance & Risk Management | Offers risk assessments for ORSA; strengthens internal controls |

| Pillar 3 | Disclosure & Transparency | Provides data for QRTs and public disclosures (SFCR) |

Conclusion

Key Reporting Requirements Recap

International credit insurers must adhere to strict reporting deadlines under Solvency II. Solo undertakings are required to submit their annual QRTs, the SFCR, and the RSR within 14 weeks after the end of the year (for example, April 8, 2026, for the 2025 reporting cycle). Quarterly QRTs have even tighter timelines, with solo entities needing to file within five weeks, while group undertakings have eleven weeks from the quarter’s end to complete their submission.

Before submission, board approval is mandatory, and in some jurisdictions, directors must also certify the accuracy of the reports. Although a full RSR is generally required every three years, regulators can request it annually if needed. Insurers should also begin preparing for the upcoming changes to the Solvency II framework, set to take effect on January 30, 2027. These updates will bring extended annual reporting deadlines and introduce new QRT templates under Taxonomy 2.10.0.

Meeting deadlines is essential, but a solid focus on effective risk management is equally important.

Risk Management and Insurance Solutions

While compliance with Solvency II’s reporting standards is vital, embedding strong risk management practices into operations strengthens solvency and governance. The framework’s risk-based capital approach ensures that the likelihood of insolvency for insurers remains exceptionally low – estimated at no more than 1 in 200 years. This is further supported by historically low insolvency rates across the EEA.

Accounts Receivable Insurance aligns well with Solvency II’s emphasis on risk management. It mitigates credit risk while offering detailed data to improve risk assessments and streamline claims handling. Francesco Merlin, Chair of the Solvency II Working Group at Insurance Europe, highlights the framework’s effectiveness:

"Solvency II – the EU’s comprehensive, risk-based prudential framework – has demonstrated that European policyholders remain very well protected".

FAQs

Which Solvency II reports do credit insurers file each year?

Credit insurers must file annual Solvency II reports, which include the Solvency and Financial Condition Report (SFCR) and the Regular Supervisory Report (RSR). These reports are generally due by April 8 of the year following the reporting period.

What data is hardest to gather for QRTs?

The hardest part of collecting data for QRTs is often obtaining detailed risk exposure and capital adequacy information. This stems from the challenge of consolidating data from multiple entities while ensuring it remains consistent across different jurisdictions.

How does Accounts Receivable Insurance affect SCR?

Accounts Receivable Insurance (ARI) can play a key role in influencing the Solvency Capital Requirement (SCR) under Solvency II regulations. By mitigating an insurer’s risk exposure, ARI reduces the overall risk profile. A lower risk profile often means insurers may need less regulatory capital to meet compliance standards, providing a potential financial advantage.