Policy compliance isn’t just about following rules – it’s a safeguard against financial penalties, legal issues, and damage to your reputation. Non-compliance can cost businesses an average of $14.82 million, far more than the expense of staying compliant. Recent cases, like Meta’s €1.2 billion GDPR fine in 2023, highlight the stakes. Beyond fines, compliance failures can lead to lost consumer trust, legal battles, and even business shutdowns.

Key compliance challenges include:

- Lack of employee training: 42% of compliance professionals cite insufficient training as a major issue.

- Managing policy exceptions: Untracked exceptions create risks and complicate audits.

- Changing regulations: 43% of compliance leaders struggle to keep up with evolving laws.

- Weak documentation: Poor record-keeping leads to fines, like Citigroup’s $400 million penalty in 2020.

- Unclear roles: Scattered responsibilities result in overlooked tasks.

Solutions include:

- Frequent, role-specific training: Monthly, interactive sessions improve retention and cut violations by 40%.

- Exception management systems: Automate tracking and approvals for policy deviations.

- Integrated compliance tools: Centralize documentation and monitor regulatory changes in real time.

- Continuous monitoring: Use technology to test controls and flag risks instantly.

- Clear accountability: Assign roles and link compliance metrics to leadership performance.

Accounts Receivable Insurance (ARI) can also help by enforcing documentation standards, monitoring risks, and simplifying compliance for global operations. With ARI, businesses can protect up to 100% of receivables while reducing financial and regulatory risks.

The bottom line: Compliance isn’t just about avoiding penalties – it’s about building trust and stability while reducing long-term costs.

10 Strategies to Prepare for Key Regulatory Compliance Changes in 2024

sbb-itb-2d170b0

Common Policy Compliance Challenges

Building on the financial and reputational risks discussed earlier, this section examines key compliance challenges that organizations must address promptly.

Insufficient Employee Training and Awareness

In 2023, 42% of compliance professionals identified employee training as one of their biggest hurdles. The problem isn’t just the lack of training – it’s how training is delivered. Many companies treat compliance education as a one-time event, which means employees often forget critical regulatory protocols over time.

This creates a dangerous knowledge gap. Employees may miss red flags like unusual transaction patterns or incomplete customer documentation. Worse, they can become easy targets for social engineering attacks, such as spear-phishing campaigns designed to exploit these weaknesses. Without ongoing education, these lapses not only increase risks but also complicate the handling of policy exceptions.

Handling Policy Exceptions and Non-Standard Cases

Compliance frameworks need some flexibility, but managing exceptions can be tricky. For example, businesses often let long-standing relationships with clients or suppliers override standard protocols. A credit manager might skip due diligence for a trusted client or approve credit limits based on informal judgments rather than documented risk assessments.

In trade credit insurance, these exceptions can be especially risky during events like buyer insolvency or political instability. Without a formal approval process or proper documentation, companies lose track of waived policies. This lack of oversight creates a web of undocumented exceptions that auditors and regulators can’t verify, exposing the organization to unnecessary risks.

Adapting to Changing Regulations

Regulatory landscapes change rapidly, and 43% of Chief Ethics and Compliance Officers cite new regulations as their top challenge. For companies operating across multiple regions, the difficulty is even greater. Domestic and international regulations often evolve independently and may even conflict with one another.

Falling behind on compliance can have serious consequences. For instance, 20% of UK companies were unaware of their obligations under the recently introduced NIS2 framework, leaving them vulnerable to enforcement actions. Between 2008 and 2018, financial institutions worldwide paid nearly $27 billion in fines for failing to meet AML (Anti-Money Laundering) and KYC (Know Your Customer) regulations. Many of these violations stemmed from outdated policies that failed to keep up with regulatory changes. These evolving rules not only complicate compliance but also make managing exceptions even harder.

Poor Documentation and Record-Keeping

In October 2020, Citigroup faced a $400 million fine from federal regulators due to "long-standing deficiencies" in risk management and internal controls – even though the company employed roughly 30,000 risk and compliance staff members. The root problem? Weak documentation systems that couldn’t provide clear evidence of compliance activities.

When data is scattered across disconnected systems, compliance teams waste time piecing together information for audits. Only 4% of governance professionals report that their GRC (Governance, Risk, and Compliance) and financial systems are fully integrated. Relying on fragmented email chains or isolated spreadsheets makes it nearly impossible to trace financial calculations or prove that proper due diligence was completed. Without strong documentation, compliance efforts remain invisible to auditors.

Unclear Roles and Responsibilities

Poor governance structures often mean no single team is fully accountable for specific regulatory requirements or data quality standards. When resources are stretched thin, scattered responsibilities can lead to critical tasks being overlooked. Compliance teams frequently face pressure to shift focus to immediate operational needs, which often results in policy waivers or exceptions being granted without proper oversight. This lack of accountability leaves organizations vulnerable until an audit or enforcement action exposes the gaps.

Solutions for Policy Compliance Challenges

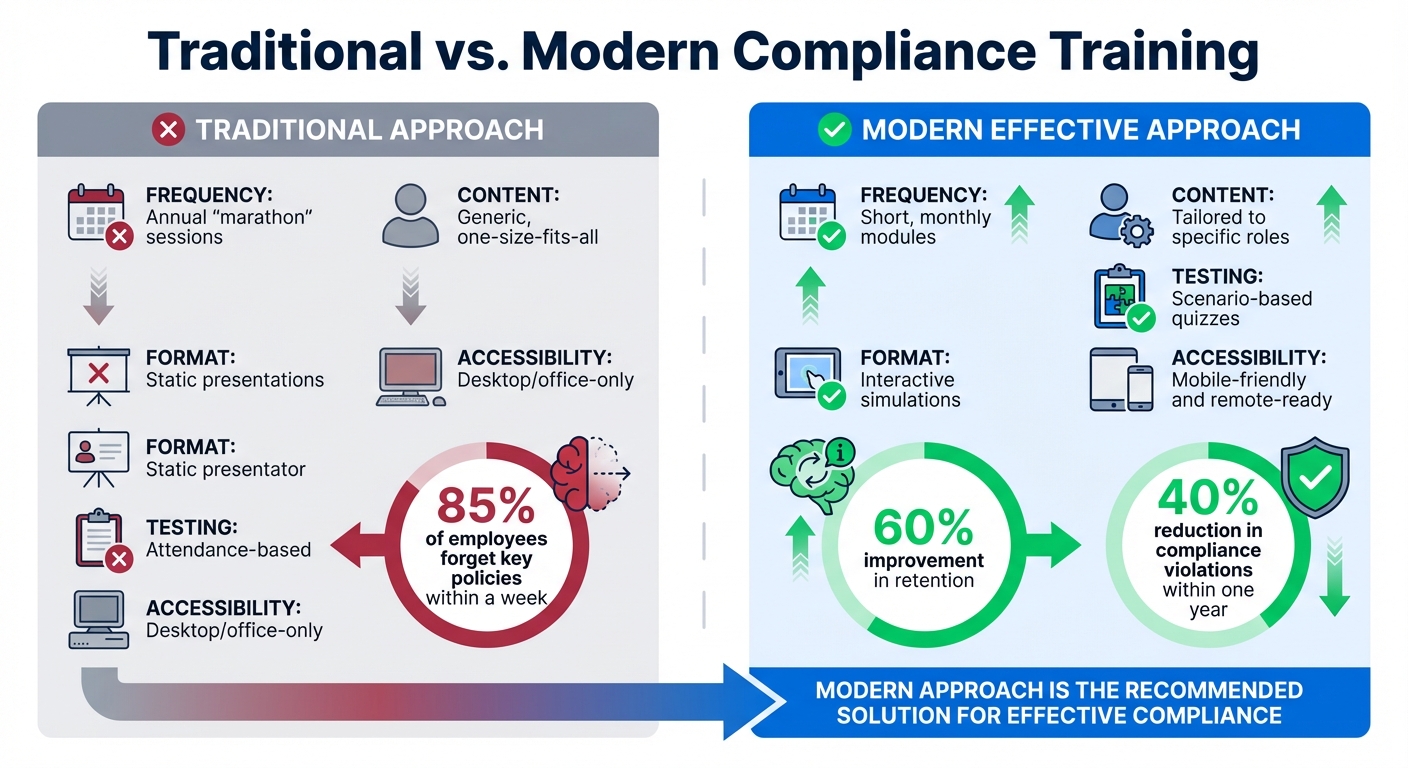

Traditional vs Modern Compliance Training Approaches Comparison

The challenges discussed earlier can be tackled effectively with a structured, technology-focused approach. By rethinking traditional methods and leveraging modern tools, businesses can turn compliance into a manageable and efficient process.

Create Structured Training and Awareness Programs

Annual, generic training sessions often fail to make an impact. Instead, companies should adopt monthly, scenario-based training modules. Research shows that shifting to brief, monthly sessions can reduce compliance violations by 40% within a year. This is because traditional training methods often lead to 85% of employees forgetting key policies within a week.

Effective training programs should focus on role-specific content. For instance, customer support teams might need guidance on identifying suspicious activity, while marketing teams should learn about advertising standards. Interactive methods like micro-learning, quizzes, and simulations improve retention by 60% compared to static presentations.

| Training Component | Traditional Approach | Modern Effective Approach |

|---|---|---|

| Frequency | Annual "marathon" sessions | Short, monthly modules |

| Content | Generic, one-size-fits-all | Tailored to specific roles |

| Format | Static presentations | Interactive simulations |

| Testing | Attendance-based | Scenario-based quizzes |

| Accessibility | Desktop/office-only | Mobile-friendly and remote-ready |

To streamline training, implement a Learning Management System (LMS). This system can centralize tracking, automate reminders, and maintain audit-ready records. Embedding quick prompts or quizzes into tools like Slack or CRM systems can also keep compliance top-of-mind. Most importantly, maintain detailed records of attendance, completion dates, and test results to demonstrate compliance oversight to regulators.

Build a Policy Exception Management System

Managing exceptions effectively is critical for compliance. Policy management software can help by logging, reviewing, and approving every exception with proper documentation. Each deviation should include a clear business justification, an expiration date, and executive approval. Use automated workflows to handle the entire lifecycle of exceptions, from submission to periodic re-validation.

Assign a dedicated policy manager to oversee this process and ensure accountability for tracking exceptions. A clear escalation path should allow the compliance team to report high-risk exceptions directly to senior leadership or the board. Keeping historical records of exceptions, including why they were granted and how they evolved, is essential for maintaining transparency and accountability.

Use Technology for Documentation and Updates

Unified GRC (governance, risk, and compliance) platforms like Diligent One and VComply can consolidate risk, compliance, and policy management into a single system. These tools help cut compliance costs by 40% and reduce violations by 50%. AI-powered regulatory tracking can monitor global legal changes in real time, aligning internal policies with new requirements. This is especially useful for companies operating in multiple jurisdictions, such as those adapting to new SEC cybersecurity disclosure rules.

Modern compliance software links evidence – complete with timestamps and version histories – directly to specific controls, ensuring audit readiness. Cross-framework mapping allows a single control to address multiple regulations (e.g., SOX, GDPR, PCI DSS), eliminating redundant testing. Additionally, these systems can notify supervisors or executives of missed deadlines or red flags, ensuring proactive compliance management.

Perform Regular Control Testing and Monitoring

Annual audits are no longer sufficient. Continuous monitoring and real-time dashboards are far more effective. Continuous Control Monitoring (CCM) technologies like ACL Analytics can automate the testing of transactions and user activity, replacing periodic sampling with 100% data population testing.

Regular control tests should also verify that granted exceptions don’t create larger compliance risks. Live visibility into compliance activities allows managers to catch unauthorized deviations before they escalate. Automated reporting tools can save compliance teams up to 50% of the time they spend on reporting. This kind of real-time oversight ensures consistent adherence to policies.

Assign Clear Roles and Responsibilities

Clearly defined roles are essential for effective compliance. Regulators like FinCEN consider having a designated compliance officer one of the "four pillars" of an Anti-Money Laundering (AML) program. Compliance software should include specific, testable controls – such as "removing terminated employee access within 24 hours" – rather than broad categories like "GDPR" or "SOX".

Integrating compliance tools with HR systems, ERP platforms, and ticketing solutions can automate tasks like policy attestations for new hires. Linking executive compensation to compliance metrics can also reduce violations by 40%. When senior leaders prioritize compliance, it sends a strong message to the entire organization about its importance. Clear accountability and visible leadership support can transform compliance from an afterthought into a core business priority.

How Accounts Receivable Insurance Supports Compliance

Accounts Receivable Insurance (ARI) plays a vital role in safeguarding compliance by embedding strict documentation practices, ensuring alignment with regulations, and maintaining continuous risk monitoring. Considering that accounts receivable often make up about 40% of a company’s total assets, protecting this critical exposure while adhering to policies is essential. ARI provides businesses with tailored solutions to meet diverse compliance challenges effectively.

Tailored Policies for Compliance Requirements

ARI offers several coverage options – whole turnover, key accounts, single buyer, and transactional – to address specific compliance needs. For multinational businesses, these tailored policies simplify navigating international regulations and local licensing laws. By aligning insurance terms with buyer agreements and regulatory frameworks, companies can avoid compliance pitfalls.

"Regulatory alignment is often overlooked in AR insurance or trade credit insurance until a claim is delayed or denied because of a compliance mismatch." – ARI Global

Coverage typically ranges from 80% to 100% of the debt amount, with single buyer policies offering up to 90% indemnity for private buyers and 100% for sovereign buyers. To optimize coverage, businesses should segment their accounts based on industry type, geographic concentration, and buyer credit profiles. This allows for tighter controls where needed and broader coverage elsewhere. Cross-border policies should incorporate legal oversight to prevent claims from being denied due to compliance issues. Additionally, ARI uses comprehensive risk assessments to identify potential challenges before they impact operations.

Risk Assessments and Early Intervention

ARI providers rely on databases tracking over 85 million companies globally to evaluate creditworthiness and flag compliance risks early. With real-time global credit data, specialized analysts monitor customer financial health, enabling businesses to adjust credit terms before defaults occur.

For example, in a business with a 5% profit margin, a $100,000 default would require $2 million in new sales to offset the loss. Risk assessments also account for external factors like geopolitical tensions, market downturns, and industry trends that could affect a buyer’s ability to pay.

Efficient Claims Management for Policy Adherence

Claims management under ARI enforces rigorous documentation standards, including purchase orders, contracts, and delivery proofs. These practices ensure compliance with internal policies and financial reporting standards, while also supporting audit readiness. Businesses must adhere to specific timelines when filing claims – 10–20 days for insolvency cases and up to 180 days for protracted defaults.

Insured receivables are often viewed by financial institutions as lower risk, which can lead to better financing terms and increased borrowing capacity. To streamline compliance, businesses can use AI-powered tools to log credit histories and sync billing data with ERP systems like NetSuite or SAP, ensuring all necessary documentation is readily available for claims. Keeping detailed records also helps counter delays or excessive paperwork during investigations. The cost of securing accounts receivable through trade credit insurance is typically a fraction of one percent of sales, making it a cost-effective way to reduce financial and reputational risks while maintaining strong policy compliance.

Conclusion

Policy compliance has become a vital pillar for financial stability and earning stakeholder trust. When compliance is seamlessly integrated into everyday operations, the results speak for themselves: a 30% drop in employee turnover in high-risk industries, 20% improvement in customer retention, and even an increase in company valuation.

Addressing compliance challenges requires a forward-thinking strategy that doesn’t just mitigate risks but uses compliance as a strategic advantage. For example, interactive, scenario-based training has been shown to improve information retention by 50% to 60%, while tying compliance KPIs to executive compensation ensures accountability at leadership levels.

"Compliance is not just about avoiding penalties; it’s about fostering a culture of integrity, gaining stakeholder trust, and unlocking new opportunities." – ZenGRC

A key component of this strategy is leveraging specialized tools for risk management. Accounts Receivable Insurance supports compliance efforts through detailed documentation and integrated risk assessments. With features like structured claims management and real-time credit monitoring, businesses can remain audit-ready and confidently demonstrate their compliance to regulators and financial partners.

FAQs

What are the first compliance fixes to prioritize?

Keeping up with the pace of changing regulations is essential to avoid penalties and legal troubles. Start by building consistent processes that ensure your company stays ahead. This means regularly monitoring legal updates, adjusting policies as needed, and maintaining thorough documentation. Equally important is providing employees with the training they need to understand and follow these changes.

Paying close attention to data privacy and vendor compliance early on can save your business from expensive fines and damage to its reputation. By addressing these areas proactively, you set the stage for long-term compliance and a more secure operational framework.

How can we track and approve policy exceptions safely?

To manage policy exceptions securely, it’s crucial to establish a structured process. This should include documenting essential details such as start and end dates, timestamps, and the current status in an exception register. By doing this, you create a clear record of all exceptions.

Additionally, regularly reviewing exception data can help pinpoint policies that may be unrealistic or pose compliance risks. This approach ensures exceptions are handled systematically, monitored over time, and aligned with your overall risk management plan. It’s a practical way to uphold governance while keeping risks under control.

How does Accounts Receivable Insurance support compliance?

Accounts Receivable Insurance supports businesses in handling financial risks while aligning with credit and payment regulations. It helps safeguard against challenges like late payments, defaults, or non-payment, reducing financial disruptions and promoting smoother day-to-day operations.