Global trade is risky, but credit monitoring can help you navigate it. Here’s why:

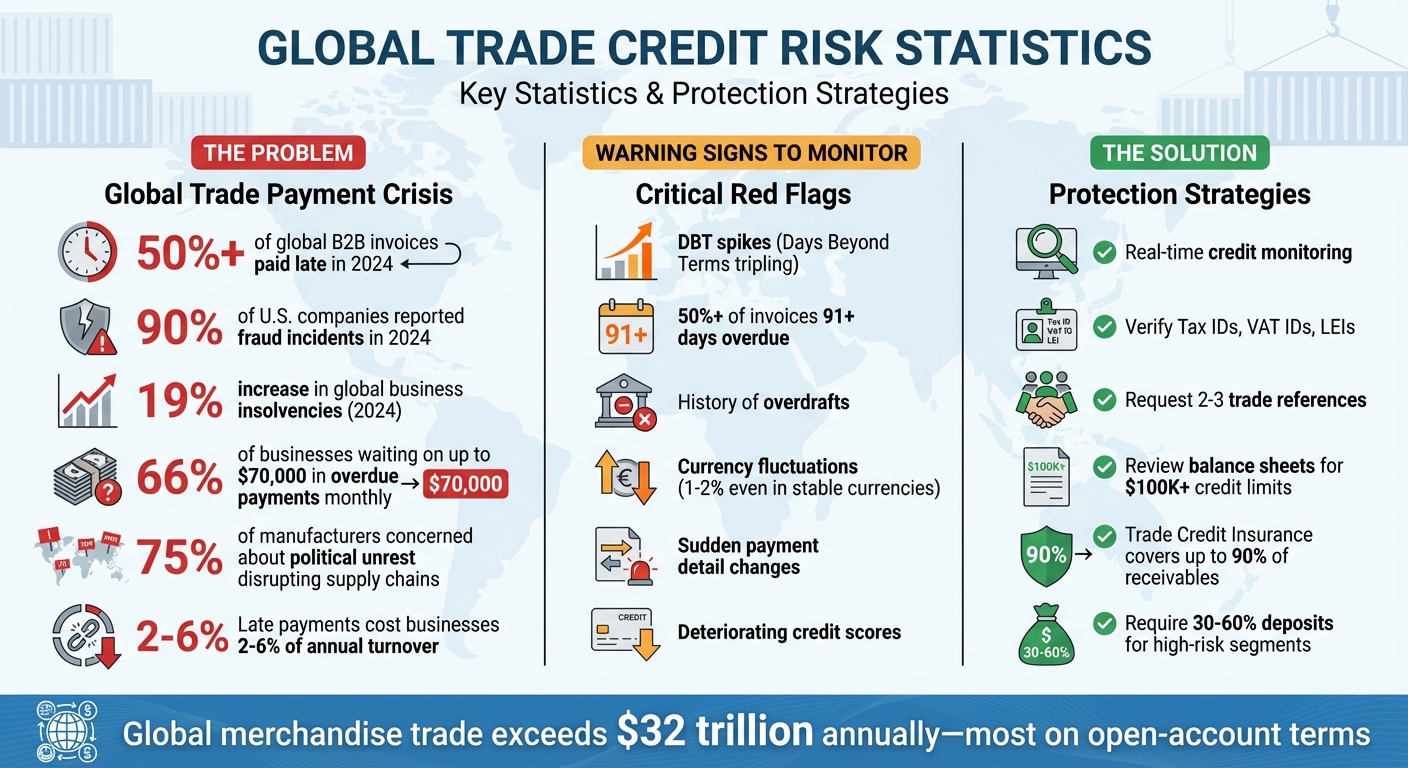

- Over 50% of global B2B invoices were paid late in 2024, affecting cash flow and working capital.

- Cross-border trade faces unique challenges like buyer defaults, political instability, currency fluctuations, and rising cyber fraud incidents (90% of U.S. companies reported fraud in 2024).

- Late payments and defaults can cost businesses 2-6% of their annual turnover.

What can you do?

- Use real-time credit monitoring to track buyer financial health and spot red flags like payment delays or deteriorating credit scores.

- Verify critical details like VAT IDs and Tax IDs to prevent fraud.

- Consider trade credit insurance to protect up to 90% of your receivables and safeguard against defaults and political risks.

Key takeaway: Proactive credit monitoring and risk protection tools like accounts receivable insurance can reduce financial risks, improve cash flow, and help businesses confidently expand into international markets.

Global Trade Credit Risk Statistics and Key Protection Strategies

Credit Insurance as a Risk Mitigation Tool for International Trade

sbb-itb-2d170b0

Risk Factors in Buyer Credit Monitoring

Effectively identifying and managing risks is crucial for maintaining strong credit profiles in international trade. Extending credit across borders exposes businesses to challenges tied to economic-political conditions, financial stability, and industry-specific dynamics.

Economic and Political Risks

The location of your buyer can be just as critical as their financial standing. Currency fluctuations, for instance, can wipe out profits overnight. While currencies like the Argentine Peso and Turkish Lira are well-known for their instability, even relatively steady currencies like the Euro can shift by 1–2% against the U.S. Dollar, impacting trade margins.

Political events can also create barriers unrelated to a buyer’s willingness to pay. Exchange controls may prevent funds from leaving a country, and sanctions from organizations like OFAC, the EU, or the UN can blacklist entities, making transactions illegal. In 2024, 75% of manufacturers expressed concern over how political unrest and labor disputes abroad could disrupt their supply chains.

"Sanctions are legal restrictions imposed by governments on companies or individuals in specific countries, usually to enforce political or economic policies." – Leighton Weston, Global Account Director, Creditsafe

Delays in payments can also stem from inefficiencies in local banking systems or political instability. To protect your business, verify country-specific identifiers like Tax IDs, VAT IDs, or Legal Entity Identifiers (LEIs). These checks ensure you’re dealing with a legitimate entity and provide a pathway for recourse if issues arise.

Buyer Financial Risks

The financial health of your buyer plays a direct role in their ability to meet payment obligations. A buyer’s payment history is one of the most dependable indicators of future behavior. For example, a sudden increase in Days Beyond Terms (DBT) – when payment delays triple compared to the previous year – can signal trouble. Requesting 2–3 trade references from other suppliers can also provide insights into how promptly they pay. In international trade, a buyer is often considered prompt if they pay within 30 days of the due date.

Liquidity issues are another red flag. Bank references can confirm if a buyer has an active line of credit, while reviewing recent year-end balance sheets and profit/loss statements offers a clearer picture of their financial position. With global business insolvencies rising by 19% in 2024, this level of due diligence is more important than ever.

Cyber fraud is an increasingly common financial risk, with 90% of U.S. companies reporting fraud incidents in 2024. If a buyer suddenly requests changes to payment details or bank account information, always verify the request through a separate communication channel before proceeding.

"If you ask to be paid in USD and they insist on using their local currency, that’s worth questioning. Why don’t they want to deal in the world’s reserve currency?" – Leighton Weston, Global Account Director, Creditsafe

Industry-Specific Risks

Certain industries face unique challenges that can impact a buyer’s ability to pay. For example, supply chain disruptions are particularly damaging to manufacturing and retail sectors, often delaying production and affecting revenue streams. Worker strikes and labor disputes can halt operations entirely, leaving buyers without the cash flow necessary to fulfill their payment obligations.

Demand shifts within an industry can also indicate potential risks. Increased competition or declining demand can create liquidity problems, while regulatory changes or compliance violations may result in a buyer being blacklisted or barred from international transactions. In markets like China, verifying social credit numbers has become a standard requirement, adding another layer of compliance to navigate.

"The quality of a credit report you should expect for a hotdog vendor in New York City is going to be very different to a large corporation anywhere in the world. Filing laws vary drastically by country." – Leighton Weston, Global Account Director, Creditsafe

To mitigate risks, tailor your credit policies based on buyer size and region. For high-risk segments, consider requiring letters of credit or a 30–60% deposit upfront.

Credit Monitoring Strategies

Building a Credit Monitoring Framework

To establish a solid credit monitoring framework, start by verifying buyer credentials. Before extending credit, confirm essential details such as the buyer’s legal form, business history, and country-specific identifiers like Tax IDs, VAT IDs, or registration numbers. These identifiers not only validate the legitimacy of the entity but also provide a fallback in case of disputes.

"Make sure you’re collecting correct country-specific identifiers like tax IDs, registration numbers, VAT IDs, or LEIs. That’s your form of recourse if something goes wrong." – Leighton Weston, Product Expert and Global Account Director, Creditsafe

Tailor your credit policies based on region and customer size instead of using a universal approach. Financial data availability can vary widely between countries – what’s accessible for a large corporation in Germany might be entirely different for a mid-sized buyer in Vietnam. Segment your policies for small, medium, and large customers, adjusting credit limits and payment terms to align with the buyer’s location and the reliability of available financial information.

Maintain a centralized database that allows both credit management and sales teams to access up-to-date customer records. This database should support continuous monitoring of key metrics like Days Sales Outstanding (DSO) and Days Beyond Terms (DBT). With 86% of finance professionals reporting that up to 30% of monthly invoiced sales are paid late, consistently tracking these indicators is crucial.

Once your framework is set up, the next step is to dive deeper into financial data to evaluate creditworthiness.

Analyzing Financial Data and Credit Reports

Evaluating creditworthiness requires layering multiple sources of data. Start with third-party credit reports from agencies like Dun & Bradstreet or Creditsafe, which offer standardized scoring models (such as A–E ratings) across over 200 countries. These reports make it easier to compare creditworthiness across regions, despite differences in local financial filing laws. For larger credit limits – typically exceeding $100,000 – request the buyer’s most recent year-end balance sheet and profit/loss statement to assess their financial health.

Trade references provide practical insights into how buyers handle their debts, while bank references confirm whether the buyer has an active line of credit. Use a formal Trade Reference Form to gather details such as the highest credit extended, current overdue balances, and payment behavior. In international trade, buyers are generally considered "prompt" if they settle payments within 30 days of the due date. For bank references, inquire about the length of the banking relationship, average daily balances, overdraft occurrences, and specifics about open loans, including maturity dates and collateral. A signed release from the buyer allows you to verify this information directly with their bank.

For U.S. exporters, the U.S. Commercial Service‘s International Company Profile (ICP) offers detailed credit reports, including insights on the company’s viability and the strength of its industry sector.

"Knowing your market, the type of buyer you are selling to… and getting to know all about your buyer and their culture" is the number one piece of advice for exporters. – Gabriel Ojeda, President, Fitz-Pak Corporation

These financial evaluations help identify potential risks early on.

Warning Signs and Monitoring Tools

With a framework and thorough data analysis in place, monitoring tools act as your last line of defense against credit risks.

Payment behavior often serves as the most reliable indicator of future risks. For example, watch for DBT spikes – if a customer suddenly begins delaying payments significantly longer than usual, it could signal trouble. A delinquency ratio where over 50% of outstanding invoices are 91+ days overdue is another red flag of serious credit risk.

Stay alert to currency and payment anomalies. If a buyer insists on using their local currency instead of USD without a solid reason, it’s worth investigating further.

Cyber fraud is another growing concern. In 2024, 90% of U.S. companies reported fraud incidents, with nearly half experiencing losses exceeding $10 million. If a buyer suddenly requests changes to payment details or bank account information, always confirm the request through a separate communication channel. Cross-check business identifiers with official government records to avoid scams involving fake accounts or impersonated directors – a problem affecting 40% of manufacturers.

Leverage real-time monitoring tools that issue automated alerts when a customer’s credit score or risk profile changes. These tools integrate seamlessly with your centralized database, enabling quick responses to financial declines. Considering that 66% of businesses are waiting on up to $70,000 in overdue payments each month, proactive monitoring is essential to avoid cash flow issues.

| Warning Sign | Detection Method |

|---|---|

| Spiking Days Beyond Terms (DBT) | Business credit reports, trade payment data |

| History of overdrafts | Bank reference letter |

| Fraudulent identity/impersonation | Verification of Tax IDs, VAT IDs, LEIs |

| Political or market volatility | Regional risk insights, credit insurer databases |

| Hidden ownership/sanctions | Ultimate Beneficial Owner (UBO) data, compliance screening |

| Deteriorating cash flow | Year-end balance sheets, profit/loss statements |

Risk Protection with Accounts Receivable Insurance

Understanding Accounts Receivable Insurance

If you already have strong internal monitoring systems, Accounts Receivable Insurance (ARI) adds an essential external layer of protection. Often referred to as trade credit insurance, ARI acts as a safety net against the risk of nonpayment. It shields a significant portion of your receivables from commercial defaults and external shocks like political or economic instability. This includes issues such as sanctions, currency transfer restrictions, sudden regulatory shifts, and conflicts that prevent buyers from fulfilling their payment obligations.

What makes ARI especially valuable is the credit intelligence it provides. Insurers use vast commercial databases to keep tabs on your customers’ financial health. They notify you of any changes in a buyer’s risk profile before a default occurs. This allows you to proactively adjust credit limits or payment terms, complementing your internal monitoring efforts and creating a more comprehensive approach to risk management.

"Trade credit insurance is not just another business expense; it’s a strategic move to safeguard your company’s future." – ARI Global

ARI Benefits for International Trade

Beyond mitigating payment risks, ARI offers additional advantages that are particularly impactful in global trade. By securing your receivables, it enhances your ability to offer competitive open-account terms to new or higher-risk international customers without endangering your cash flow. This flexibility can be a game-changer when trying to win contracts in markets where buyers often expect payment windows of 60 or 90 days.

Insured receivables are seen as high-quality collateral by banks and lenders, which can lead to better loan terms, lower interest rates, and increased borrowing capacity. This can significantly improve your financial leverage. Additionally, ARI helps businesses comply with accounting standards like IFRS 9 by managing expected credit loss provisions. This stabilizes your balance sheet and makes earnings more predictable. In many markets, trade credit insurance covers up to 90% of insured receivables, reducing the financial impact of a major default and helping you stay on track with financial planning and bank covenants.

"For CFOs, the objective is not to eliminate trade credit risk… The objective is to measure it accurately, price it correctly, and manage it actively." – Incomlend

As traditional banks scale back on SME trade financing due to compliance and capital constraints, ARI has emerged as a critical tool for managing liquidity. With global merchandise trade surpassing $32 trillion annually – much of it conducted on open-account terms – transferring risk while staying competitive is no longer a luxury; it’s essential for success.

Conclusion

Effectively managing international credit risk requires consistent effort and vigilance. Financial stability of buyers and market conditions can shift quickly, making one-time credit checks inadequate for fostering lasting trade relationships across borders.

Successful businesses in global markets rely on a mix of active monitoring and thoughtful safeguards. Keeping tabs on payment behaviors, evaluating financial health, and maintaining accurate, centralized data helps identify early warning signs. This allows companies to adjust credit limits before small issues become major problems. These practices not only protect financial health but also strengthen competitiveness.

"The objective is not to eliminate trade credit risk. That would mean stopping trade altogether. The objective is to measure it accurately, price it correctly, and manage it actively." – Incomlend

To enhance internal monitoring, Accounts Receivable Insurance (ARI) adds an extra layer of security to your risk management strategy. ARI transforms credit monitoring into a tool for growth by protecting up to 90% of receivables. This protection enables businesses to confidently enter new markets while offering appealing payment terms.

FAQs

How often should I refresh buyer credit checks?

Keeping buyer credit checks up to date is crucial for maintaining accurate risk assessments. For active credit relationships, it’s a good idea to refresh these checks at least every 30 days. However, the ideal frequency may depend on the buyer’s risk profile and the specifics of the transactions involved.

What are the fastest red flags a buyer may default?

Spotting potential buyer default early can save businesses from significant losses. Some of the clearest warning signs include fraudulent activity, such as making purchases on open accounts without any intention of paying. Additionally, suspicious behaviors like erratic payment patterns or a noticeable lack of transparency in communication should raise concerns. Conducting thorough due diligence and implementing solid risk assessment practices can help identify these issues before they escalate.

When should I add Accounts Receivable Insurance (ARI)?

Accounts Receivable Insurance (ARI) can be a smart addition to your business strategy if you’re looking to protect yourself against non-payment risks. This coverage is particularly useful when dealing with customer insolvency or defaults. It’s especially critical when extending credit to international buyers, where factors like political instability or currency fluctuations can make payments less predictable.