Working capital and trade credit insurance are closely linked. Here’s why it matters:

- Working Capital: The difference between your current assets (like cash and receivables) and current liabilities (like debts and payables). A healthy current ratio (1.20–2.00) signals financial stability.

- Trade Credit Insurance: Protects your business against unpaid invoices, covering 75%–95% of losses due to defaults or insolvency.

Why It Matters: Insurers assess your working capital to determine your eligibility, premiums, and coverage limits. Strong working capital often leads to lower premiums, higher credit limits, and better terms. Weak metrics, however, may result in higher costs or denial of coverage.

Key Metrics Insurers Review:

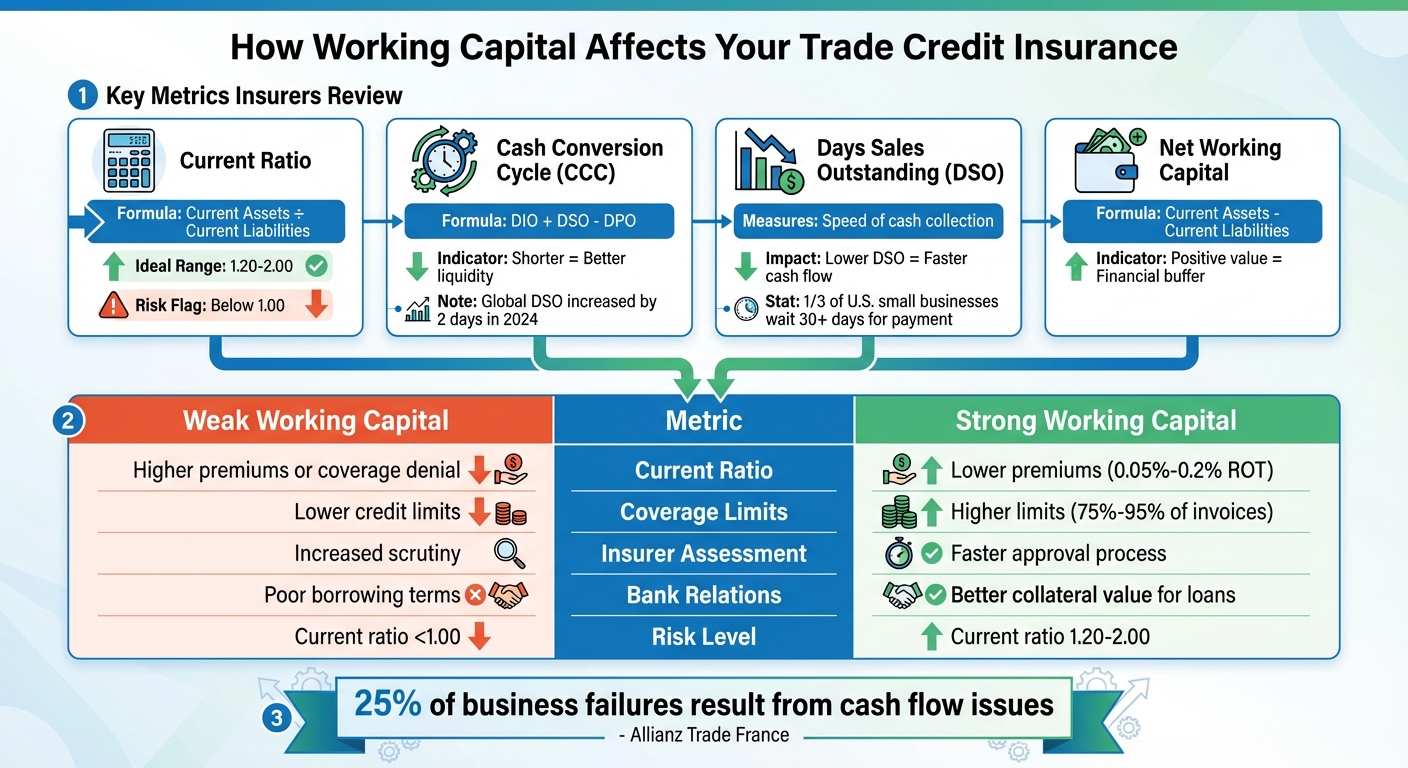

- Current Ratio: Ideal range is 1.20–2.00.

- Cash Conversion Cycle (CCC): Shorter cycles mean better liquidity.

- Days Sales Outstanding (DSO): Lower DSO indicates faster cash collection.

Improving Your Position:

- Manage cash flow by negotiating supplier terms or reducing inventory.

- Lower DSO with prompt invoicing and clear credit policies.

- Consider trade credit insurance to protect receivables and strengthen financial stability.

Takeaway: Healthy working capital isn’t just about daily operations – it directly influences your ability to secure affordable, comprehensive trade credit insurance. Start by auditing your working capital metrics and exploring tailored insurance options to protect your business.

Working Capital in Business & Its Financing, Bank loan, Trade Credit, Invoice Financing, Equity EV

sbb-itb-2d170b0

How Insurers Use Working Capital in Risk Assessment

How Working Capital Metrics Impact Trade Credit Insurance Terms

When you apply for trade credit insurance, insurers dig into your working capital metrics to evaluate how well your business can handle payment delays or customer defaults. This analysis plays a big role in determining whether you qualify for coverage and what your premiums might look like.

Working Capital Metrics Insurers Review

Insurers rely on specific metrics to gauge risk, starting with the current ratio – calculated by dividing current assets by current liabilities. A ratio between 1.20 and 2.00 is generally seen as a sign of lower risk.

Another critical area they examine is your cash conversion cycle (CCC) and Days Sales Outstanding (DSO). These metrics show how quickly you can turn sales into cash. A shorter cycle means faster cash flow, which reduces the risk for insurers. However, global DSO increased by 2 days in 2024, with notable spikes in Europe, signaling rising financial strain in trade.

"Cash is king; cash flow is and will remain the sinews of war. 25% of business failures are the result of suspension of payments."

– Philippe Vammale, Head of Risk Underwriting, Allianz Trade France

Insurers also evaluate your underwriting quality, which reflects how well you assess customer creditworthiness and manage collections. Poor practices in these areas can lead to higher premiums or reduced coverage, making it clear that due diligence is non-negotiable.

How Weak Working Capital Affects Insurance Eligibility

Weak working capital metrics can be a red flag for insurers. For instance, a current ratio below 1.00 suggests that your business may struggle to cover short-term obligations. This perceived risk often results in higher premiums or even outright denial of coverage.

Additionally, weak working capital usually means lower credit limits. Insurers base these limits on your financial stability, so if your cash conversion cycle is too long, it signals that your cash is tied up and liquidity is tight.

"The creditworthiness of your business determines the level of risk they [insurers] are willing to accept."

– FasterCapital

Insurers also keep an eye out for practices like factoring and reverse factoring, which can artificially inflate your cash position. These tactics often lead to closer scrutiny of your actual liquidity.

How Strong Working Capital Improves Insurance Terms

On the flip side, strong working capital can work in your favor. Businesses with solid metrics are typically seen as lower risk, allowing them to secure lower premiums. A current ratio in the 1.20 to 2.00 range signals efficient asset management and reassures insurers that your business can meet its obligations.

With strong working capital, you can also access higher coverage limits. Insurers use your financial health to determine the maximum amount they’ll indemnify, so a robust cash position gives you more flexibility, especially if you’re expanding into new markets or offering extended payment terms to attract larger clients.

"A strong credit rating can lead to better insurance terms and lower premiums."

– FasterCapital

There’s an added bonus: banks often view insured receivables as lower-risk collateral. This means that pairing strong working capital with trade credit insurance can improve your borrowing terms and even reduce interest rates. In this way, maintaining healthy working capital not only helps with insurance but also strengthens your overall financial stability.

| Metric | Formula | Insurer Interpretation |

|---|---|---|

| Current Ratio | Current Assets ÷ Current Liabilities | 1.5–2.0 is healthy; <1.0 indicates liquidity risk |

| Cash Conversion Cycle | DIO + DSO – DPO | Shorter cycles indicate efficient cash generation |

| Net Working Capital | Current Assets – Current Liabilities | A positive value indicates a buffer for unexpected expenses |

| Quick Ratio | (Current Assets – Inventory) ÷ Current Liabilities | Measures the ability to meet short-term obligations with liquid assets |

Improving Working Capital to Strengthen Trade Credit Insurance Coverage

Once you know how insurers assess your working capital, the next step is taking practical measures to improve it. A stronger financial position not only appeals to insurers but can also help you secure better coverage terms and potentially lower premiums.

Better Cash Flow Management

Managing cash flow effectively is a key step in strengthening your working capital. One way to do this is by shortening your cash conversion cycle – the time it takes to turn inventory into cash. A quicker cycle means more liquidity for your business.

For instance, you could negotiate longer payment terms with suppliers. Shifting from Net 30 to Net 60 terms allows you to hold onto cash longer while maintaining good relationships with your vendors. Another option is adopting just-in-time (JIT) inventory practices, which reduce the amount of cash tied up in unsold goods.

To speed up cash inflows, consider offering early payment discounts to customers. This is especially important given that late payments impact over 50% of small and medium enterprises (SMEs) and contribute to roughly 25% of business failures. Proactive cash flow management can make a significant difference.

"Cash flow is the life blood of any business and is the primary indicator of business health."

– Atradius

Streamlining your invoicing process can also help improve liquidity, ensuring payments are received on time.

Lowering Day Sales Outstanding (DSO)

Lowering your Day Sales Outstanding (DSO) is another way to strengthen working capital. A lower DSO means quicker conversion of accounts receivable into cash, which insurers view as a sign of efficient credit management and lower risk.

Start by invoicing immediately upon delivery. Combine this with automated invoicing and reminders to reduce errors and ensure customers are notified promptly. A simple yet effective tactic is calling customers on the delivery day to confirm receipt and address any potential payment issues upfront.

You can also set up automatic holds on new orders for customers who exceed payment terms. For example, if your terms are Net 30, place a hold at 60 days to limit further credit exposure. Additionally, establish clear credit policies for extending terms, such as requiring no negative public records and a minimum of two years in business ownership.

With nearly one-third of U.S. small business owners waiting over 30 days for payments, these strategies can give you an edge in managing receivables effectively.

"The lower the DSO you can offer, the better cash flow will be as those receivables turn around quicker."

– Atradius

Using Accounts Receivable Insurance for Risk Protection

To complement these cash flow strategies, consider protecting your receivables with Accounts Receivable Insurance. This type of insurance safeguards your working capital by covering cash flow gaps caused by customer non-payment. Policies typically cover between 75% and 95% of the invoice amount in such cases.

Beyond the direct protection, Accounts Receivable Insurance provides access to buyer creditworthiness databases, helping you set safer credit limits. It also includes professional debt collection and legal services, which can reduce operational costs. Additionally, insured receivables are often viewed as secure collateral by banks, potentially leading to larger credit lines and better borrowing terms. This added security not only protects your working capital but also supports your business’s growth.

"By using trade credit insurance to defend accounts receivables and manage credit risk, business can position themselves as lower risk investments for lenders."

– Marsh Commercial

Despite these advantages, only about 2% of SMEs currently utilize trade credit insurance coverage.

How Working Capital Shapes Policy Design and Coverage

Your working capital doesn’t just determine whether you qualify for trade credit insurance – it also plays a key role in shaping policy structure, coverage limits, and premium costs. Insurers use your working capital metrics to tailor policies that align with your financial health and risk profile.

Setting Policy Limits Based on Working Capital

Insurers rely on your working capital data to establish preset credit limits for your customers. Companies with strong working capital and effective credit controls often qualify for discretionary limit systems. These systems let you manage credit up to a set threshold without needing individual approvals for each customer.

However, if your business depends heavily on a single customer, insurers may enforce stricter limits or even partial exclusions. Payment terms also factor in – longer terms, such as 60–90 days, are seen as riskier than 30-day terms, which can lead to lower coverage limits.

For small to mid-sized businesses with a handful of high-value clients, a Named Buyer Policy can be a cost-effective solution. This type of policy focuses on insuring your most critical or high-risk accounts and can reduce premiums by as much as 50%, all while maintaining essential protection. These customized limits directly influence your premium costs.

How Working Capital Affects Premium Costs

Premiums are typically calculated using a Rate-on-Turnover (ROT) model, which ranges from 0.05% to 1.0% for U.S. businesses. Where you fall within this range depends heavily on the health of your working capital.

- Low-risk businesses – those with high turnover, diverse customer bases, and short payment terms (30 days or less) – generally pay between 0.05% and 0.2%.

- High-risk businesses – those with fewer customers, longer payment terms (60 days or more), and exposure to emerging markets – can expect rates between 0.8% and 1.0%.

For example, a mid-sized exporter with $1.5 million in turnover and strong working capital might pay $4,500 annually at a 0.30% rate. Meanwhile, a small business with $100,000 in turnover and weaker financial metrics might face a 0.90% premium, equating to $900.

"Implementing and effectively managing trade credit exposure plays a pivotal role in stabilizing a company’s financial health, by protecting its balance sheet and maintaining its operational efficiency." – Michael Creighton, WTW

Coverage Differences for Domestic and International Trade

Working capital also impacts the type of coverage you can secure for domestic versus international trade. Domestic trade typically comes with lower premium rates, around 0.25%–0.30%, since it primarily addresses risks like commercial insolvency and defaults. On the other hand, international trade – especially in emerging markets – often has rates of 0.60% or higher due to added risks like political instability, currency controls, and cross-border disputes.

Providers like Accounts Receivable Insurance specialize in creating policies tailored to your working capital and trade environment. For businesses with limited working capital, flexible options such as single invoice coverage can protect individual high-value transactions instead of your entire ledger. By managing working capital effectively, as discussed earlier, businesses can secure better terms across all types of coverage.

Conclusion

Key Points

Working capital isn’t just a number on your balance sheet – it plays a crucial role in shaping your trade credit insurance. Insurers evaluate metrics like your current ratio (ideally between 1.20 and 2.00) and Day Sales Outstanding (DSO) to determine your eligibility, set credit limits, and calculate premiums. Businesses that manage their working capital effectively often secure better terms and coverage.

Strong cash flow management has a direct impact on your insurance coverage. By reducing your cash conversion cycle and lowering DSO, you minimize the uncertainty insurers face when assessing your risk profile. This can lead to higher indemnity limits – typically covering 75% to 95% of invoice amounts – while strengthening your financial position overall.

Additionally, Accounts Receivable Insurance not only protects your receivables from non-payment but also enhances your borrowing power. Banks are more likely to view insured receivables as low-risk collateral, making it easier to secure larger credit lines or better financing terms. This creates a cycle of improvement: better working capital management leads to improved insurance terms, which then supports greater financial stability.

Next Steps for Your Business

Start by auditing your working capital. Calculate your current ratio, net working capital, and DSO. For context, nearly one-third of U.S. small business owners experience payment delays exceeding 30 days, and late payments contribute to 25% of business failures. Addressing these issues now can help you avoid significant cash flow challenges in the future.

Consider connecting with Accounts Receivable Insurance for a tailored risk assessment. Their experts can help you design a policy that aligns with your working capital needs, ensuring your receivables are protected and positioning your business for long-term growth.

FAQs

What working capital numbers do insurers want to see?

Insurers pay close attention to working capital metrics like a solid current ratio and consistent positive cash flow. These metrics highlight a company’s ability to handle short-term financial obligations and maintain enough liquidity. For insurers, this is key to evaluating a business’s financial health and understanding its capacity to manage potential risks effectively.

Can trade credit insurance help me get better bank financing?

Yes, trade credit insurance can help you secure better financing from banks. By safeguarding your accounts receivable, it lowers the risk for lenders, turning insured receivables into reliable collateral. This can result in higher credit limits, lower interest rates, and more flexible terms. Plus, it boosts your financial stability, making you more attractive to lenders and opening doors to better financing opportunities.

How can I quickly improve DSO before applying for coverage?

To bring down your Days Sales Outstanding (DSO) quickly before applying for trade credit insurance, prioritize proactive management of accounts receivable. Start by establishing clear credit policies to set expectations upfront. Regularly review your customers’ creditworthiness to identify potential risks early. Using automation tools to track overdue accounts can streamline the process and ensure nothing slips through the cracks. Additionally, consider implementing auto-hold procedures for customers with late payments – this can help reduce collection delays and improve overall cash flow.