When a foreign buyer fails to fulfill their payment obligations, your business can face serious challenges like disrupted cash flow and operational strain. Non-performance in export contracts often stems from commercial issues (e.g., bankruptcy, bad faith) or political factors (e.g., war, sanctions). While export credit insurance can cover 90-100% of losses, the reimbursement process can be time-consuming.

Key Takeaways:

- Prevent Problems: Conduct thorough credit checks, draft clear contracts, and verify compliance before signing agreements.

- Common Risks: Financial (nonpayment, insolvency), operational (supply chain issues), and political/legal (sanctions, regulatory changes).

- Risk Management: Monitor buyer behavior, maintain communication, and use export credit insurance to protect cash flow.

- Handling Breaches: Document issues meticulously, explore legal remedies, and leverage insurance for recovery.

Being prepared and staying vigilant can protect your business from costly defaults while maintaining competitiveness in global markets.

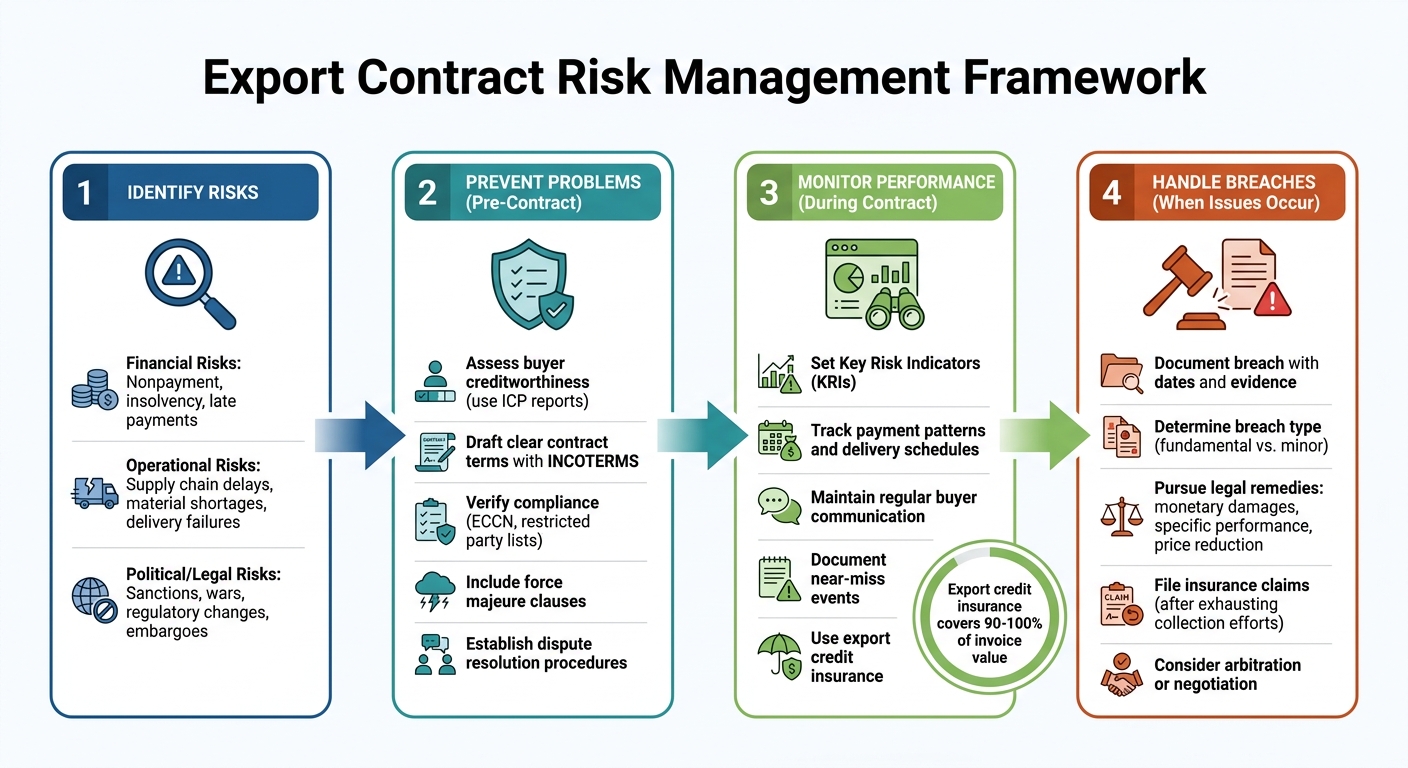

Export Contract Risk Management: 4-Stage Framework for Preventing Non-Performance

How to manage compliance and risk in a changing global trade landscape

sbb-itb-2d170b0

Common Risks in Export Contracts

Export contracts come with a mix of financial, operational, and political-legal risks that can throw even the most carefully planned transactions off track. Knowing these risks – specific to regions, industries, and contract structures – can help safeguard your business.

Financial Risks

The biggest financial threat? Buyer nonpayment. When a foreign customer doesn’t pay for your goods or services, you’re left holding an unpaid invoice and absorbing additional costs. This problem worsens with commercial insolvency – when a buyer suddenly declares bankruptcy, they may no longer be legally obligated to pay .

Late payments are another challenge. They can disrupt cash flow, making it harder to fund production. According to the U.S. Commercial Service, collecting overdue payments in international trade is far more complex and expensive than dealing with domestic defaults. Often, you’ll need to exhaust every reasonable collection effort before insurance claims can even be considered .

But financial risks are just one piece of the puzzle. Operational challenges can also jeopardize contract fulfillment.

Operational Risks

Supply chain hiccups – like port delays, material shortages, or labor strikes – can cause delivery failures, putting you in breach of contract. These risks go beyond logistics. For example, in 2025, U.S. export controls on semiconductors and China’s restrictions on rare earth materials disrupted global manufacturing contracts almost immediately.

Policy changes have led to overnight changes to material pricing, availability, and delivery timelines in the most-affected industries,

as Christopher J. Walsh and Aaron R. Fenton from McLane Middleton explain.

Even when delivery is still possible, economic factors can make fulfilling a contract unfeasible. A sudden tariff, for instance, might not stop shipment but could turn a profitable deal into a losing one. Companies that scramble to find replacement suppliers during such disruptions often face additional fallout. Walsh and Fenton highlight the risks of rushing these decisions:

A company that shortcuts diligence in favor of haste can find itself suffering the consequences, including indemnity claims against suppliers, rescission or price-reduction demands, and reputational harm.

Operational risks are tough, but external political and legal events can be even more unpredictable.

Political and Legal Risks

Geopolitical upheavals – like wars, sanctions, or sudden regulatory shifts – can bring contracts to a halt. These events can freeze assets, block payments, or collapse supply chains overnight . A striking example occurred in February 2026, when a Hong Kong-based company filed arbitration against Panama after losing its port concession. This case underscores how quickly state actions can strip businesses of their rights to perform under contracts.

Political risks, such as new export controls or embargoes, can also make shipping goods or importing materials legally impossible. Duncan Speller and his team at Duane Morris LLP emphasize the importance of preparation:

Unpredictable geopolitical developments have created risk for commercial parties… it is more important than ever for commercial parties to be proactive in planning for and mitigating that risk.

Deals involving buyers in politically unstable regions – or under fluctuating U.S. trade policies – carry significantly higher exposure to these risks.

Risk Mitigation Before Signing Contracts

Taking the time to prepare thoroughly before signing a contract can reduce risks and open up more options for resolving potential issues. Exporters can protect themselves by carefully evaluating buyers, drafting precise contract terms, and ensuring compliance with relevant regulations. These steps build on earlier risk assessments and lay the groundwork for effective performance management.

Assessing Buyer Creditworthiness

Understanding a buyer’s creditworthiness is a critical step in minimizing non-payment risks. Before extending credit, evaluate the buyer’s financial stability. Tools like the U.S. Commercial Service’s International Company Profiles (ICPs) provide detailed financial data and list other U.S. companies that have worked with the buyer, giving you a chance to check their payment history.

If you’re dealing with buyers in high-risk markets, consult banking professionals for additional insights. For existing clients, watch for signs of trouble, like late payments or changes in payment patterns – these could indicate potential risks. Based on your findings, decide whether to offer open-account terms or opt for more secure methods like cash in advance or letters of credit. Even for seemingly secure payment methods, it’s wise to conduct thorough credit checks.

Writing Clear Contract Terms

Ambiguity in contracts often leads to disputes. As James Holbein from Braumiller Law Group notes:

In the complex world of commercial international trade, contracts serve as the foundation for successful transactions.

Your contract should clearly outline remedies for non-performance, including penalties, dispute resolution procedures, and realistic delivery schedules. Establish a "hierarchy of terms" to ensure specific provisions override generic ones. Using INCOTERMS can clarify responsibilities for shipping, insurance, delivery, and storage. Additionally, detailed payment terms – covering schedules, triggers, currency, and invoicing – can help prevent misunderstandings or non-payment. Don’t forget to include a force majeure clause to address unexpected events and specify whether disputes will be handled through arbitration or litigation.

Verifying Compliance Requirements

Before finalizing any contract, screen buyers against U.S. restricted and denied party lists using tools like RPS. Identify the correct Export Control Classification Number (ECCN) or ITAR category for all items, whether they are goods, software, or technical data. Request this information from your manufacturer early in the process. Even items classified as EAR99 may require compliance measures if they involve sensitive technologies like semiconductors or confidential technical data.

Additionally, review the Country Limitation Schedule to check for any political or commercial restrictions related to the buyer’s country. For transactions involving sensitive technology, consider creating a Technology Control Plan (TCP) or Risk Mitigation Plan (RMP) to document your compliance efforts and internal procedures.

Managing Risks During Contract Performance

After the contract is signed, the focus shifts to keeping everything on track through continuous performance monitoring and clear communication with your buyer. Even with a solid contract in place, consistent oversight is essential to ensure compliance. Below, we explore methods for tracking performance and how export credit insurance can protect your operations.

Monitoring and Communication

Monitoring performance effectively begins with setting up Key Risk Indicators (KRIs) – specific metrics designed to track progress and flag issues when certain thresholds are exceeded. Assigning a dedicated risk owner to each key risk ensures accountability and a quick response when needed. As MetricStream aptly puts it:

Risk mitigation is not a ‘set it and forget it’ process.

It’s also important to document near-miss events and minor incidents, as these can reveal patterns that may indicate emerging risks. Regularly screen your exports to maintain compliance with regulations. Keep a close eye on your buyer’s payment habits – late payments or deviations in their usual payment schedule can hint at financial trouble. Use clear invoicing forms with specific due dates to simplify this process.

Communication plays a big role in avoiding misunderstandings. Use standardized language to ensure everyone interprets contract terms the same way. Check regularly that billing and delivery addresses are accurate, and keep thorough records of all risk management efforts to stay prepared for audits. If changes to the contract are necessary, document them meticulously with tracked changes for clarity.

Using Export Credit Insurance

Export credit insurance can cover 90% to 100% of your invoice value, providing a safety net for your cash flow while enabling you to offer competitive open-account terms to foreign buyers. This type of insurance protects against both commercial risks – like a buyer declaring bankruptcy – and political risks, such as war or civil unrest.

For tailored solutions, Accounts Receivable Insurance (https://accountsreceivableinsurance.net) offers policies designed to fit your specific needs. Whether you want to insure your entire export portfolio, a particular group of buyers, or just one high-value client, their services include risk evaluations, claims handling, and access to a global network of credit insurers.

Insured receivables can also strengthen your financial position. They can be used as collateral to secure loans, unlocking additional working capital to keep your operations running smoothly. Many policies operate on a pay-as-you-go basis, meaning premiums are only due after shipments are made. To make the most of export credit insurance, monitor buyer behavior and political developments regularly, adjusting your coverage as needed.

Handling Non-Performance Events

Taking quick and organized action when non-performance occurs can help shield your business from further losses. Start by documenting the breach thoroughly, then explore legal or insurance options to recover damages.

Identifying and Recording Non-Performance

First, determine the type of breach. Is it a "fundamental non-performance"? This happens when the breach significantly deprives you of what the contract promised. For example, if a supplier fails to deliver goods that are critical to your operations, this could qualify as fundamental. Contracts often include clauses stating that time is "of the essence", meaning even minor delays could be considered a breach. Imagine a shipment due on March 15, 2026, still undelivered by April 23 – that delay may justify terminating the contract.

Also, consider external factors like force majeure events (e.g., embargoes or destruction of goods) that might excuse the breach . If you suspect future non-performance – such as a buyer hinting they can’t pay – request assurances of performance and pause your own obligations until you receive confirmation.

Keep meticulous records of any deviations from the contract. As Hall Ellis Solicitors explains:

any deviation from the contractual obligations will amount to a breach of contract.

Record missed deadlines, shipment discrepancies, quality issues, or payment delays with precise dates and supporting evidence. These records will be crucial as you move forward with legal remedies or insurance claims.

Legal Remedies and Insurance Claims

Once you’ve documented the breach, you can explore several options to address the issue. Monetary damages can cover lost profits, direct financial losses, and incidental expenses caused by the breach . If financial compensation isn’t enough, you might seek specific performance, which forces the other party to fulfill their contractual duties .

Under the UN Convention on Contracts for the International Sale of Goods (CISG), you could also request a price reduction if the goods don’t meet agreed specifications. For fundamental breaches, termination or rescission of the contract may be the best course of action. However, this requires formal notice, as

the right of a party to terminate the contract is exercised by notice to the other party.

Make sure to issue this notice promptly after identifying the breach.

If your contract includes liquidated damages clauses – pre-determined sums for specific breaches – these can provide a straightforward remedy without lengthy disputes .

Insurance can also play a significant role. Export credit insurance, for example, can cover up to 100% of your invoice value in cases of commercial risks (like buyer insolvency) or political risks . However, as Export.gov points out:

the exporter must exhaust all reasonable means of obtaining payment before an insurance claim will be honored.

This means you’ll need to document your collection efforts, formal notices, and the event that led to non-payment.

Services like Accounts Receivable Insurance can guide you through the claims process, ensuring compliance with policy requirements and proper documentation. They can also help you prove that the non-payment stemmed from covered risks. With timely filing and thorough records, you can recover most of your losses while still pursuing legal remedies if necessary. In many cases, direct negotiation or international arbitration – such as through the International Chamber of Commerce – can resolve disputes faster and more affordably than litigation.

Conclusion

Taking a proactive approach to risk management can help you avoid costly defaults. Start by conducting thorough credit checks on foreign buyers, drafting clear contracts with Incoterms to outline costs and risks, and ensuring all compliance requirements are met before signing any agreements.

Once agreements are in place, focus on maintaining strong pre-contract practices and continuous monitoring. Keep communication lines open and regularly assess the financial health of your partners. Insurance can play a key role here, protecting your cash flow and allowing for better credit terms. If a breach occurs, document everything carefully – include specific dates and detailed evidence. Then, act promptly by negotiating, pursuing arbitration, or filing claims as necessary.

Accounts Receivable Insurance can support you throughout this process. From customizing policies to fit your export portfolio to managing claims and ensuring proper documentation, they provide valuable assistance every step of the way. By combining proactive evaluations, vigilant monitoring, and swift responses, you can strengthen your defenses against export non-performance. This steady approach not only safeguards your business but also helps you maintain a competitive edge and financial stability in the global market.

FAQs

What early warning signs suggest a foreign buyer may not pay?

Delays in payments, abrupt changes in payment habits, or trouble verifying a buyer’s financial health can all serve as early warning signs. It’s crucial to research the buyer’s financial stability, review their transaction history, and assess their reliability in imports before committing to a contract. Keeping an eye on these factors allows you to spot risks early and take proactive steps to reduce the chances of non-payment.

What contract clauses best protect me if a buyer defaults or delays?

Key contract clauses can help shield you from buyer defaults or delays. Start with payment terms – these should clearly outline payment schedules, due dates, and accepted payment methods. To encourage timely payments, include late payment penalties, which can act as a deterrent for delays.

For added protection, define remedies for non-performance. These might include suspending deliveries or, in extreme cases, terminating the contract entirely. If you’re looking for financial security, consider incorporating surety bonds or payment bonds as guarantees to minimize risks tied to non-performance.

What documents are required to file an export credit insurance claim?

When filing an export credit insurance claim, you’ll need to gather specific documents to confirm the transaction and the buyer’s responsibility. These typically include the international purchase order, proof of export (like a third-party bill of lading), and other relevant shipping paperwork. It’s also important to electronically report overdue accounts or payment defaults through your insurer’s platform. Double-check that all documents are accurate and fully completed to help streamline the claims process.