Smart contracts are transforming insurance claims by automating processes, improving accuracy, and reducing costs. Here’s what you need to know:

- What are smart contracts? Self-executing agreements on a blockchain that trigger actions (like payouts) when specific conditions are met.

- How do they work? They rely on "if/then" logic, external data sources (oracles), and automation to handle claims faster and more transparently.

- Benefits:

- Cut claim processing times from weeks to hours.

- Reduce errors to less than 1%.

- Lower administrative costs by up to 60%.

- Combat fraud, reducing fraudulent claims by 30–40%.

- Real-world examples:

- A hospital network reduced claim approvals from 7 days to 48 hours.

- A travel insurer cut costs per policy by 73% using smart contracts.

- Trade credit insurance automates payouts for missed payments or insolvencies.

Smart contracts are reshaping how insurers and businesses handle claims, offering faster payouts, better accuracy, and cost savings. By integrating with existing systems and addressing challenges like data reliability and security, this technology is creating a more efficient future for insurance claims.

How Smart Contracts Will Change Insurance FOREVER

sbb-itb-2d170b0

What Are Smart Contracts?

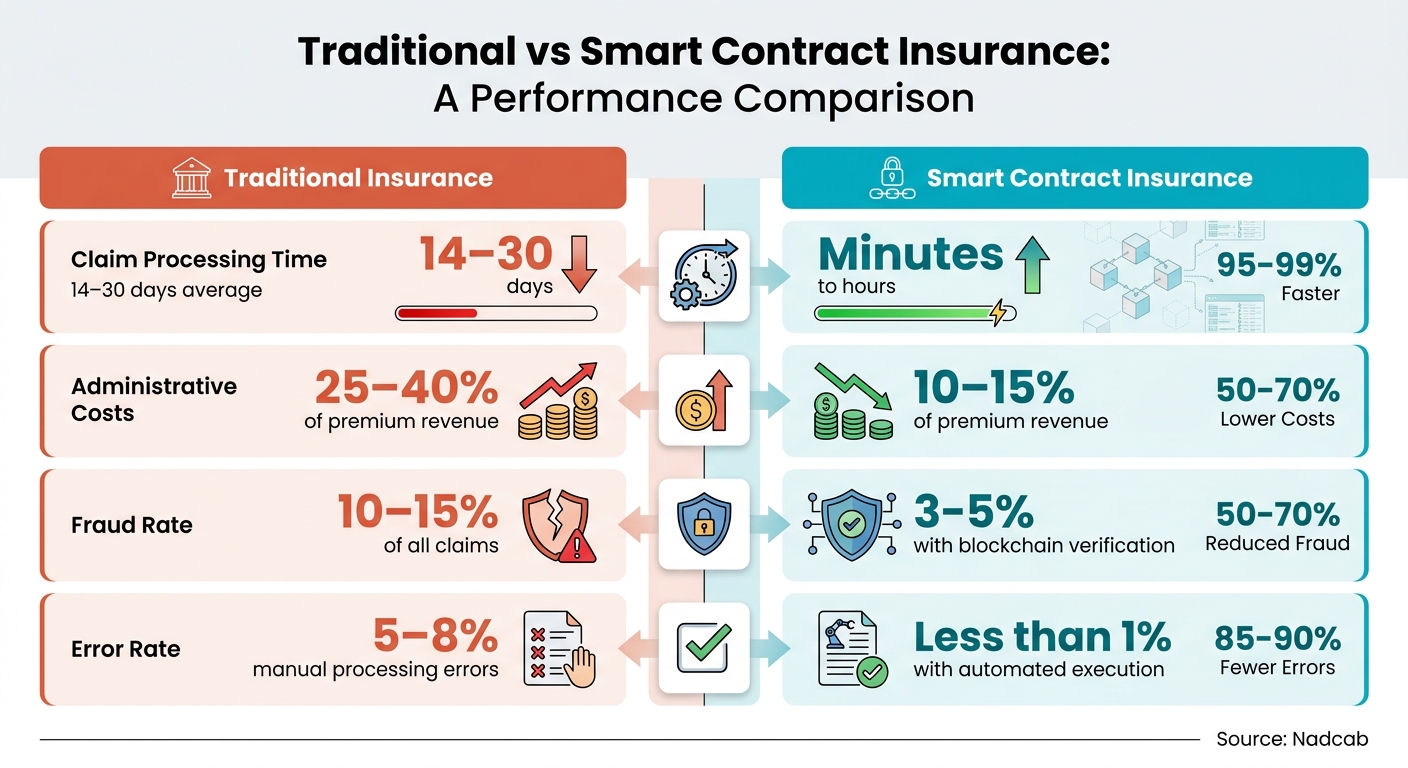

Traditional vs Smart Contract Insurance Claims Processing Comparison

A smart contract is a self-executing digital agreement stored on a blockchain. Instead of relying on paper documents or manual processes, the terms of the agreement are written directly into code. Once the specified conditions are met, the contract automatically carries out the agreed-upon action, such as issuing a payment.

These contracts operate using "if/then" logic. For example, if a specific event like a flight delay or a weather incident occurs, the smart contract automatically triggers a response – no human intervention required. This eliminates the need for manual claims processing, paperwork, and subjective judgments.

"Insurance is fundamentally rule-based. If X happens… then Y should happen… That’s exactly what a smart contract does – ‘if this, then that,’ automated, no human decision." – Domi Petocz, AI and Blockchain Department Lead, Interexy

Once a smart contract is deployed on a blockchain, it becomes unchangeable. Neither the insurer nor the policyholder can modify the terms after the fact. This tamper-proof design ensures that the contract is carried out exactly as written, reducing the chances of disputes. Every action, from policy creation to payout, is recorded on a decentralized ledger that is visible to all authorized parties. This creates a transparent and permanent record, ensuring trust and clarity in the process.

How Smart Contracts Work

Here’s how smart contracts function, step by step:

- Encoding Policy Terms: The policy details – such as coverage terms, premiums, and trigger conditions – are programmed into the contract and uploaded to the blockchain. The contract becomes active once the premium payment is confirmed.

- Data Input via Oracles: Since blockchains cannot directly access external information, smart contracts rely on "oracles." These are secure systems that provide real-world data, such as weather updates, flight statuses, or payment confirmations, to the blockchain. Oracles continuously monitor conditions and feed verified data to the contract.

- Trigger Activation: When the data from the oracle matches the contract’s trigger conditions, the smart contract calculates the payout amount.

- Automated Payout: The contract then transfers the payout directly to the policyholder’s digital wallet without any manual steps.

For instance, a European travel insurer adopted smart contracts in 2025 and saw incredible efficiency improvements. By automating claims for 10,000 annual policies, the company reduced its staff from 8 employees to just 2. Administrative costs dropped from $45 per policy to $12 – a 73% decrease. Plus, claims that once took 15–20 days to process were settled in under 4 hours.

Why Blockchain Improves Claims Processing

The effectiveness of smart contracts is rooted in blockchain’s strengths. A distributed ledger provides a permanent, time-stamped record of every policy term, event, and payout. This transparency minimizes disputes – when all parties have access to the same unchangeable records, disagreements over coverage or eligibility become rare.

Blockchain also helps combat fraud. For example, carriers can quickly verify whether an asset has been involved in multiple claims, reducing opportunities for duplicate filings. Studies show that blockchain-based systems can cut insurance fraud by 30–40%, with some automated setups achieving fraud reductions as high as 80%. Additionally, the automated nature of smart contracts reduces processing errors to less than 1%, compared to 5–8% in manual systems.

| Metric | Traditional Insurance | Smart Contract Insurance |

|---|---|---|

| Claim Processing Time | 14–30 days average | Minutes to hours |

| Administrative Costs | 25–40% of premium revenue | 10–15% of premium revenue |

| Fraud Rate | 10–15% of all claims | 3–5% with blockchain verification |

| Error Rate | 5–8% manual processing errors | Less than 1% with automated execution |

Source: Nadcab

This combination of automated execution and blockchain’s secure record-keeping has led to what insurers call "zero-touch claims." For industries like trade credit and Accounts Receivable Insurance, this means faster payouts when customers default and more reliable cash flow for businesses managing credit risks.

Benefits of Smart Contracts in Claims Processing

Smart contracts are changing the game for insurers by improving speed, accuracy, and cost efficiency in claims processing. Companies using this technology are already experiencing noticeable advancements in these areas.

Faster Claims Resolution

Speed is a standout advantage. Traditional claims processing often involves lengthy steps like filing paperwork, manual reviews, and multiple approval layers – taking anywhere from 14 to 30 days. Smart contracts, however, reduce this timeline to mere minutes or hours by automating the entire process. This is achieved through straight-through processing (STP), which handles routine claim verifications and payments without human intervention.

Here’s how it works: when a triggering event occurs – like a flight delay or a car accident detected by sensors – oracles provide verified real-world data. The smart contract checks this data against the policy terms, calculates the payout, and transfers the funds directly to the policyholder’s digital wallet.

In auto insurance, for example, smart contracts have tripled the speed of claims processing. A remarkable case is the Lemonade Foundation‘s initiative launched in 2022. Using smart contracts on the Avalanche blockchain and weather oracles, they introduced automated climate insurance for African farmers. This system delivers instant payouts based on real-time weather data, bypassing the need for claims adjusters.

"By using a DAO instead of a traditional insurance company, smart contracts instead of insurance policies, and oracles instead of claims professionals, we expect to… deliver affordable and instantaneous climate insurance to the people who need it most." – Daniel Schreiber, Director, Lemonade Foundation

Reduced Errors and Fraud

Smart contracts don’t just speed things up – they also reduce errors and fraud. Traditional claims processes have error rates of 5–8%, but encoding policy terms directly into smart contracts lowers this rate to under 1%.

Fraud, which costs the U.S. economy over $40 billion annually in non-health insurance alone, is another area where smart contracts excel. They combat fraud through shared ledgers, which prevent duplicate claims by verifying whether an incident has already been reported. Additionally, oracle-based verification uses objective third-party data – like weather reports, flight statuses, or IoT sensor data – to trigger payouts, reducing reliance on self-reported claims.

The impact is significant: blockchain technology can cut insurance fraud by 30–40%. Insurers using smart contracts have seen fraudulent claims drop by 65–75%, saving $8–12 million annually for mid-sized companies. Fraud rates, which typically range from 10–15% in traditional systems, fall to just 3–5% with blockchain verification.

Lower Costs and Better Efficiency

Automation through smart contracts also slashes costs. Administrative expenses in traditional systems often consume 25–40% of premium revenue, but smart contracts reduce this to 10–15%. Similarly, Loss Adjustment Expenses (LAE) – the costs of investigating and settling claims – typically account for 12–15% of an insurer’s premium income. For simple, high-volume claims, manual processing can even cost more than the claim itself. Smart contracts solve this issue with zero-touch resolution.

By automating claims, insurers can cut administrative costs by up to 60% and significantly reduce LAE. For example, a European travel insurer that adopted smart contracts in 2025 reduced administrative costs from $45 per policy to just $12 – a 73% drop – while managing 10,000 annual policies with only two employees instead of eight.

"Operational costs decrease by up to 60% when insurers implement smart contract automation, eliminating redundant administrative tasks and streamlining policy management workflows." – Nadcab Labs

Faster claims settlements also improve capital efficiency. When payouts happen in hours instead of weeks, insurers can free up funds for other purposes. This is especially crucial for event-driven or catastrophe coverage, where quick payouts can prevent further financial hardship for policyholders.

Smart Contracts in Trade Credit and Accounts Receivable Insurance

Smart contracts are reshaping the way trade credit and accounts receivable insurance claims are handled. By automating payouts based on clear, predefined credit events – like buyer insolvency or missed payments – these contracts eliminate delays and streamline processes. Two major applications stand out: parametric insurance for trade credit risks and seamless accounts receivable management.

Parametric Insurance for Trade Credit Risks

Parametric insurance uses measurable events to trigger automatic payouts. In the context of trade credit, these events could include a buyer filing for insolvency, a downgrade in their credit rating, or a payment default that exceeds a set threshold. Smart contracts rely on external data sources, known as oracles, to confirm these triggers.

Once the oracle verifies the event, the smart contract executes immediately – no manual intervention required. Funds are transferred directly to the policyholder’s account, cutting settlement times from the typical 7–30 days to an incredible 5–60 minutes.

The cost savings are just as impressive. Traditional claims processing costs insurers $7–$15 per claim, but with smart contract automation, this drops to as little as $0.10–$0.50 per claim. For insurers managing thousands of claims annually, this efficiency can save millions in administrative expenses while ensuring faster payouts and greater transparency.

This same level of automation is also revolutionizing accounts receivable risk management.

Accounts Receivable Risk Management

When it comes to Accounts Receivable Insurance, smart contracts integrate directly with a company’s ERP system. They monitor for payment issues, such as overdue invoices or missed thresholds, and automatically generate a digital claim – eliminating the need for policyholders to file manually.

A real-world example of this innovation took place in June 2019, when Clause, a technology firm, showcased its solution at the Global Insurtech Leaders’ Summit in New York. Clause’s system linked ERP data with insurance policies, enabling it to automatically process claims for buyer defaults. In one demonstration, the smart contract paid out 90% of the loss instantly and updated the accounting systems of both the insurer and the policyholder to reflect accurate cash balances.

"Claims processing, amongst other processes, could be almost completely automated… [Technology] could be used to enforce contract specific rules and offer a reliable and transparent payout mechanism." – National Association of Insurance Commissioners (NAIC)

This level of automation doesn’t just speed up claims. It also keeps the financial records of both the insurer and policyholder in sync throughout the process. Additionally, the reliability of these automated guarantees can help companies secure cheaper debt financing, as their receivables are backed by a more dependable system. With these advancements, the global smart contract insurance market is projected to surpass $9 billion by 2032, driven by the efficiency and reliability these technologies bring.

How to Implement Smart Contracts for Claims Processing

Implementation Steps

Rolling out smart contracts for claims processing involves a series of well-defined steps. Each phase is crucial to creating an efficient and transparent claims system. The first step is to translate your policy terms – like credit limits, insolvency triggers, or non-payment periods – into executable code. This involves formalizing your business rules into a programmable format.

"The most important part – formalization of the insurer’s unique business rules in smart contracts – involves a considerable amount of custom code and requires extensive technology background." – Vadim Belski, Principal Architect, ScienceSoft

Next, choose the right blockchain platform. Public networks like Ethereum or Polygon offer transparency, while private networks such as Hyperledger Fabric or R3 Corda prioritize data privacy and regulatory compliance.

To connect smart contracts with real-world events, integrate decentralized oracles like Chainlink. These oracles provide external data to trigger claims, and using multiple independent sources ensures consensus and eliminates single points of failure.

Security is a top priority. Conduct thorough audits with tools like Slither or MythX to identify weaknesses. Simulate various scenarios, including edge cases and malicious inputs, using frameworks that replicate real-world conditions. Deploy smart contracts incrementally, starting with limited funds and restricted access. Features like circuit breakers can pause operations if issues arise.

Finally, bridge blockchain systems with your existing infrastructure. Middleware and APIs can link smart contracts to underwriting, CRM, and accounting systems, ensuring seamless integration.

Once the system is in place, be ready to tackle some common challenges.

Common Challenges and Solutions

1. Oracle Reliability

Smart contracts rely on oracles to interpret real-world data, but compromised oracle data can lead to errors. To address this, use decentralized oracle networks like Chainlink, incorporating redundancy to ensure reliability.

2. Regulatory Uncertainty

Many regions lack clear rules for blockchain-based insurance. Participating in regulatory sandboxes allows you to test live products under flexible conditions while working toward compliance. Pairing smart contracts with legal agreements also strengthens enforceability.

3. Security Risks

Security vulnerabilities are a significant concern. In the first half of 2025 alone, attackers exploited crypto protocols to steal over $2.17 billion. Reduce risks by using audited libraries like OpenZeppelin for standard functions instead of developing custom code. Implement admin override functions to pause payouts in case of bugs.

4. Data Privacy

Public blockchains can conflict with regulations like GDPR. To navigate this, use permissioned blockchains for sensitive data or store confidential information off-chain, such as on IPFS, while keeping only transaction hashes on-chain.

| Challenge | Proposed Solution |

|---|---|

| Oracle Reliability | Use decentralized oracle networks (e.g., Chainlink) with redundancy. |

| Regulatory Compliance | Participate in regulatory sandboxes and combine smart contracts with legal terms. |

| Data Privacy (GDPR) | Use permissioned blockchains or store sensitive data off-chain securely. |

| Legacy Integration | Employ middleware and APIs to connect blockchain with existing systems. |

| Complex Claims | Combine parametric payouts with manual review for subjective claims. |

Start by focusing on straightforward use cases like logistics disruptions or insolvency events. These objective scenarios allow you to test the technology with minimal risk before moving on to more complex claims. By addressing these challenges head-on, you’ll be better equipped to reduce errors and speed up claims processing, meeting the goals outlined in this guide.

Conclusion

Smart contracts are reshaping claims processing in trade credit and accounts receivable insurance. The numbers speak for themselves, showing faster processing times, reduced costs, and fewer instances of fraud. This marks a major shift in how the industry operates.

Regulators have taken notice, too. The National Association of Insurance Commissioners has acknowledged this shift, stating: "Claims processing, amongst other processes, could be almost completely automated". For businesses, this means quicker access to payouts, seamless integration of claims with accounting systems, and transparent, automated processes triggered by specific events.

The rapid adoption of blockchain technology in insurance is hard to ignore. Companies that begin with straightforward parametric use cases – such as insolvency events or delayed payments – can develop valuable expertise before moving on to more complex applications.

For example, Accounts Receivable Insurance provides customized solutions that can greatly benefit from smart contract automation. As this technology evolves, businesses can explore integrating features like automated execution, oracle-based data feeds, and real-time updates to enhance their insurance coverage.

To maximize these benefits, businesses should focus on incorporating smart contracts into their workflows. Start with simple, objective triggers, ensure contracts align with legal frameworks, and emphasize data accuracy and security. By taking these initial steps, companies can unlock the full potential of automated claims processing. Now is the perfect time to embrace smart contracts and gain a competitive edge through improved efficiency and cost savings.

FAQs

What data do oracles use to prove a claim event happened?

Oracles use verified external data to confirm whether a claim event has taken place. This information might come from Internet of Things (IoT) devices or trusted third-party sources, providing a reliable foundation for claims processing while maintaining clarity and precision.

How do smart contracts handle complex claims that need human judgment?

Smart contracts streamline the claims process by automating actions based on specific rules and triggers, cutting down on manual work. However, for more complicated cases that need a human touch, these contracts flag claims for review to ensure they are handled with care and precision. Oracles, which are reliable data sources, play an essential role by verifying real-world events – like weather conditions or delays – to activate automated responses. This blend of automation for simple claims and human oversight for more intricate ones strikes a balance, delivering both efficiency and clarity.

Can insurers pause or fix a smart contract if a bug is found?

Once deployed, insurers typically can’t pause or directly modify a smart contract because these contracts are designed to be immutable and self-executing. However, some smart contracts are built with upgradable features or use proxy patterns. These allow authorized parties to address bugs or make updates as needed. Without these built-in mechanisms, fixing issues becomes far more challenging. That’s why careful planning during development is essential – this includes conducting thorough audits and, when possible, incorporating upgrade options to maintain both transparency and trust.