Trade credit insurance protects businesses from customer payment defaults, helping stabilize finances and support growth. Here’s how it impacts ROI:

- Premium Costs: Typically 0.1%-0.4% of total sales, premiums are offset by benefits like reduced write-offs, better financing terms, and fewer doubtful accounts.

- Claim Payouts: Policies cover 75%-95% of eligible losses, turning major defaults into manageable events and reducing bad debt expenses.

- Economic Conditions: During downturns, insurance mitigates risks like buyer insolvency and political instability, offering a safety net.

- Coverage Scope: Tailored policies (whole turnover or selective) ensure protection aligns with business needs, reducing exposure and improving recovery rates.

- Better Financing: Insured receivables strengthen collateral, enabling higher advance rates, lower interest margins, and improved cash flow.

Key takeaway: Trade credit insurance not only protects against losses but also strengthens financial stability, improves funding opportunities, and supports business growth.

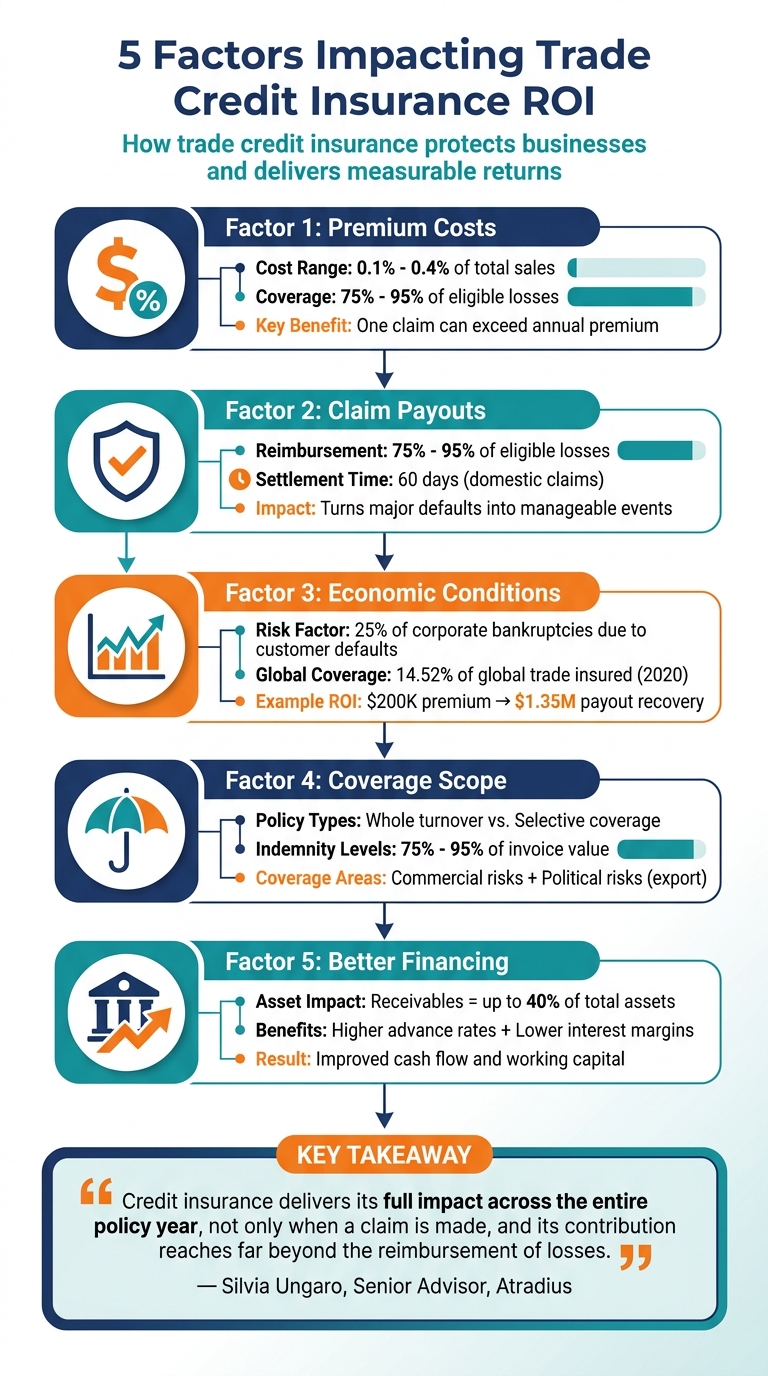

5 Factors Impacting Trade Credit Insurance ROI

1. Premium Costs

Impact on ROI

Premium costs represent the initial outlay, but the return on investment (ROI) comes when claim recoveries, improved financing, and added margins outweigh these costs. Often, even a single claim recovery can surpass the premium for an entire year. For example, if a mid-sized customer defaults, the recovery amount could immediately deliver a positive ROI.

"One unpaid invoice can outweigh the annual premium, so the cover can pay for itself." – Silvia Ungaro, Senior Advisor, Atradius

Cost-Effectiveness

The cost of premiums is influenced by factors like industry stability, customer diversification, geographic risks, and the specific structure of the policy. Industries with lower volatility, a broader customer base, and favorable geographic exposure often see lower premium rates.

To determine if the cost is justified, simulate a stressed loss scenario for your portfolio. Compare the potential financial impact of an uninsured loss to the annual premium. This analysis helps assess the value of your coverage. Additionally, calculate how the policy strengthens your borrowing capacity or lowers funding costs with lenders to identify the broader financial benefits.

But these premiums don’t just protect against losses – they also play a role in reducing risk.

Risk Mitigation Benefits

Beyond recovering losses, the investment in premiums helps reduce doubtful accounts, fortify your balance sheet, and provide access to insurer-led recovery services and buyer insights. Policies typically cover 75% to 95% of eligible losses, with most offering coverage in the 80% to 90% range.

This enhanced risk management can also open doors for expanding your business.

Business Growth Support

Investing in premiums supports growth by enabling higher credit limits and facilitating entry into new markets. This can lead to improved gross margins and faster cash flow throughout the year.

"The cost is outweighed by protection against customer defaults and the ability to grow with confidence." – Kirk Elken, Co-founder, Securitas Global Risk Solutions

sbb-itb-2d170b0

2. Claim Payouts and Recovery Rates

Impact on ROI

Claim payouts directly translate into a return on investment (ROI) for your insurance. If a customer defaults, the policy typically reimburses between 75% and 95% of the eligible loss, turning what could have been a major financial setback into a more manageable situation. Even a single large claim can easily outweigh the cost of your premiums. This reimbursement plays a critical role in safeguarding your balance sheet.

"A claim turns a serious loss into a controlled event and protects the business from financial disruption." – Silvia Ungaro, Senior Advisor, Atradius

These payouts not only cover losses but also simplify financial operations, offering businesses a safety net during challenging times.

Cost-Effectiveness

Beyond the immediate ROI, claim payouts enhance cost-efficiency by reducing bad debt expenses. Insurers often provide professional recovery teams that handle collections more effectively than in-house efforts. This can significantly shorten the cash conversion cycle. For domestic claims, the settlement process is typically completed within 60 days. However, it’s important to note that insurers won’t pay claims on invoices under dispute – such disputes must be resolved before the claim is processed. To ensure eligibility, businesses should maintain accurate documentation and follow clean delivery processes.

Business Growth Support

Reliable claim payouts do more than just offset losses – they also support growth. With the security of insurance, businesses can confidently extend higher credit limits to existing customers and offer net terms to new, higher-risk buyers. Additionally, banks often regard insured receivables as stronger collateral, resulting in higher advance rates and lower interest margins on financing. This improved access to liquidity provides the financial stability needed to grow without taking on unnecessary risk.

3. Economic Conditions

Impact on ROI

Economic ups and downs make trade credit insurance more valuable than ever. When inflation spikes, supply chains falter, or commodity prices swing wildly, the risk of buyer insolvency increases – and that’s where your policy steps in. In fact, customer defaults and insolvencies are responsible for 25% of all corporate bankruptcies. These risks tend to amplify during economic downturns, making protection critical.

Trade credit insurance can also give you a leg up on your competitors. While others may tighten credit terms in uncertain times, your coverage allows you to maintain or even extend payment terms. This flexibility can help you capture more market share. For export businesses, economic instability often brings political risks like currency issues or government interference. The good news? Most export policies cover these scenarios too.

"Trade credit insurance is worth considering if facing uncertain economic times… it provides stability, making it easier to weather bad times." – Ari Global

In short, while economic shifts may increase risks, they also highlight the value of having a policy in place.

Cost-Effectiveness

Premiums for trade credit insurance often shift with economic conditions. Insurers rely on actuarial models that incorporate sector trends and broader economic forecasts. When volatility is high, premiums may rise, but the protection becomes more worthwhile as the likelihood of claims increases. For instance, in 2020, about 14.52% of global trade was safeguarded by trade credit insurance.

During tough economic periods, higher premiums make sense. Take the example of a distributor with $100 million in revenue: they might pay $200,000 in premiums but secure a $1.35 million payout following a customer default. Beyond immediate financial protection, trade credit insurance also supports compliance with IFRS 9 regulations. By replacing buyer risk with the insurer’s stronger credit rating, it lightens the "Expected Credit Loss" burden on your balance sheet.

Risk Mitigation Benefits

One of the hidden strengths of trade credit insurance is the insurer’s ability to monitor economic trends in real time. This keeps you ahead of potential risks, enabling you to adjust credit limits before defaults occur. It’s especially valuable for industries prone to commodity price fluctuations or sudden demand changes.

"Companies exposed to commodity cycles, supply chain shocks, or rapid demand swings benefit from the resilience that insurance provides." – Silvia Ungaro, Senior Advisor, Atradius

For businesses heavily reliant on a few key accounts, insurance becomes a lifeline during uncertain times. A single default from a major customer could spell disaster, but with insurance, you turn that threat into a manageable, predictable cost.

Business Growth Support

Trade credit insurance doesn’t just protect your bottom line – it can also help you grow. Banks often see insured receivables as better collateral, which can make securing loans easier and on more favorable terms. Additionally, having this safety net allows you to confidently enter new markets or extend credit to new customers while others are scaling back. This puts you in a strong position to grow when the economy stabilizes.

4. Coverage Scope and Limits

Impact on ROI

Coverage scope plays a key role in shaping your return on investment (ROI), building on factors like premium costs and claim recovery. The type of policy you choose can make a big difference. For instance, whole turnover policies protect your entire portfolio of buyers, offering broad coverage and easier management. On the other hand, selective policies focus on high-risk accounts, which can help reduce premium costs. Indemnity levels are another critical factor – most policies reimburse between 75% and 95% of the invoice value. A higher indemnity rate means you’ll recover more when filing a claim, though this often comes with increased premiums. If your business involves international trade, it’s essential to secure coverage for political risks like currency restrictions, conflicts, or expropriation. For domestic operations, the focus typically shifts to commercial risks such as insolvency or defaults.

Cost-Effectiveness

Striking the right balance between premium costs and potential recoveries is key to cost-effective coverage. Even a single mid-sized default can often offset the entire annual premium, illustrating how quickly the coverage can pay for itself. Features like discretionary limits can cut administrative costs by enabling auto-approval for smaller buyers, while top-up policies offer extra capacity for high-volume buyers. If your business depends heavily on a handful of major accounts, setting adequate coverage limits is especially important. A default from a key account could lead to serious financial disruption, so having the right safeguards in place is crucial.

Business Growth Support

The right coverage doesn’t just protect – it helps your business grow. Broader coverage limits allow you to confidently explore new sectors or markets while managing your exposure. Additionally, trade credit insurance can reduce the need for high allowances for doubtful accounts, freeing up working capital. That extra liquidity can then be reinvested into areas like equipment upgrades, new hires, or market expansion.

"The policy coverage also needs to match how your business operates" – Jason Benson, J.P. Morgan

Tailoring your coverage to align with your business operations ensures you’re not over-insured or unnecessarily exposed to risks. Accounts Receivable Insurance offers customized trade credit policies built to fit your specific risk profile and operational needs, helping you get the most out of your investment.

5. Better Financing and Cash Flow

Impact on ROI

Trade credit insurance transforms receivables – often a huge chunk of total assets, sometimes up to 40% – into collateral that lenders trust. Why? Because insured receivables come with a much lower risk of non-payment. This makes banks more comfortable, allowing businesses to secure improved financing terms.

"Lenders advance more against insured receivables at favorable terms." – Kirk Elken, Co-founder, Securitas Global Risk Solutions

By assigning your trade credit insurance policy to a financing bank, you enhance your credit profile. What does this mean for you? Lenders may offer higher advance rates and even lower interest margins. This gives you more working capital to reinvest in your operations or fuel growth. Plus, recovery teams can help speed up collections on overdue invoices, which shortens your cash conversion cycle. The result? Better loan terms and faster cash flow.

Business Growth Support

When financing terms improve, it’s like unlocking a new level of opportunity. The extra capital you gain can go toward expanding your business. Insured receivables also allow you to negotiate a more flexible borrowing base with your lender, giving you access to more liquidity. And since you can reduce allowances for doubtful accounts, those funds can be redirected toward things like upgrading equipment, hiring talent, or entering new markets.

"Banks recognise insured receivables as stronger collateral because protection reduces uncertainty on recovery." – Silvia Ungaro, Senior Advisor, Atradius

With Accounts Receivable Insurance, policies are designed to align with lender requirements, ensuring you get the maximum protection and financial benefits possible.

Trade Credit Insurance Explained

Conclusion

The return on investment (ROI) in trade credit insurance comes from two key areas: direct claim recoveries and indirect benefits like improved financing options and operational efficiency. Direct recoveries typically cover 75% to 95% of losses, while the indirect perks include smoother operations, better loan terms, and opportunities for growth.

"Credit insurance delivers its full impact across the entire policy year, not only when a claim is made, and its contribution reaches far beyond the reimbursement of losses." – Silvia Ungaro, Senior Advisor, Atradius

This comprehensive impact shows how trade credit insurance supports financial stability. Instead of viewing premium costs, claim payouts, and financing benefits as separate elements, these factors work together to strengthen your balance sheet. Insured receivables reduce write-offs, improve loan terms, and increase gross margins, transforming them into valuable collateral that stabilizes cash flow and unlocks additional working capital.

When considering ROI, the right coverage can make a noticeable financial difference. By partnering with Accounts Receivable Insurance, you gain access to tailored policies designed to fit your specific risk profile, whether you need whole-turnover coverage or protection for specific accounts. Expert brokers guide you through complex policy details, help you meet claim deadlines, and ensure your coverage aligns with lender requirements. This personalized approach maximizes both protection and financial benefits.

Beyond financial security, the right policy provides operational advantages. It shields your business from customer insolvencies while offering valuable buyer intelligence, industry insights, and recovery expertise – resources that might otherwise require expanding your internal team. As a result, vulnerable receivables become protected assets, cash flow remains steady, and allowances for doubtful accounts decrease, leaving your balance sheet stronger than ever.

FAQs

How do I calculate trade credit insurance ROI for my receivables?

To figure out the return on investment (ROI) for trade credit insurance, start by subtracting the total costs of the insurance – like premiums – from the benefits it provides. These benefits might include protected cash flow, lower risk of customer defaults, and potential cost savings. Once you have the net benefit, divide it by the total insurance costs.

The key takeaway? Trade credit insurance can offer advantages like better cash flow management, reduced financial risks, and potential savings, all of which help you assess whether the insurance is delivering a worthwhile return.

What can cause a claim to be denied or delayed?

Claims can face delays or denials for several reasons, including disputed invoices, missing claim reporting deadlines, failure to meet past-due reporting requirements, shipping goods to buyers with overdue payments, or issuing invoices outside of approved payment terms. To prevent these problems, it’s important to follow all policy guidelines and meet deadlines consistently.

How does trade credit insurance improve borrowing and cash flow?

Trade credit insurance helps businesses enhance their borrowing power and manage cash flow by safeguarding against unpaid invoices caused by customer insolvency or default. When receivables are insured, lenders view them as lower-risk assets, which can lead to improved financing terms. This protection also brings more stability to cash flow, minimizes the need to set aside large reserves for bad debts, and aids in more reliable financial planning. As a result, businesses can cover expenses, plan for growth, and maintain overall financial stability with greater confidence.