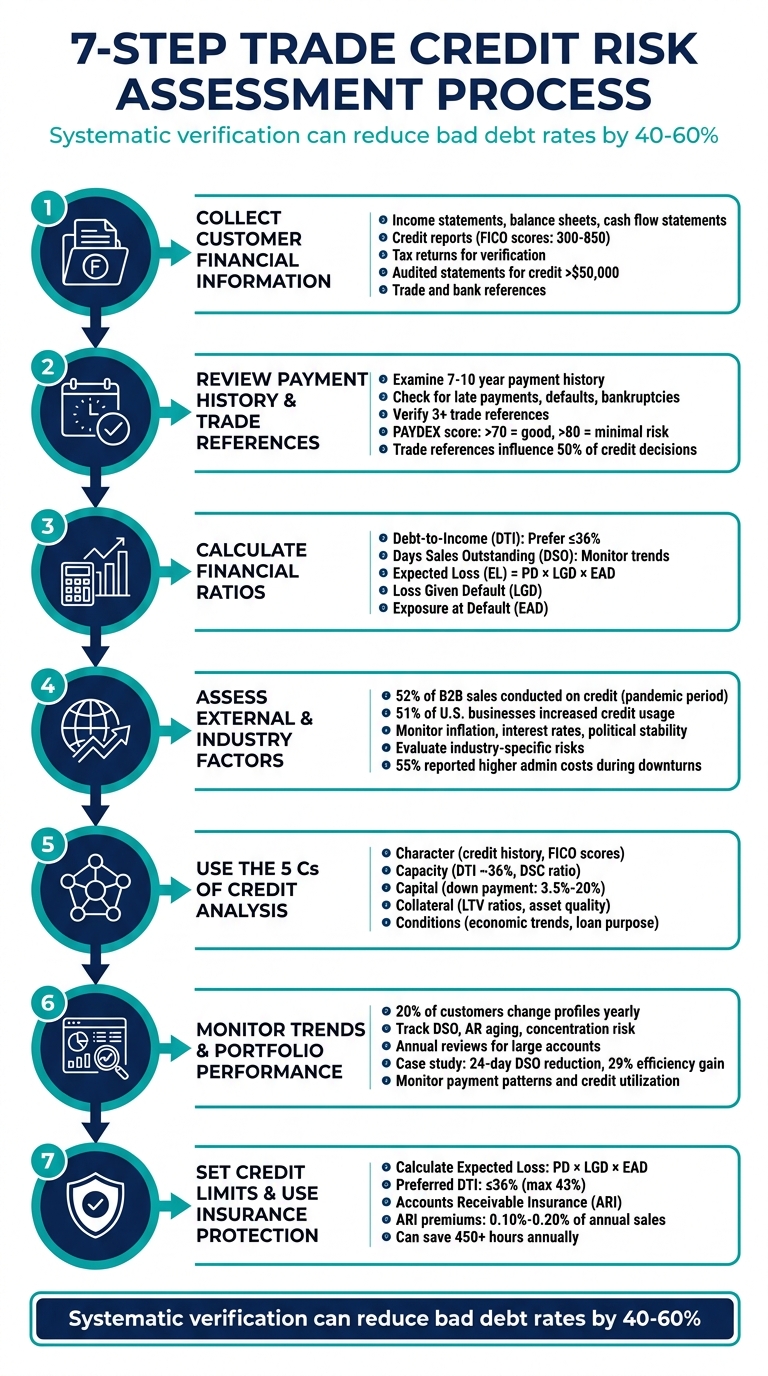

Trade credit risk is the risk of financial loss when a borrower or customer fails to meet payment obligations for goods, services, or loans provided on credit. To effectively manage this risk, focus on these key steps:

- Key Metrics: Use Probability of Default (PD), Exposure at Default (EAD), and Loss Given Default (LGD) to estimate risks and guide decisions.

- Collect Financial Data: Gather and verify financial statements, credit reports, and references to assess customer stability.

- Review Payment History: Analyze payment patterns and trade references to identify potential red flags.

- Analyze Financial Ratios: Use ratios like Debt-to-Income (DTI), Days Sales Outstanding (DSO), and Expected Loss (EL) to quantify risk.

- Evaluate External Factors: Consider economic conditions, industry-specific risks, and market trends that may impact customers.

- Apply the 5 Cs of Credit: Assess Character, Capacity, Capital, Collateral, and Conditions for a comprehensive credit evaluation.

- Monitor Trends: Continuously track customer behavior, portfolio performance, and adjust credit limits as necessary.

- Use Credit Insurance: Protect against defaults and non-payment with Accounts Receivable Insurance (ARI).

7-Step Trade Credit Risk Assessment Process for Financial Services

Credit Risk Managment – Credit Analysis and Risk Assessment

sbb-itb-2d170b0

Step 1: Collect Customer Financial Information

The backbone of any credit risk assessment is reliable financial data. Without it, making informed decisions becomes nearly impossible. The key lies in knowing what to request and ensuring the information you receive is accurate and dependable. The next step is to pinpoint and verify the financial documents that reveal a customer’s stability.

Required Financial Documents

Start by gathering essential financial statements: income statements, balance sheets, and cash flow statements. These documents provide insights into profitability, debt levels, and liquidity. For consumer credit evaluations, you’ll need credit reports from major agencies like Equifax, Experian, and TransUnion, along with FICO scores, which range from 300 to 850. For business customers, reports from Dun & Bradstreet or similar commercial credit agencies are essential.

Tax returns offer a secondary layer of verification to confirm reported income matches what was filed with the IRS. For credit limits exceeding $50,000, always request audited financial statements instead of relying on unaudited or self-reported documents. Additionally, trade and bank references provide valuable insights into actual payment behavior.

It’s important to scale documentation requirements based on the level of credit exposure. For smaller credit limits, such as $5,000, a credit report and a couple of trade references may be enough. However, as the credit amount increases, so should the depth of your documentation.

Verify Data Accuracy

Collecting financial documents is just the first step – verification is what ensures their reliability. This step is critical to avoid costly errors. Cross-reference customer-provided financial statements with external credit reports and lien databases to identify any discrepancies. For example, a company might present a clean balance sheet while concealing judgments or tax liens that appear in public records.

Modern tools, such as automated systems and APIs, allow direct data extraction from banks and employers, reducing manual errors and the risk of fraudulent submissions. Contact trade references directly to confirm payment patterns, average payment timelines, and whether special payment arrangements were ever required. Businesses that implement systematic verification as part of their credit management process often see bad debt rates drop by 40% to 60% compared to those that skip this step.

Once you’ve verified the accuracy of the data, you can move on to analyzing payment behaviors to complete the risk assessment.

Step 2: Review Payment History and Trade References

A customer’s payment history is one of the clearest indicators of their future reliability. Patterns like repeated late payments, defaults, or even bankruptcies can significantly raise their risk profile. This step involves turning raw data into actionable insights about payment behavior.

Examine Payment Patterns

Once financial data is verified, take a closer look at payment patterns to identify trends in credit behavior. Credit reports from agencies like Equifax, Experian, and TransUnion often highlight critical markers such as late payments, defaults, accounts in collections, and bankruptcies – some of which can remain visible for 7–10 years. Even minor issues, like payments made 15 days late on Net 30 terms, should be flagged for deeper investigation.

It’s not just about spotting isolated incidents, though. Keep an eye out for worsening trends, such as progressively longer delays in payments, which can indicate deteriorating financial health. To get a full picture, combine your internal accounts receivable data with external credit reports. Automated risk systems can also be valuable, alerting you to shifts in payment performance so you can adjust credit lines before issues escalate.

Check Trade References

Trade references offer a practical view of how customers handle their financial obligations. Aim to get references from at least three vendors who have similar billing cycles and risk levels. Key details to evaluate include the reporting date, payment method, recent credit usage, overdue amounts, sale terms, current balances, and the date of the last transaction.

Always verify trade references directly. A phone call to the listed contact can reveal details that written forms might miss. Since supplier references influence over 50% of trade credit decisions, it’s crucial to look for consistent feedback across multiple vendors. A single glowing reference isn’t enough, and vague or incomplete references should raise red flags. For a broader view, business credit reports from companies like Dun & Bradstreet or Experian can be helpful. These reports, which typically cost $50–$150, aggregate trade data into scores like the PAYDEX. A PAYDEX score above 70 suggests good payment behavior, while scores over 80 indicate minimal credit risk.

Together, these insights help build a well-rounded risk profile, setting the stage for a deeper analysis of financial ratios.

Step 3: Calculate Financial Ratios

Once you’ve gathered payment history and trade references, the next step is to calculate financial ratios. These ratios turn raw financial data into measurable indicators of credit risk. They help you spot potential problems early and provide a data-driven perspective on a customer’s creditworthiness, complementing the payment data you’ve already reviewed.

Key Financial Ratios to Know

• Debt-to-Income (DTI) Ratio

This ratio shows how well a borrower can manage monthly debt payments compared to their gross monthly income. Generally, lenders prefer a DTI of 36% or less, though some may approve up to 43%. A DTI under 38% often signals a borrower can handle payments comfortably. To calculate it, divide total monthly debt payments by gross monthly income.

• Days Sales Outstanding (DSO)

DSO measures the average time it takes to collect payment after a sale. Use this formula:

(Accounts Receivable / Total Credit Sales) × Number of Days.

An increasing DSO can highlight cash flow issues or financial trouble among customers. Comparing your DSO to industry averages can reveal if your payment terms or collection processes need adjusting.

• Expected Loss (EL)

Expected Loss estimates the potential financial loss from a credit exposure. It’s calculated as PD × LGD × EAD, where:

– Loss Given Default (LGD): The percentage of exposure lost if a default occurs, calculated as 1 – (Potential Sale Proceeds / Outstanding Debt).

– Exposure at Default (EAD): The total outstanding principal plus accrued interest at the time of default.

| Ratio | Calculation Formula | Purpose in Risk Assessment |

|---|---|---|

| Debt-to-Income (DTI) | Total Monthly Debt / Gross Monthly Income | Evaluates the borrower’s ability to handle additional debt |

| Days Sales Outstanding (DSO) | (Accounts Receivable / Total Credit Sales) × Number of Days | Assesses collection efficiency and AR portfolio quality |

| Expected Loss (EL) | PD × LGD × EAD | Estimates total potential loss from credit exposure |

| Loss Given Default (LGD %) | 1 – (Potential Sale Proceeds / Outstanding Debt) | Measures potential loss percentage in a default scenario |

| Exposure at Default (EAD) | Total Outstanding Principal + Accrued Interest | Calculates the total value at risk during default |

Once these ratios are calculated, the next step is to interpret them for actionable insights.

Making Sense of the Ratios

These ratios are essential for understanding credit risk. For example, a high DTI suggests a borrower is overleveraged and more likely to default, while a low DTI indicates they have room to take on more debt. Similarly, a high DSO could point to cash flow issues or inefficiencies in collections, whereas a low DSO reflects strong payment practices.

Tracking DSO trends over time can help identify patterns among customers based on geography, industry, or company size. Pair this analysis with aging reports to flag accounts with overdue payments. Keep in mind that trade credit often operates on slim profit margins – sometimes as low as 1–2% per transaction. A few delinquent accounts can seriously hurt your bottom line. By combining these numerical insights with qualitative evaluations, you can build a well-rounded risk profile to support better credit decisions.

With these metrics in hand, you’re ready to move on to evaluating external and industry-specific factors.

Step 4: Assess External and Industry Factors

While financial ratios provide a snapshot of a customer’s current financial health, they don’t account for external influences that can quickly escalate credit risk. For instance, during the economic turmoil caused by the pandemic, 52% of the total value of B2B sales in surveyed U.S. industries was conducted on credit. Additionally, 51% of U.S. businesses reported an uptick in trade credit usage in the months following the disruption. This surge in credit reliance came at a cost – many businesses faced increased late payments and higher debt write-offs as customers struggled to meet their obligations.

Market and Economic Conditions

Broader economic factors like inflation, fluctuating interest rates, and political instability play a big role in shaping your customers’ ability to pay. When uncertainty looms, it’s crucial to update your Probability of Default (PD) models to reflect the shifting landscape. As Mahesh Narayanasami, Partner at KPMG in the U.S., explains:

"In times of increased economic uncertainty, it may be challenging for companies to incorporate forward-looking information… into their assessment of whether credit risk on a financial instrument has increased significantly".

Keep an eye out for qualitative red flags, such as requests for payment holidays, relaxed covenants, or increased credit limits. These can serve as early warning signs of financial stress. During economic downturns, 55% of U.S. businesses reported higher administrative costs associated with managing accounts receivable, especially those that self-insure. These signals provide context for identifying vulnerabilities that may be unique to specific industries.

Industry-Specific Risks

Some industries are more prone to sudden disruptions than others. Take the energy sector, for example – when oil prices drop sharply, it can lead to rapid declines for companies within the industry, often pushing offshore drilling contractors toward bankruptcy. Concentration risk is another critical factor to consider. If your portfolio is heavily tied to a single sector or geographic area, a localized downturn could result in widespread defaults.

It’s essential to assess how your customers’ industries are performing and evaluate their supply chain dependencies. Even a financially stable customer can face challenges if a key supplier collapses or a major buyer reduces orders. Additionally, regulatory changes can reshape entire industries overnight, influencing profitability and stability. Staying informed about pending legislation and its potential impact on your customers’ sectors is a key part of managing credit risk effectively.

Step 5: Use the 5 Cs of Credit Analysis

The 5 Cs Framework

After analyzing financial ratios and external risks, it’s time to bring everything together. The 5 Cs of Credit – Character, Capacity, Capital, Collateral, and Conditions – offer a structured way to assess creditworthiness. As Investopedia puts it:

"The five Cs of credit are a system used by lenders to gauge the creditworthiness of potential borrowers… attempting to estimate the chance of default and, consequently, the risk of a financial loss for the lender".

Each "C" plays a distinct role in the overall evaluation. For instance, a borrower might have strong cash flow (Capacity) but face challenges from a struggling industry (Conditions). Or, they may have a poor credit history (Character) but offer significant collateral to offset risk. The Corporate Finance Institute notes, "Strength in one C can help to offset weakness in another". This interconnected nature means you need to weigh all five elements carefully before making a decision.

Apply the 5 Cs in Practice

Character focuses on the borrower’s trustworthiness. For individuals, this involves reviewing credit reports from agencies like Equifax, Experian, or TransUnion and checking FICO scores. For businesses, assess management’s track record, industry expertise, and how they’ve handled credit obligations in the past. You can also strengthen this evaluation by encouraging automatic bill payments.

Capacity assesses whether the borrower can generate enough cash flow to meet their debt obligations. For individuals, this often means maintaining a Debt-to-Income (DTI) ratio near 36%. For businesses, calculate the Debt Service Coverage (DSC) ratio using their income statements to confirm they can manage all payment obligations. When evaluating businesses, focus on their ability to pay off loans entirely rather than just reducing balances, as lenders prioritize monthly payment reliability.

Capital refers to the borrower’s financial strength and their personal stake in the loan or investment. For instance, Federal Housing Administration (FHA) loans may require as little as a 3.5% down payment, but borrowers who contribute at least 20% often avoid private mortgage insurance. In trade credit, look for personal or corporate guarantees and unencumbered assets that can act as secondary repayment sources.

Collateral includes assets pledged to secure the loan, reducing the lender’s potential losses. These can range from real estate and equipment to accounts receivable or stock portfolios. The quality and liquidity of these assets determine acceptable Loan-to-Value (LTV) ratios. Identifying liquid assets, for example, can help borrowers secure better terms. This analysis directly affects credit limits and may highlight the need for Accounts Receivable Insurance for extra protection.

Conditions cover external factors like the loan’s purpose, economic trends, and industry-specific risks. Assess how current interest rates, GDP growth, and regulatory changes could impact repayment ability. Borrowers should provide clear "use of proceeds" statements and solid financial projections that show how the loan will support future cash flow.

| The 5 Cs | Financial Services Application | Key Metrics/Documents |

|---|---|---|

| Character | Borrower’s reputation and reliability | FICO scores, credit reports, background checks, industry experience |

| Capacity | Ability to generate sufficient cash flow | Debt-to-Income (DTI) ratio, Debt Service Coverage (DSC) ratio, income statements |

| Capital | Borrower’s financial strength and investment | Down payment size, debt-to-equity ratio, personal/corporate guarantees |

| Collateral | Assets securing the loan | Loan-to-Value (LTV) ratio, real estate, inventory, stock portfolios |

| Conditions | External factors and loan purpose | Interest rates, industry trends, GDP growth, regulatory environment |

Step 6: Monitor Trends and Portfolio Performance

Evaluating credit risk isn’t just a one-and-done task. Once credit limits are set and customers are approved, it’s essential to keep an eye on their behavior and the overall performance of your portfolio. Here’s why: 20% of trade credit customers change their profiles every year. That means a customer who seemed low-risk yesterday could become a concern tomorrow. This underscores the need for ongoing monitoring.

Start by focusing on individual customer behavior. Pay close attention to key indicators like payment patterns, credit utilization, and invoice disputes. For example, if a customer stretches payment terms from 30 days to 60–90 days, it’s a red flag that needs immediate attention. Similarly, maxing out a credit limit or an increase in invoice disputes can often signal financial trouble long before an actual default occurs. Amanda Slusarczyk, National Credit Manager at Flocor, highlights the value of automated tools for staying ahead:

"Moody’s portfolio monitoring and daily email alerts are fantastic. It gives me a poke to investigate when accounts could be at risk without adding to my daily workload".

On a portfolio-wide level, keep track of metrics like Days Sales Outstanding (DSO), accounts receivable aging, and concentration risk. Regular reviews are key – schedule annual evaluations for your largest accounts and biennial ones for smaller customers. A great example of how monitoring and automation can boost efficiency comes from Jumio, a global digital identity verification provider. In June 2024, the company adopted Quadient AR to centralize its receivables data. By automating payment reminders and offering self-service billing options, Jumio cut its DSO by 24 days, improving collection efficiency by 29% without adding staff.

For high-risk or high-limit accounts, request updated financial statements annually and compare trends over at least two years. This helps identify early warning signs and allows for proactive adjustments.

Another critical factor is analyzing concentration risk. If a large portion of your revenue depends on a few customers or a single industry, you face heightened vulnerability to correlated defaults. Reviewing five years of bad debt history can reveal patterns tied to specific regions or industries. Recognizing these trends early enables you to refine credit policies and minimize risks before they escalate.

Step 7: Set Credit Limits and Use Insurance Protection

After establishing a system for monitoring performance, the next step is to fine-tune credit limits to protect your cash flow while enabling growth.

Determine Credit Limits

Setting appropriate credit limits is a balancing act between encouraging business growth and minimizing risks. To do this effectively, rely on your earlier 5 Cs analysis, with a particular focus on Capacity. This is often measured by the customer’s debt-to-income (DTI) ratio. Generally, lenders favor a DTI of 36% or less, though some may accept up to 43%.

To refine your decision-making, calculate the Expected Loss using this formula: Probability of Default (PD) × Loss Given Default (LGD) × Exposure at Default (EAD). For instance, if a customer has a 10% probability of default, you estimate a 60% loss on recoverable amounts, and the exposure is $100,000, your expected loss would come to $6,000. This figure provides a solid foundation for setting credit limits.

Credit limits should remain flexible. Automated systems can help adjust limits in real-time as customer conditions evolve. If a customer’s financial health begins to decline, lowering their credit line early can prevent more severe payment issues down the road.

Protect with Accounts Receivable Insurance

Even with carefully managed credit limits, defaults can still happen. That’s where Accounts Receivable Insurance (ARI) steps in, acting as a safety net against risks like non-payment, bankruptcies, or even political instability. This form of insurance complements your existing risk management strategies by mitigating losses identified during your earlier analyses. Premiums for ARI typically range from 0.10% to 0.20% of your total annual sales.

Providers like Accounts Receivable Insurance offer policies tailored to your business needs, covering both domestic and international markets. Beyond just financial protection, ARI services include risk assessments and early warning systems, which alert you to potential customer issues before they escalate. For example, a timely credit alert could help you avoid charge-offs as high as $30,000.

Additionally, ARI seamlessly integrates into your existing risk monitoring tools, providing a comprehensive view of your global portfolio. By automating administrative tasks, it can save your business over 450 hours annually. For companies in high-risk industries or those dealing with large credit exposures, this insurance transforms unpredictable risks into manageable costs.

Conclusion

Managing trade credit risk in financial services requires a structured approach, constant attention, and effective safeguards. As Atradius aptly states:

"The secret to prompt payment lays in a systematic and consistent approach to credit management".

By following the outlined seven steps, businesses can establish a framework that identifies potential risks before they escalate into significant problems.

But it doesn’t stop there. Effective risk assessment also involves examining internal processes. For example, segmenting your portfolio can uncover areas of over-concentration or inefficiencies in collections. Tracking key metrics like Days Sales Outstanding (DSO) can highlight weaknesses in your payment collection strategies. Regular reviews – ideally led by a dedicated team on a weekly basis – allow for quick adjustments when economic conditions change or customer payment behaviors shift.

Even the best processes have limitations, which is why having protective measures in place is critical. Tools like Accounts Receivable Insurance can turn unpredictable losses into manageable expenses, protecting your cash flow when faced with customer insolvency or non-payment. This complements the proactive monitoring and disciplined credit limit strategies discussed earlier, ensuring that your business can seize growth opportunities without taking on unmanageable risks.

Ultimately, early detection of credit risks is key to minimizing losses. A disciplined approach to credit assessment not only shields your financial health but also positions your business to navigate uncertainty with confidence.

FAQs

How do I estimate PD, LGD, and EAD for a new customer?

This measures how likely it is that a customer will default on their financial obligations. To evaluate this, factors like credit scores, overall financial health, and industry-specific data are analyzed.

LGD (Loss Given Default)

This metric estimates the potential financial loss in the event of a default. It considers elements such as the value of collateral, the seniority of the debt, and historical recovery rates.

EAD (Exposure at Default)

This calculates the amount of exposure a lender might face if a default occurs. It is determined by examining credit limits, current account balances, and credit usage patterns.

For a more precise assessment of expected losses, risk models like CECL (Current Expected Credit Loss) are often used, particularly for trade receivables. These models provide a structured approach to quantifying potential financial risks.

What are the earliest warning signs a customer is about to pay late or default?

Spotting the early signs of late payments or potential default can make a big difference for businesses. Some red flags to watch for include customers expressing dissatisfaction with payment terms, frequently requesting extensions, or blaming delays – these often point to cash flow troubles.

Keep an eye on payment patterns too. Delays in payments or sudden requests to adjust credit terms can signal underlying issues. By identifying these warning signs early, businesses can take proactive steps to address the situation and reduce financial risks.

When should I add Accounts Receivable Insurance to my credit risk strategy?

If you’re looking to minimize the risk of non-payment or default when offering trade credit, Accounts Receivable Insurance (ARI) could be a smart addition to your credit risk strategy. This type of insurance is especially helpful in protecting your business from losses caused by customer insolvency, political instability, or other unexpected events. With coverage that can reimburse up to 90% of losses, ARI becomes an important safety net – particularly during times of economic uncertainty or when dealing with substantial receivables.