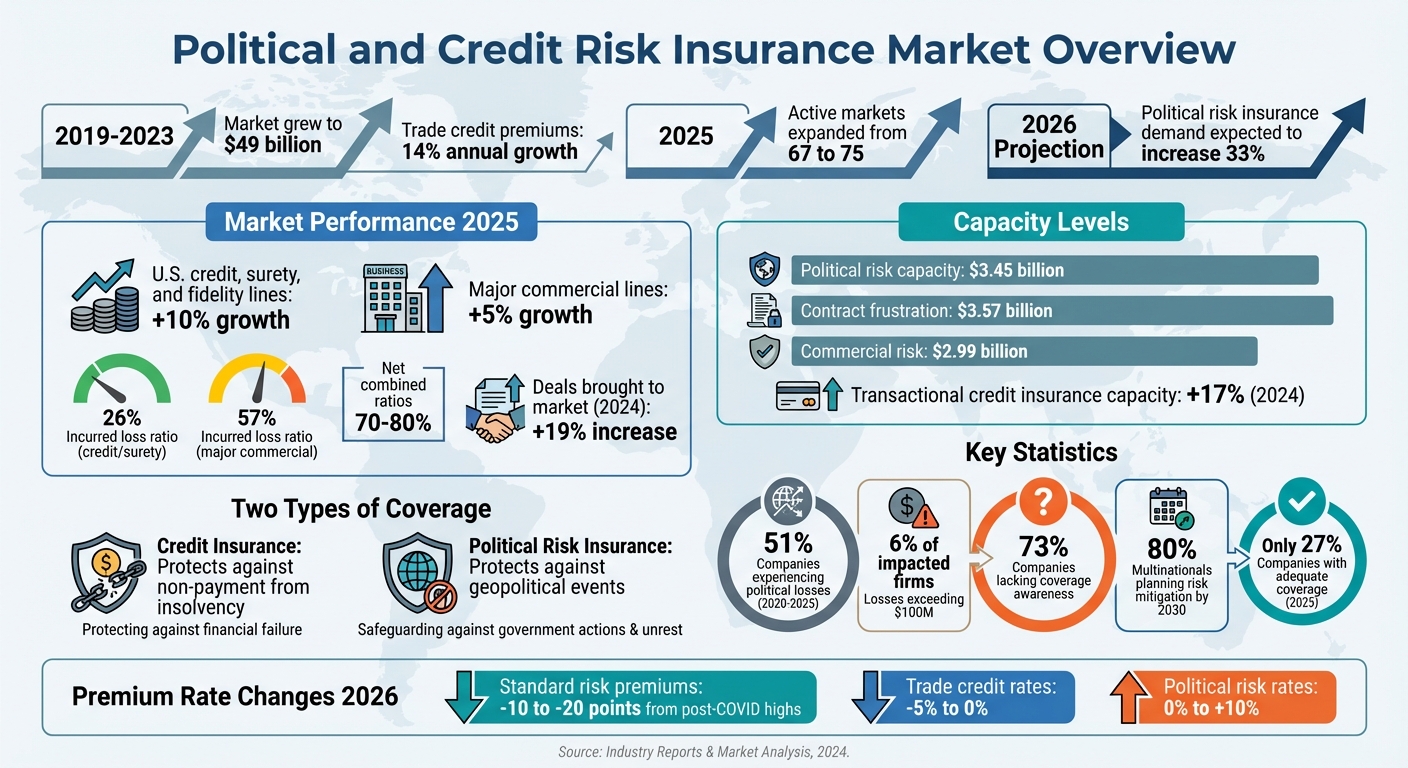

Political and Credit Risk Insurance (CPRI) is increasingly important for businesses navigating international trade risks. It protects against two main threats: non-payment by customers and political disruptions like expropriation or currency restrictions. Between 2019 and 2023, the CPRI market grew rapidly, reaching a value of $49 billion, with trade credit premiums expanding by 14% annually.

Key takeaways:

- Credit insurance covers losses from unpaid invoices due to insolvency or other financial issues.

- Political risk insurance protects against geopolitical events, such as government interference or political violence.

- Combined policies are gaining traction, addressing overlapping risks like payment defaults caused by political events.

In 2025, demand surged due to global instability, rising inflation, and geopolitical tensions. Renewable energy projects overtook oil and gas as a focus area, while emerging markets like Asia and Africa drove growth. Insurers expanded their capacity, with active markets increasing from 67 to 75. Underwriting standards tightened, focusing on tailored solutions for complex risks.

Looking ahead to 2026, factors like tariff uncertainties, rising bankruptcies, and "gray zone" risks are expected to push more businesses toward adopting CPRI. U.S. companies, especially in high-growth regions like India and Mexico, can benefit from stable trade credit insurance rates and tailored policies to mitigate risks and support global growth.

Global Political and Credit Risk Insurance Market Growth 2019-2026

Market Growth and Performance in 2025

What’s Driving Market Expansion

The growth of the Credit and Political Risk Insurance (CPRI) market in 2025 was fueled by a mix of global disruptions and shifting priorities. Geopolitical instability played a major role, with escalating tensions in regions like the Middle East and Africa, coupled with changes in U.S. political policies and evolving trade relationships. These factors pushed businesses to reassess their international strategies, making political risk a priority rather than an afterthought.

On top of that, macroeconomic challenges added to the demand for risk transfer solutions. Persistent inflation, fluctuating interest rates, and concerns over potential sovereign defaults created a climate of financial uncertainty. Global supply chains, already under strain, faced additional pressure, highlighting the importance of comprehensive risk coverage.

Interestingly, 2025 saw a shift in industry focus. For the first time, renewable energy projects attracted more attention than traditional oil and gas ventures. Emerging markets in Asia and Africa experienced significant growth, with infrastructure development driving demand for credit and political risk protection.

These factors combined to shape the market’s strong performance throughout the year.

Market Performance Data and Statistics

The numbers tell a compelling story. During the first half of 2025, U.S. credit, surety, and fidelity lines grew by 10%, outpacing the 5% rise in major commercial lines. This growth wasn’t just about scale – it reflected precise underwriting and a focus on profitability. The incurred loss ratio for credit and surety markets dropped to 26%, a sharp contrast to the 57% seen in major U.S. commercial lines during the same period.

"2025 was defined by a rare combination of strong growth, disciplined underwriting and sustained outperformance across the CPRI market." – Phil Bonner, Managing Director of Global Specialty Treaty, Howden Re

The market’s dynamism was evident in its activity. In 2024, the number of deals brought to market for coverage surged by 19%, leading to over 15,000 communications with insurers. To meet this growing demand, the number of active CPRI markets expanded to 75 in 2025, up from 67 the previous year. Net combined ratios in the sector remained consistently favorable, typically ranging between 70% and 80%.

These statistics underscore the sector’s ability to balance growth with profitability, maintaining resilience in the face of global challenges.

sbb-itb-2d170b0

Supply, Demand, and Insurer Capacity Trends

Growing Preference for Customized Coverage

The insurance landscape is shifting as businesses increasingly demand policies tailored to their unique risks. Generic, one-size-fits-all coverage no longer cuts it, especially as operational challenges grow more complex. Since 2025, this trend has gained significant traction, particularly in sectors like infrastructure, trade finance, and renewable energy. These industries face risks that standard policies often fail to address, making customization the norm rather than the exception.

Accounts Receivable Insurance is a prime example of this shift, offering policies specifically designed to shield businesses from credit and political risks. This push for bespoke coverage is reshaping how insurers allocate capacity, ensuring they align their offerings with the specific needs of their clients.

How Insurers Are Expanding Their Capacity

The demand for tailored policies has prompted insurers to rethink and expand their capacity. The number of active CPRI markets rose from 67 in 2024 to 75 in 2025. But this growth isn’t just about adding more players – it’s about making capacity more accessible and practical for businesses.

Insurers have adjusted their strategies by reducing theoretical coverage lines in favor of increasing deployable capacity. This means businesses can now access more usable coverage for standard transactions. Additionally, Managing General Agents (MGAs) have entered the scene, bringing fresh capacity and intensifying competition.

Current capacity levels highlight this growth: political risk capacity stands at $3.45 billion, contract frustration at $3.57 billion, and commercial risk at $2.99 billion. Notably, transactional credit insurance capacity surged by 17% in 2024, outpacing political risk insurance capacity for the first time.

To keep up with evolving client demands, insurers are honing their focus on specific market segments rather than attempting to cover every possible risk. This targeted approach ensures that capacity aligns more closely with the nuanced needs of modern businesses.

Pricing and Underwriting Practices

How Risk Conditions Affect Premium Rates

The political risk insurance market is still challenging overall, but pricing trends are starting to show some shifts depending on what and where you’re insuring. For more standardized risks, premium rates have dropped by 10 to 20 points from their post-COVID highs, largely due to new players entering the market and increasing capacity. However, looking ahead to 2026, political risk rates are expected to change by 0% to +10% year-over-year, depending on the specific risk profile.

Geography plays a major role in determining premium rates. In regions with heightened tensions – such as China, Taiwan, parts of West Africa (Mali, Burkina Faso, Niger), Sudan, and Israel – capacity remains extremely limited, resulting in stricter terms and higher premiums. On the other hand, insurers are actively pursuing opportunities in areas like Mexico, Malaysia, Nigeria, India, and Indonesia, where competition keeps pricing more attractive.

"The political risk market remains hard, but some insurers are gradually adopting more flexible stances for multicountry programs (as long as they don’t include China or Taiwan)." – WTW Insurance Marketplace Realities 2026

At the January 1, 2026 reinsurance renewals, ceding commissions on quota-share business saw moderate increases, while excess of loss programs remained relatively steady. These pricing dynamics are directly influencing underwriting practices, which are becoming more rigorous.

Changes in Underwriting Standards

As pricing adjusts, underwriting standards have tightened to address emerging risks. Insurers are now more selective, focusing on what they call "gray zone" risks – uncertain threats like abrupt regulatory changes, state-backed corporate takeovers, and political instability caused by polarization. A notable example is Guinea’s 2025 nationalization of mining concessions, where the government reassigned assets to newly created state entities. This type of regulatory unpredictability is now a key factor in underwriting decisions.

The industry is also grappling with a shortage of skilled underwriters, which is pushing up expense ratios and further influencing selectivity. Insurers are prioritizing sectors where they have deep expertise, with renewables now surpassing oil and gas in total exposure for the first time. This talent gap is helping maintain premium levels, even as market capacity grows.

To meet client needs, insurers are refining their underwriting criteria to ensure effective risk-sharing. A major focus is on achieving alignment of interest between insurers and policyholders, which has been credited with keeping loss ratios low despite global uncertainty. Insurers are also moving away from offering large, rarely used "theoretical" capacities. Instead, they’re providing smaller, more practical line sizes tailored to actual client needs. For businesses, this shift means underwriters are looking for genuine partnerships and a shared commitment to managing risks, rather than purely transactional relationships.

2026 Outlook: What Will Drive Adoption

Expected Adoption Drivers in 2026

The global trade landscape is shifting rapidly, and several factors are pushing businesses to prioritize risk insurance in 2026. One major catalyst is the uncertainty surrounding tariffs. Following the April 2025 introduction of a minimum 10% global tariff on U.S. imports – which climbed to an effective rate of 19.5% by August – many companies faced sudden payment defaults, a phenomenon experts now call "tariff shocks". Trade credit insurance is becoming an essential tool for managing the growing risks of counterparty non-payment.

Adding to the urgency, corporate bankruptcies in the U.S. surged by 15% in late 2025, further driving demand for insurance solutions. Political risk insurance, in particular, is expected to see a 33% increase in demand in 2026, driven by emerging threats like abrupt regulatory changes and discriminatory practices, often referred to as "gray zone" risks.

"2026 has started under a large cloud of uncertainty, often in the presence of overwhelming risks." – Coface

Another notable trend is the expansion of the buyer base. While political risk insurance was once the domain of large multinational corporations, it is now gaining traction among Middle Market enterprises venturing into international markets. This shift is supported by new capital inflows. For example, in February 2026, the International Finance Corporation finalized a $6 billion credit insurance policy with 19 global insurers to facilitate up to $10 billion in new loans for small and medium-sized businesses in emerging markets.

These evolving dynamics highlight the growing importance of tailored insurance solutions for U.S. businesses navigating a riskier global environment.

Opportunities for U.S. Companies

For U.S. companies, these adoption drivers create both challenges and opportunities. Heightened risks abroad – especially regulatory retaliation stemming from U.S. tariff policies – pose significant threats. Foreign governments are increasingly implementing measures like "creeping" expropriation, local content requirements, and discriminatory regulations. Political risk insurance can help address these vulnerabilities.

Meanwhile, high-growth markets such as Mexico, Malaysia, Nigeria, India, and Indonesia offer favorable opportunities for U.S. businesses. Insurers in these regions are well-positioned to provide competitive terms. For example, India’s economy is projected to grow by 6.1% in 2026, and global trade volumes rose by 3.9% in 2025 despite tariff pressures. Additionally, trade credit insurance rates are expected to remain stable, ranging from –5% to flat in 2026, making this an ideal time for companies managing international accounts receivable to secure coverage.

These policies also deliver financial benefits. Under Basel IV regulations, they provide capital relief for U.S. banks and investment funds, allowing for greater flexibility in emerging markets. Despite the clear advantages, there remains a significant gap in coverage: while 80% of multinationals plan to adopt geopolitical risk mitigation strategies over the next five years, only 27% of companies impacted by political risk losses in 2025 had adequate insurance. This gap underscores an opportunity for U.S. businesses to strengthen their competitive position by proactively addressing these risks with comprehensive insurance strategies.

Regional Trends and Real-World Examples

Regional Market Differences

The growing demand for tailored insurance coverage is shaping regional trends, with integrated policies advancing more swiftly in certain areas. A notable shift has occurred as insurers increasingly prioritize developed markets like the U.S., UK, and France over emerging markets. This change stems from concerns about fiscal challenges and potential losses in regions with higher volatility.

Adoption rates for political risk tools differ significantly across regions. Surveys show that in North America and Europe, the use of these tools is expected to rise sharply by 2030, compared to 68% adoption in the earlier part of the decade. This growth reflects a shift in perception, as multinational corporations now recognize that political instability is no longer exclusive to emerging markets. Between 2020 and 2025, 51% of senior risk and treasury executives in these regions reported experiencing political losses tied to international investments.

In Asia, the adoption of integrated policies is accelerating, with insurers expanding their capacity and targeting specialized market segments. Trade credit premiums in the region have seen impressive growth, increasing at a compound annual rate of 14% from 2019 to 2023 – outpacing U.S. surety (11%) and international surety (9%).

Examples of Successful Policy Use

These regional trends come to life through real-world examples where integrated policies have provided clear financial advantages. For instance, in September 2024, a Polish manufacturer obtained political risk insurance to safeguard a $45 million production facility in Ukraine. This groundbreaking policy offered protection against political and war-related risks, marking a significant milestone as the first insurance of its kind for a Polish production complex in Ukraine since the onset of the full-scale war.

The financial benefits of such coverage are evident in other cases as well. In May 2025, Equinor and Polenergia secured over €6 billion in financing for the Bałtyk 2 and Bałtyk 3 offshore wind farms in Poland. KUKE provided repayment guarantees for part of this financing, which involved around 30 international financial institutions.

Another noteworthy example took place in August 2024, when Turkish renewable energy firm Kalyon Enerji obtained a €249 million loan arranged by Standard Chartered Bank. The loan, backed by guarantees from KUKE (Poland) and UKEF (UK), facilitated the construction of Turkey’s second-largest solar project while also supporting the renewable energy supply chain in the UK.

A perfect storm for credit and political risk re/insurance, with Lockton Re‘s Eran Charit

Conclusion: What Businesses Should Know

By 2025, political and credit risk insurance has evolved from being a niche offering to becoming a must-have for U.S. companies operating on a global scale. Recent figures reveal the extent of political exposure, with 6% of impacted firms reporting losses exceeding $100 million.

For insured companies, the benefits are clear: reduced losses and lower country risk premiums. These policies can significantly decrease the country risk premium in emerging markets – from around 15% to 11% – resulting in average annual savings of about $2 million per investment. Considering premiums typically range from 0.5% to 1.5% of coverage limits, the financial case for protection becomes compelling.

"Political risk insurance is no longer just a safety net. It’s a strategic enabler."

- Laura Burns, Head of Political Risk, North America, Willis Credit Risk Solutions

One of the biggest hurdles for broader adoption remains awareness. A striking 73% of companies pinpoint a lack of understanding as the primary reason for not utilizing coverage. To address this, U.S. businesses can start by organizing internal risk education sessions and working with experienced brokers to customize policies for specific threats, such as currency disputes and ownership conflicts – issues that have impacted 40% of companies facing political losses. With 80% of multinational corporations planning to implement geopolitical risk mitigation strategies by 2030, early adopters will likely enjoy a competitive edge in uncertain markets.

The current market dynamics are favorable for buyers. Increased insurer capacity and rising demand have created opportunities for more flexible terms, especially for high-quality risks. Companies should assess both direct and indirect risks to ensure their coverage provides comprehensive protection and supports their global growth ambitions.

For U.S. businesses seeking tailored solutions, Accounts Receivable Insurance offers expertise in safeguarding both domestic and international investments, helping companies navigate an increasingly unpredictable global landscape.

FAQs

Do I need credit, political risk, or a combined policy?

Global trends indicate an increasing need for credit and political risk insurance, largely influenced by ongoing geopolitical and economic uncertainties. Deciding whether to opt for credit insurance, political risk insurance, or a combination of both depends entirely on the unique challenges your business faces. For example, if non-payment is a primary concern, credit insurance might be the right fit. On the other hand, if political instability poses a threat to your operations, political risk insurance could be more suitable. A combined policy may offer broader protection for businesses dealing with both types of risks. It’s always a smart move to consult with a specialized insurer who can evaluate your specific situation and recommend the most appropriate coverage.

What is a ‘gray zone’ political risk, and can it be insured?

A "gray zone" political risk describes uncertain geopolitical situations that don’t neatly fit into categories of war or peace, creating challenges in defining them. Interestingly, these risks are now more often being viewed as insurable. Political risk insurance providers are adjusting their approach to account for the growing complexities of the global landscape.

How do tariffs and bankruptcies affect my non-payment risk in 2026?

Tariffs can lead to higher costs and contribute to economic uncertainty, while an increase in bankruptcies adds to financial instability. Combined, these issues are likely to heighten the risk of non-payment in 2026. In this environment, trade credit insurance becomes an essential resource, offering businesses protection against losses from unpaid invoices and economic upheavals.