Credit insurance helps businesses offer longer payment terms (e.g., net 30, 60, or 90 days) while reducing financial risks. This coverage protects up to 85–95% of unpaid invoices if customers default due to insolvency, bankruptcy, or economic challenges. It also improves borrowing power by making receivables less risky for lenders. However, payouts often take 30–60 days, and deductibles can apply.

For businesses needing faster cash flow, Accounts Receivable Insurance (ARI) offers quicker liquidity, with cash advances of up to 90% of an invoice’s value within 24 hours. ARI is tailored to specific needs, such as managing risks tied to key customers or international trade. While more expensive than standard credit insurance, ARI provides faster access to funds and tools like automated credit monitoring.

Key Points:

- Standard Credit Insurance: Lower cost, broad protection, delayed payouts, deductibles apply.

- Accounts Receivable Insurance (ARI): Faster cash flow, tailored coverage, higher cost, no deductibles.

Quick Comparison:

| Feature | Standard Credit Insurance | Accounts Receivable Insurance (ARI) |

|---|---|---|

| Risk Coverage | 85–95% of losses, includes political risks | 80–90%, for approved customers only |

| Payout Speed | 30–60 days | Within 24 hours |

| Cost | 0.1–0.6% of sales | 0.1–0.4% of sales |

| Best For | Broad customer base | Key customers, faster cash needs |

Choose based on your business’s priorities: broad protection or immediate cash flow.

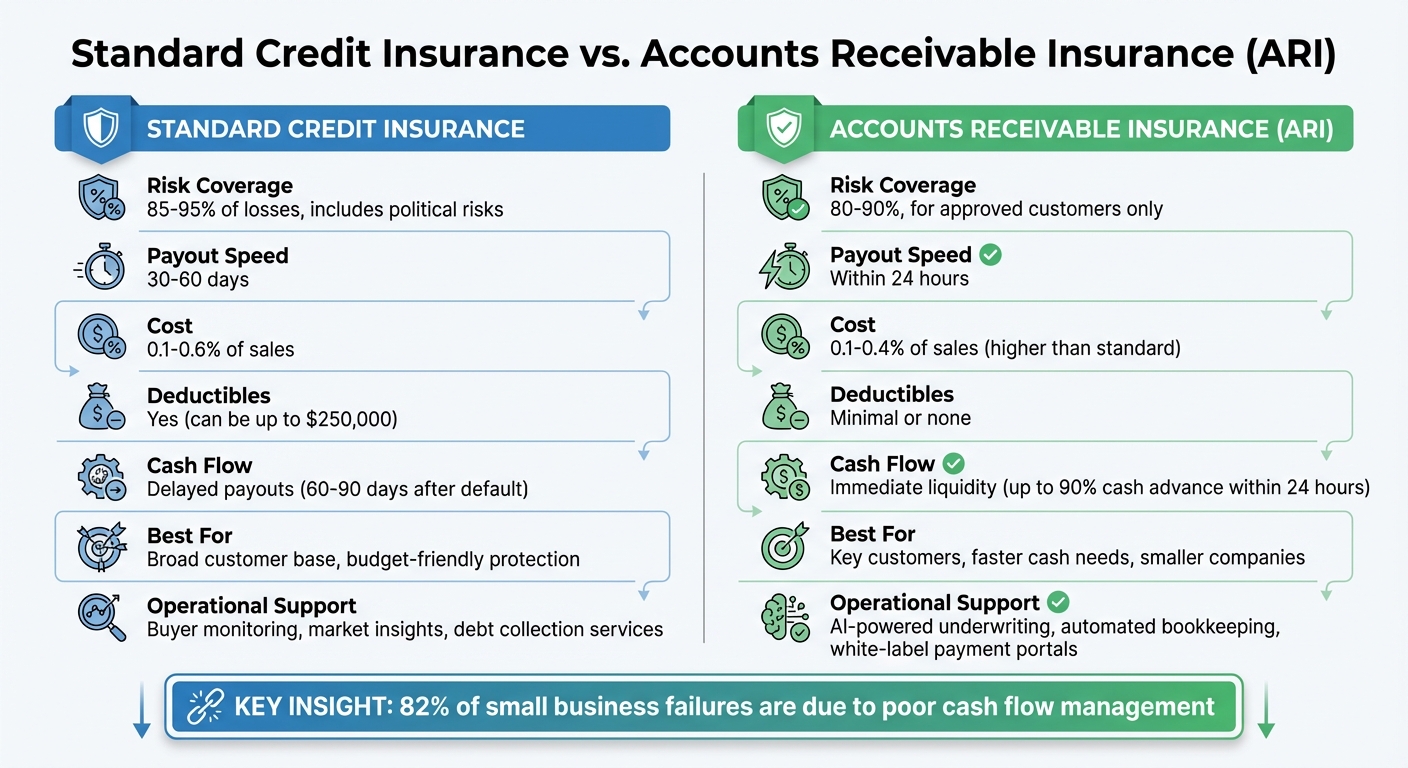

Standard Credit Insurance vs Accounts Receivable Insurance (ARI) Comparison

Using credit insurance to offer competitive payment terms

sbb-itb-2d170b0

How Credit Insurance Supports Longer Payment Terms

Credit insurance helps businesses manage the risk of customers not paying their invoices. When you offer extended payment terms, like net 60 or net 90 days, credit insurance can cover up to 90% of unpaid debts if a customer becomes insolvent or delays payment for an extended period. This allows you to provide more flexible terms to your customers without putting your company’s financial health at risk.

Specialized underwriting plays a key role in this process. Insurers conduct thorough evaluations of your customers’ financial stability and payment history to set appropriate credit limits. This ensures you can confidently extend credit to customers while minimizing potential losses.

"This kind of insurance helps companies mitigate their risks when they need to provide flexible terms for their international clients. If the customer doesn’t pay, you’ll still receive most of your funds". – Sarah van Wolde, Senior Underwriter at Export Development Canada (EDC)

This careful underwriting doesn’t just protect your business – it can also enhance your financial standing with lenders.

Credit insurance offers another advantage: it can improve your borrowing power. Many banks require credit insurance before approving revolving credit lines because insured receivables are considered less risky. This can result in better loan terms and higher credit limits, enabling you to maintain steady cash flow while waiting for customer payments. For instance, some companies have reported sales increases of up to 20% by safely extending higher credit limits. In 2024, American Trade Finance helped clients expand their credit limits by as much as 10x, managing over $1 billion in authorizations.

Accounts Receivable Insurance (ARI) takes this a step further by tailoring policies to your needs. It includes options like Discretionary Credit Limits for smaller, unnamed buyers and specific limits for key accounts. ARI also continuously monitors your customers’ financial health and steps in when defaults occur, managing tasks like creditor meetings, renegotiating payment schedules, and recovery efforts.

The benefits extend beyond domestic operations. Credit insurance makes it easier to offer competitive open account terms in international markets, where collecting payments can be complicated by different legal systems. ARI providers also offer localized insights and intelligence on foreign customers, helping you navigate political and economic uncertainties. These tools make expanding into new markets far less risky and much more manageable.

1. Standard Credit Insurance

Standard credit insurance builds on earlier concepts by focusing on specific coverage options, cash flow benefits, costs, and operational details.

Risk Coverage

Standard credit insurance safeguards your business from customer defaults caused by insolvency, bankruptcy, or prolonged non-payment. It also covers political risks, including embargoes, war, riots, and currency issues that prevent payment.

Through programs like those offered by the Export-Import Bank of the United States (EXIM), businesses can typically recover 85% to 95% of the invoice amount when a buyer defaults. You can choose to insure your entire customer base (whole turnover), specific high-risk accounts, or even a single large transaction (single buyer insurance). These coverage options directly impact your working capital, as explained below.

Impact on Cash Flow

Standard credit insurance provides a safety net for your working capital. With this coverage, you can confidently extend 30-, 60-, or 90-day payment terms without worrying that a single default could cripple your cash reserves.

Additionally, insured receivables are viewed as high-quality collateral by banks, which can help you secure better borrowing terms. This means you may be able to borrow more against your accounts receivable and at lower interest rates. However, it’s important to note that claims payouts usually take 30 to 60 days after the waiting period, so cash flow delays aren’t entirely eliminated.

Cost and Profitability

The cost of standard credit insurance is relatively low, with premiums typically under 1% of your insured sales volume. Minimum annual premiums start at around $3,500, while monthly premiums generally range from 0.2% to 0.6% of total insured sales. Businesses with strong credit controls often see costs closer to 0.25% of their projected annual turnover.

This predictable expense offers peace of mind in the face of uncertain non-payment risks. The global trade credit insurance market, valued at $9.39 billion in 2019, is expected to grow to $18.14 billion by 2027, with an annual growth rate of 8.6%. Demand for these policies surged during the 2020 economic downturn as businesses sought protection against market disruptions.

Operational Support

Beyond financial protection, insurers provide ongoing business intelligence and assign credit limits based on the financial health of your buyers. This support enables businesses to confidently enter riskier foreign markets and extend higher credit limits to existing customers.

However, standard policies often include high deductibles – sometimes up to $250,000 – meaning you’ll need to absorb initial losses. Even so, the insights provided by insurers allow you to offer competitive payment terms while maintaining financial stability. This combination of risk management and operational support can be a game-changer for businesses navigating uncertain markets.

2. Accounts Receivable Insurance (ARI)

Accounts Receivable Insurance (ARI) offers a tailored solution that goes beyond standard credit insurance by focusing on the specific needs of your business. This personalized approach is especially helpful for managing risks tied to a small number of key customers or navigating the uncertainties of international trade.

Risk Coverage

ARI shields your accounts receivable from losses caused by customer non-payment or default. It’s particularly effective for handling large, catastrophic losses tied to single accounts, which is crucial for businesses dependent on a few major buyers. This type of coverage is also valuable in international markets, where access to reliable business data or legal recourse may be limited [2,3].

As Sarah van Wolde, Senior Underwriter at Export Development Canada (EDC), puts it:

"This kind of insurance helps companies mitigate their risks when they need to provide flexible terms for their international clients. If the customer doesn’t pay, you’ll still receive most of your funds."

Policies typically reimburse between 80% and 90% of the invoice value [17,18]. However, it’s important to confirm the legal names of your customers to ensure enforceability and coverage. Keep in mind that deductibles can be high – sometimes as much as $250,000 – so not all portions of a large default may be covered.

Impact on Cash Flow

When you offer payment terms of 30, 60, or 90 days, your working capital can be tied up for extended periods. ARI ensures that even if a buyer defaults, you’ll recover most of the owed funds. For domestic claims, payments are typically made within 60 days of the reported loss [2,3,19].

Insured receivables also improve your financial standing with lenders. Banks are often more willing to extend credit at better rates when receivables are backed by insurance. This can help offset the cost of premiums and provide greater financial stability. Additionally, ARI can reduce the size of your Allowance for Doubtful Accounts, enhancing your reported earnings. This cash flow stability is a key benefit that supports the overall value of ARI.

Cost and Profitability

Premium costs for ARI depend on factors like industry risk, customer concentration, and whether your sales are domestic or international [17,19]. On average, businesses pay between 0.1% and 0.4% of their total annual sales for coverage. For instance, a company generating $2 million in annual sales might spend around $5,000 on ARI.

Kirk Elken, Co-founder of Securitas Global Risk Solutions, emphasizes:

"The cost [of ARI] is outweighed by protection against customer defaults and the ability to grow with confidence."

With ARI, you can safely extend longer payment terms to higher-risk customers, potentially capturing sales that would otherwise be lost [2,19]. However, ARI is not a "set it and forget it" solution. Insurers regularly review buyer creditworthiness and may adjust credit limits as new information becomes available. Disputed invoices are not eligible for payouts until the dispute is resolved.

Operational Support

Beyond financial protection, ARI enhances your operational efficiency. Providers offer real-time credit insights and stability metrics, especially for international clients, helping you spot potential payment issues early [2,3].

ARI also encourages a disciplined credit management process. A suggested six-step framework includes:

- Collecting corporate and bank data

- Verifying credit history

- Building direct relationships with customers

- Documenting sales agreements

- Monitoring credit standings annually

- Standardizing overdue account management

When setting credit limits for new customers, it’s wise to start conservatively and increase limits only after establishing trust. Additionally, delinquent accounts are most recoverable within the first 90 days after the due date. Keeping your ARI coverage confidential can also reduce any incentive for customers to default.

Advantages and Disadvantages

This section dives into the strengths and weaknesses of Standard Credit Insurance and Accounts Receivable Insurance (ARI), offering a side-by-side look at how they manage extended payment terms.

When it comes to Standard Credit Insurance, it stands out as a relatively low-cost option for protecting a diverse customer base. Premiums typically range from 0.1% to 0.6% of covered sales. It provides coverage for 85–95% of losses and shields businesses from risks like insolvency, bankruptcy, and political disruptions. However, there are trade-offs. For instance, payouts are not immediate – businesses often have to wait 60 to 90 days after a default to receive compensation. Additionally, policies often include deductibles, meaning your business will need to absorb smaller losses upfront.

On the other hand, ARI is designed for businesses that need quick access to cash. Modern ARI platforms offer near-instant liquidity, with cash advances of up to 90% of an invoice’s value delivered within 24 hours. ARI can cover invoices as low as $1,000, with no minimum thresholds. While ARI tends to be pricier than standard credit insurance, it is still generally more affordable than factoring fees. However, ARI focuses primarily on credit and insolvency risks for approved customers, and it may not cover disputes related to product quality.

Operational support is another area where these two options differ. Standard Credit Insurance often includes features like buyer monitoring, market insights, and debt collection services across your portfolio. In contrast, ARI platforms use AI-powered underwriting to make fast credit decisions and provide tools like automated bookkeeping, collections, and white-label payment portals that maintain your brand identity. Here’s a quick comparison of the two:

| Criteria | Standard Credit Insurance | Accounts Receivable Insurance (ARI) |

|---|---|---|

| Risk Coverage | Covers 85–95% of losses and includes protection against political risks. | Offers non-recourse protection for approved customers, with minimal or no deductibles, for real-time de-risking. |

| Impact on Cash Flow | Payouts are delayed, often taking weeks or months after a default. | Provides immediate liquidity with cash advances up to 90% within 24 hours. |

| Cost | Lower premiums, ranging from 0.1–0.6% of sales. | Higher cost than standard insurance but cheaper than factoring fees. |

| Operational Support | Includes buyer monitoring, market insights, and debt collection services. | Features AI-driven credit checks, automated bookkeeping, and white-label payment systems. |

Ultimately, the best option depends on your business priorities. If you’re looking for budget-friendly, broad protection and can handle delayed payouts, Standard Credit Insurance is a solid choice. However, if immediate cash flow is critical and you need flexibility with extended payment terms, ARI might be the better fit for your operations.

Conclusion

Selecting the right credit insurance strategy hinges on your business’s size and cash flow priorities.

For larger exporters, Standard Credit Insurance offers a practical way to safeguard against major losses, especially when dealing with the complexities of foreign legal systems or political uncertainties. Experts highlight that this type of insurance allows businesses to manage risks while offering flexible payment terms to international clients.

If your business’s primary challenge is cash flow – particularly for smaller companies, where poor cash flow management accounts for 82% of failures – ARI (Accounts Receivable Insurance) can be a game-changer. With cash advances of up to 90% available within 24 hours, ARI helps bridge payment delays and ensures liquidity.

For businesses heavily reliant on a few key customers, balancing financial risk with liquidity is critical. Companies exploring new markets may benefit from the buyer tracking and market insights provided by Standard Credit Insurance. Meanwhile, those needing immediate working capital may find ARI’s fast cash flow solutions more suitable.

FAQs

Will credit insurance let me safely offer net 60 or net 90 terms?

Yes, credit insurance can provide the confidence to offer net 60 or net 90 payment terms by protecting your business against the risk of non-payment. It safeguards your finances if customers encounter issues like bankruptcy or other payment difficulties. With this coverage, you can extend longer payment terms while reducing the worry of potential losses.

What can prevent a claim payout (like disputes or credit-limit issues)?

Issues like disputes between buyers and sellers, late claim submissions, misunderstandings of policy terms, coverage exclusions, or mistakes in the application process can sometimes prevent claim payouts. To avoid these hurdles, focus on clear communication, submit claims promptly, and ensure all documentation is accurate and complete.

How do I choose between standard credit insurance and ARI for cash flow?

When deciding between standard credit insurance and Accounts Receivable Insurance (ARI), it all comes down to what your business requires.

Standard credit insurance is a solid option for general risk management, offering protection for 85-95% of unpaid invoices. It’s particularly useful for businesses looking for broad coverage to safeguard their cash flow and support growth.

On the other hand, ARI is designed for companies with more specific needs. It provides customized policies, advanced risk management tools, and export coverage, making it a strong choice for businesses involved in international trade or those needing more tailored solutions.

Think about your business’s priorities – whether it’s broad protection or specialized coverage – to decide which fits best.