When selling internationally, ensuring buyers pay on time is critical. Late payments are a common issue, with 66% of businesses waiting on up to $70,000 monthly and 86% reporting delays on 30% of invoices. To reduce risks, businesses must assess creditworthiness using the 5 Cs of Credit:

- Character: Buyer’s reputation and reliability.

- Capacity: Ability to meet financial obligations.

- Capital: Financial reserves for stability.

- Collateral: Assets to secure credit.

- Conditions: Market and political factors.

Key steps include reviewing audited financial statements, analyzing payment history, and monitoring country-specific risks like economic instability or political sanctions. Tools like trade credit insurance (TCI) can protect against non-payment and provide access to expert insights.

Why it matters: Poor credit management can lead to insolvency, with 82% of small business failures tied to cash flow problems. By combining financial analysis, due diligence, and insurance, businesses can safeguard cash flow and seize opportunities confidently.

How to Conduct Effective Creditworthiness Analysis Using Financial Statements

sbb-itb-2d170b0

Assessing the Financial Health of International Buyers

Financial Statement Types Reliability Comparison for International Trade Credit Assessment

Before offering credit to an international buyer, it’s crucial to get a clear picture of their financial health. This involves examining their core financial statements and understanding their payment behaviors to gauge their ability to meet financial obligations.

Reviewing Financial Statements

Start by analyzing the four key financial statements: the balance sheet, income statement, statement of cash flows, and statement of shareholders’ equity. Each provides unique insights:

- The balance sheet reveals the company’s assets, liabilities, and equity, giving a snapshot of its leverage and liquidity.

- The income statement tracks revenue and expenses, helping you understand profitability trends.

- The statement of shareholders’ equity shows changes in net worth, including retained earnings and distributions.

- The statement of cash flows is particularly important. As NACM explains, it "gives the reader the true picture of the sources of cash… and the uses of that cash". A company might appear profitable on paper due to accrual accounting but lack the cash to pay suppliers. If net income consistently exceeds operating cash flow, it could indicate inflated earnings.

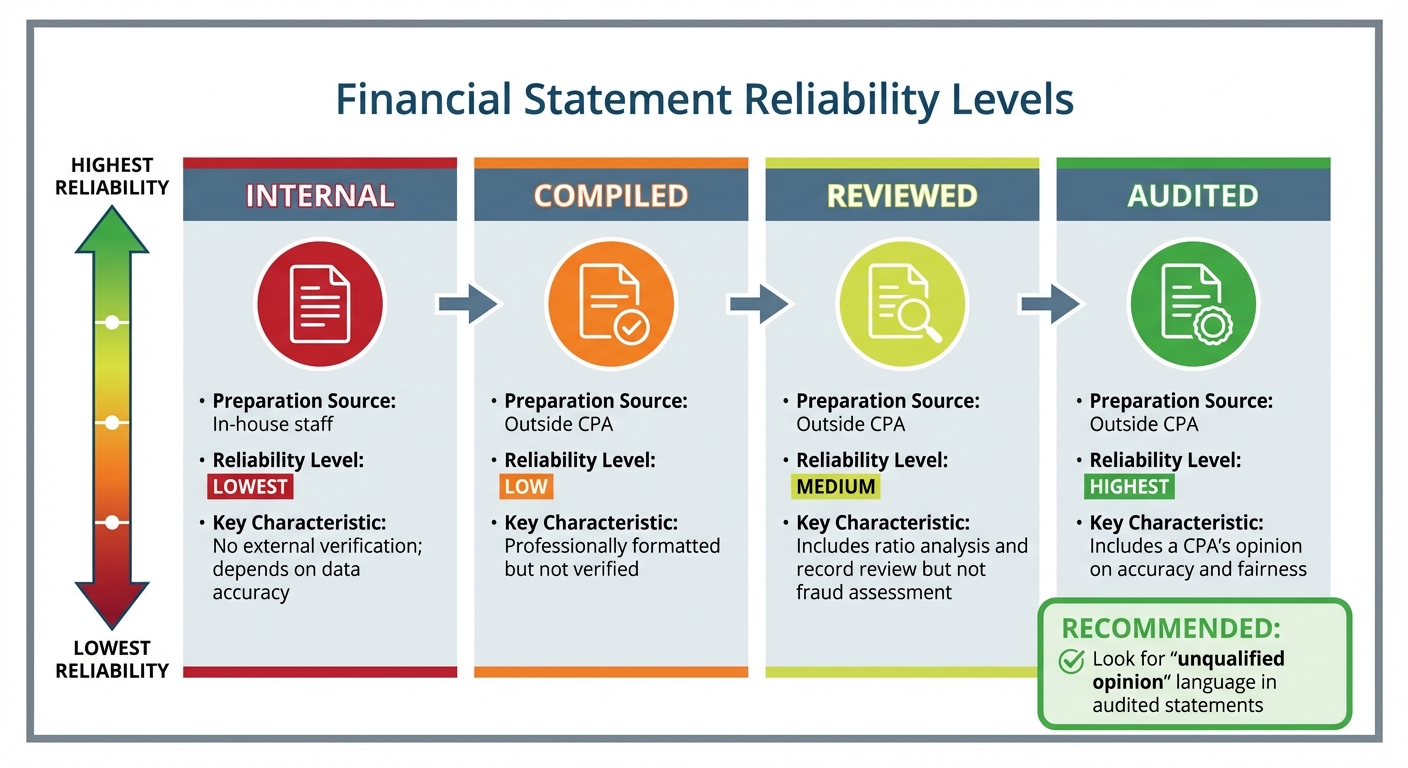

Charles Edwards, CCE, emphasizes the importance of audited financial statements, stating, "an unqualified opinion… is the language you want to see in the cover letter of your audited financial statements". The table below shows the reliability of different financial statement types:

| Statement Type | Preparation Source | Reliability Level | Key Characteristic |

|---|---|---|---|

| Internal | In-house staff | Lowest | No external verification; depends on data accuracy. |

| Compiled | Outside CPA | Low | Professionally formatted but not verified. |

| Reviewed | Outside CPA | Medium | Includes ratio analysis and record review but not fraud assessment. |

| Audited | Outside CPA | Highest | Includes a CPA’s opinion on accuracy and fairness. |

Pay attention to red flags, such as continuous losses over multiple periods, which suggest more money is going out than coming in. Ratios can also reveal risk:

- A current ratio or quick ratio below 1.0 signals the buyer may struggle to meet short-term obligations.

- A debt-to-equity ratio of 2.0 indicates $2 in debt for every $1 in equity, which should be compared to industry norms. A negative ratio points to insolvency and high default risk.

Don’t skip the notes to financial statements. These often disclose critical details like debt repayment terms, contingent liabilities, and inventory valuation methods. Additionally, review accounts receivable and payable aging reports to identify payment trends. Pursuit notes, "in general, the older a debt is, the less likely it is that it will be paid". If a buyer’s customers are slow to pay, that could indicate they’ll have trouble paying you.

To confirm the buyer’s identity, use a D-U-N-S Number and request supporting documents such as bank and trade references, as well as tax returns. Pair this with a detailed review of their payment history for a fuller picture.

Checking Payment History

Once you’ve reviewed the financial documents, take a closer look at the buyer’s payment history. Past behavior often predicts future reliability. Philip Hale, Senior Product Manager at Experian, highlights the importance of due diligence, stating, "doing business on today’s global stage requires a due diligence strategy that helps you minimize financial and credit risks at every stage of the export process".

Accounts receivable aging reports are a key tool for this. These reports categorize unpaid invoices into time buckets: Current, 1-30 days, 31-60 days, 61-90 days, and over 90 days past due. A high volume of overdue invoices (60+ or 90+ days) can indicate collection problems. To measure how quickly a buyer converts sales into cash, calculate the average collection period (ACP) using this formula:

(Accounts Receivable / Annual Sales) × 360.

A longer ACP suggests higher investment in receivables and potential liquidity risks. Additionally, compare the AR to sales ratio (Monthly Accounts Receivable / Monthly Sales) to see if receivables are growing faster than revenue.

For seasonal businesses, compare data to the same period from the previous year to avoid misleading conclusions. For high-value accounts, contact customers directly to verify balances and identify disputed invoices or unapplied payments. Watch for patterns in credit notes and write-offs – frequent disputes may signal deliberate payment delays. When dealing with international wire transfers, confirm when funds clear rather than relying on initiation dates, as timing discrepancies can skew records.

As CreditManagement-Tools.com advises, "prevention is better than cure… It is preferable to identify the risks of non-payment as early as possible rather than battling in costly litigation following unpaid debts". During times of economic uncertainty, focus more on short-term liquidity risks and immediate cash forecasts rather than long-term stability. Using standardized credit reports can help ensure consistency, as creditworthiness standards vary across countries.

Analyzing payment trends alongside financial statements provides a clearer picture of a buyer’s credit behavior. Since 82% of small business failures are attributed to cash flow problems, this step is essential for mitigating non-payment risks in international trade.

Analyzing Country and Political Risks

Evaluating buyer financials is only part of the equation when it comes to international transactions. Just as important is understanding country and political risks, which can undermine even the most financially stable buyers. A company with strong cash flow might still default if government-imposed currency controls, political violence, or economic instability disrupt their ability to pay. As the International Monetary Fund points out, "Creditworthiness appears to be determined primarily by economic variables". Yet, political events often play a significant role in payment reliability. Assessing these risks is a crucial step in fully understanding buyer creditworthiness in global trade.

Reviewing Economic and Trade Stability

To gauge a country’s financial health, start by analyzing key macroeconomic indicators like GDP growth, inflation, interest rates, and external debt. A country’s current account balance and export performance are also critical because they reveal whether it generates enough foreign currency to meet international payment obligations. By early 2026, central banks have eased interest rates in response to moderated global inflation, while trade dynamics remain influenced by rising protectionism and ongoing conflicts in regions like the Middle East and Eastern Europe.

Risk ratings from organizations like the OECD and Allianz Trade provide a structured way to assess country risk. The OECD uses an eight-tier system (0 to 7), while Allianz Trade employs a six-level scale (AA to D). These ratings factor in structural and financial indicators, including business climate quality, regulatory frameworks, corruption control, and short-term financial flow risks that could signal immediate payment challenges.

One critical element to watch is transfer and convertibility risk, which reflects the likelihood of government-imposed capital or exchange controls. According to the OECD, "Country risk encompasses transfer and convertibility risk… and cases of force majeure (e.g. war, expropriation, revolution, civil disturbance, floods, earthquakes)". Even a buyer with sufficient funds may be unable to convert local currency into U.S. dollars to make payments. Resources like the U.S. Commercial Service’s "Country Commercial Guides" and the Ex-Im Bank’s "Country Limitation Schedule" can help identify markets where financial support is limited.

While economic indicators often point to long-term risks, political events can cause immediate disruptions to payments.

Managing Political Risks

Political instability – whether in the form of war, unrest, or terrorism – can disrupt business operations and lead to defaults. Similarly, government actions like nationalization or expropriation can strip buyers of essential assets. Recent nationalizations in Burkina Faso and Niger are stark examples of how asset seizure can impact payment reliability.

Sanctions are another factor to consider. For instance, sanctions following the 2022 Ukraine invasion disrupted global financial systems and supply chains, halting trade in some cases. In July 2024, a Russian Supreme Court ruling further complicated international trade by barring the enforcement of arbitration awards from "unfriendly" countries, leading to increased government refusals to honor international rulings. These examples highlight how quickly political shifts can turn a reliable buyer into a payment risk.

To mitigate these risks, diversifying export markets can help reduce overexposure to any single region. Spreading trade efforts across areas with varying risk levels can cushion against sudden disruptions. Tools like Transparency International’s Corruption Perceptions Index can also provide insight into fraud risks and the strength of legal systems in a buyer’s country. As Roberto Bergami, Senior Lecturer at Victoria University, wisely notes, "a rogue customer in a good country is not a much better risk than a good customer in a rogue country".

For businesses operating in high-risk markets, trade credit insurance can safeguard against unpaid invoices caused by political instability. For broader protection, Political Risk Insurance can cover risks like expropriation and currency inconvertibility. These strategies are essential for maintaining stability in unpredictable environments.

Conducting Due Diligence and Credit Scoring

Once you’ve assessed country and political risks, the next step is verifying the buyer’s legitimacy and compliance. This process sets the foundation for building a reliable credit scoring system to classify risk consistently.

Verifying Legal and Compliance Requirements

Start by confirming the buyer’s legal registration. You can request an International Company Profile (ICP) from the U.S. Commercial Service, which provides a detailed credit report within about 15 days. This document helps verify the buyer’s legitimacy and offers insights into their operations.

It’s also essential to conduct sanctions screening to ensure the buyer isn’t involved in activities like transshipping goods to U.S.-embargoed countries, such as Syria. Credit reporting agencies like Dun & Bradstreet, which have data on over 240 million companies globally, can help identify potential red flags. Additionally, verifying the buyer’s physical operating address is a good way to rule out the possibility of dealing with a shell company.

"Knowing your market, the type of buyer you are selling to, i.e., whether they are end-users, consumers or industrials and getting to know all about your buyer and their culture." – Gabriel Ojeda, President, Fitz-Pak Corporation

Next, gather bank and trade references. With a signed release form, you can access the buyer’s bank information, including details like average daily balances and overdraft history. For trade references, request at least two or three from current suppliers. Use a standardized form to capture critical details such as "Highest Credit Outstanding", "Terms of Sale", and whether payments are typically made within 30 days – an important benchmark for international trade.

Once compliance checks are complete, you’re ready to focus on quantifying risk through a robust credit scoring system.

Building a Credit Scoring System

Effective due diligence paves the way for a detailed credit scoring system that evaluates both financial and qualitative risks. A well-rounded system considers financial ratios, payment history, buyer reputation, and industry standing to classify risk levels. One commonly used framework is the "5 Cs of Credit":

- Character: Assessed through trade references and credit history.

- Capacity: Determined using debt-to-income ratios, with a ratio below 36% generally seen as favorable.

- Capital: Evaluated via certified balance sheets and profit-and-loss statements, particularly for credit limits exceeding $100,000.

- Collateral: Includes assets like equipment or accounts receivable that could be liquidated in case of default.

- Conditions: External factors such as economic stability and political risks.

Business credit scores typically range from 1 to 100, with scores above 75 indicating lower risk. However, a static score is just a snapshot in time. Trend analysis is equally important – look at whether the buyer’s performance is stable, improving, or declining compared to industry benchmarks. Modern tools, including AI and machine learning, can analyze large datasets to detect early warning signs of financial trouble.

"A good credit score does not necessarily mean a customer is a low risk. Even with a stellar credit history, any business or individual faced with significant or unexpected economic hardships is at risk of default." – Allianz Trade

One thing to watch out for is selection bias. Buyers often provide references from suppliers they pay on time while leaving out those they pay late. To get a clearer picture, cross-check information from multiple sources and monitor performance continuously rather than relying on a single snapshot. This approach ensures a more accurate understanding of the buyer’s risk profile.

Using Trade Credit Insurance for Risk Protection

How Trade Credit Insurance Protects Your Business

Trade credit insurance (TCI) offers a safety net for businesses dealing with international buyers, shielding them from the financial fallout of buyer defaults. This is crucial when you consider that 25% of bankruptcies are linked to unpaid invoices. On top of that, 80% of companies worldwide experience late payments from their partners.

But TCI isn’t just about protecting against bankruptcies. It provides two key types of coverage:

- Commercial risk coverage: This protects against issues like insolvency or "protracted default", where buyers pay significantly late – or not at all – after the agreed period.

- Political risk coverage: This covers events beyond the buyer’s control, such as war, civil unrest, currency issues, or sudden regulatory changes.

Major players like Allianz Trade keep an eye on 83 million companies in 160 countries, delivering real-time credit data to help businesses stay informed.

Beyond protection, TCI offers practical benefits. It simplifies debt collection and opens doors to better financing. Banks often view insured receivables as lower-risk assets, which can lead to improved financing terms, including lower interest rates. Additionally, TCI provides access to global databases and local experts who can verify the creditworthiness of foreign buyers – insights that would otherwise be difficult to gather on your own.

"Trade credit insurance is a package of tools offered to the credit managers including assessment and monitoring of the buyer, debt collection and indemnification of unpaid debts." – ICISA

TCI can even become a strategic advantage. By offering extended or more flexible credit terms to international customers, you can stand out from competitors who demand upfront payments. However, it’s worth noting that TCI doesn’t cover payment disputes, such as claims of undelivered goods. Resolving such disputes directly with buyers is essential before involving your insurer.

For businesses looking for even more tailored protection, specialized policies like Accounts Receivable Insurance provide a way to align coverage with specific risks.

Tailoring Policies with Accounts Receivable Insurance

While standard TCI policies often follow a one-size-fits-all approach, Accounts Receivable Insurance (ARI) focuses on customizing coverage to suit your business’s unique needs. This approach allows you to address specific risks in your receivables portfolio, whether you’re managing domestic transactions, international exports, or a blend of both.

There are several policy structures to choose from:

- Whole Turnover: Covers your entire receivables portfolio, ideal for businesses handling high volumes and seeking broad protection.

- Key Accounts: Focuses on high-value customers who are critical to your operations, particularly useful if a few major clients account for a large portion of your revenue.

- Single Buyer: Protects trade receivables from one key client or transaction, perfect for high-value, one-off deals.

ARI also connects you to a global credit insurance network, offering local expertise and market-specific underwriting intelligence. This includes proactive monitoring of your customers’ financial health, with real-time alerts on regional risks or downgraded buyer ratings.

"Accounts receivable (trade credit) insurance is not a one-size-fits-all solution; we work with you to design a policy that aligns perfectly with your business model and risk tolerance." – Accounts Receivable Insurance

Using trade credit insurance can even help grow your sales. By extending credit more confidently, businesses have seen sales increase by up to 20%. ARI can cover up to 95% of unpaid trade receivables when dealing with international clients. Plus, specialized brokers like ARI often provide their services at no additional cost to your business, as they’re compensated by the insurance carriers.

Setting and Monitoring Credit Limits

Determining Initial Credit Limits

Finding the right credit limit from the start is a balancing act between opportunity and risk. To guide this process, use the 5 Cs: Character, Capacity, Capital, Collateral, and Conditions – a well-established framework for credit decisions. Business credit scores, which typically range from 1 to 100, can be helpful here. A score of 75 or higher is generally considered strong.

To ensure buyers can handle credit responsibly, ask for 2–3 trade and bank references. This step helps verify whether they consistently pay within 30 days.

"A buyer with a strong financial position is less likely to default, allowing for higher credit limits." – Anthony Wolff, Dynamic Business Information

Set limits based on the buyer’s typical order size and frequency. This minimizes unnecessary risk exposure. For credit limits under $100,000, a basic credit check is usually sufficient. However, for larger amounts, it’s wise to dig deeper by reviewing the buyer’s latest balance sheet and profit/loss statement. If you’re dealing with cross-border transactions, these limits can help manage payment risks. For buyers in high-risk regions, external guarantees – like bank guarantees or letters of credit – can justify higher credit limits while reducing your exposure.

Reviewing and Adjusting Limits

Once the initial credit limits are set, ongoing monitoring is critical to staying ahead of potential risks. Regular reviews ensure that credit limits remain aligned with the buyer’s financial health and changing market conditions. Just as you assess risks initially, continuous evaluations help keep your safeguards effective.

"Credit risk management is a continuous process of identifying risks, evaluating their potential for loss and strategically guarding against the risks of extending credit." – Allianz Trade

Conduct quarterly account reviews using a mix of manual checks and risk management software. This approach helps identify warning signs like financial struggles, late payments, or negative business news. Group buyers by risk level and adjust their credit limits accordingly. Monthly or quarterly reviews of accounts receivable aging reports are also useful for tracking overall exposure. Watch out for concentration risk – relying too heavily on a single large client could strain your cash flow if they default. For buyers with a strong track record of on-time payments, consider increasing their limits. On the flip side, reduce limits quickly if there are signs of financial trouble.

Conclusion

Safeguarding your international trade operations requires a proactive approach, blending financial reviews, risk assessments, and strategic tools like trade credit insurance. By consistently evaluating trade creditworthiness, businesses can protect cash flow and maintain smooth operations, even in the face of challenges like late payments or economic uncertainty.

The 5 Cs of Credit – Character, Capacity, Capital, Collateral, and Conditions – serve as a solid foundation for assessing buyer reliability. Combining internal evaluations with third-party insights provides a clearer picture of potential risks. Persistent late payments, a common hurdle in cross-border trade, further highlight the importance of robust credit management.

"Effective credit risk management is imperative to the success of your business." – Allianz Trade

International trade also comes with added complexities, such as currency shifts, political uncertainty, and differing legal systems. Trade credit insurance (TCI) offers a dual benefit: protection against non-payment and access to extensive risk databases. And the cost? Typically, it’s just a fraction of 1% of your sales volume.

"Trade credit insurance emerges as a critical tool for businesses engaged in international trade. By protecting against the non-payment of receivables, TCI safeguards the lifeblood of a business, its cash flow." – ARI Global

For a more tailored approach, Accounts Receivable Insurance (ARI) offers customized policies designed to meet both domestic and international needs. Their services include detailed risk assessments, claims management, and connections to a global network of credit insurance providers. This personalized support empowers businesses to extend competitive payment terms while managing risk effectively.

FAQs

What are the biggest red flags in a buyer’s financial statements?

Key warning signs in a buyer’s financial statements include irregular cash flow, high levels of debt, overstated or fluctuating asset values, hidden liabilities not listed on the balance sheet, and evidence of manipulated accounting practices. These factors can point to financial instability or raise concerns about creditworthiness, particularly in the context of international trade.

How do I factor country and political risk into a credit decision?

When making a credit decision, understanding country and political risks is crucial. Start by examining key factors such as political stability, economic conditions, legal systems, foreign exchange risks, and potential government actions. These elements help paint a clearer picture of the risks involved.

Keep an eye out for warning signs like political unrest, natural disasters, or trade restrictions that could impact the credit environment. To make this process more precise, use tools like risk classifications to measure and quantify these risks effectively.

For additional security, consider adjusting credit terms to reflect the level of risk. Another option is to explore trade credit insurance solutions, such as Accounts Receivable Insurance, which provides an extra layer of protection against potential losses.

When should I use trade credit insurance instead of tighter payment terms?

Trade credit insurance can be a smart alternative to tightening payment terms when you need to balance risk management with offering competitive payment options. It’s particularly helpful if you want to extend flexible terms like open accounts or delayed payments, as it provides protection against non-payment stemming from issues like insolvency, bankruptcy, or political uncertainties. This strategy is especially beneficial when dealing with new or higher-risk buyers, allowing you to expand sales opportunities while maintaining a secure financial position.