When your business operates in unstable regions, unexpected political events – like currency crises, government actions, or violence – can disrupt payments and jeopardize investments. Political Risk Insurance (PRI) and Accounts Receivable Insurance (ARI) are two key tools to protect your trade credit and assets. Here’s a quick breakdown:

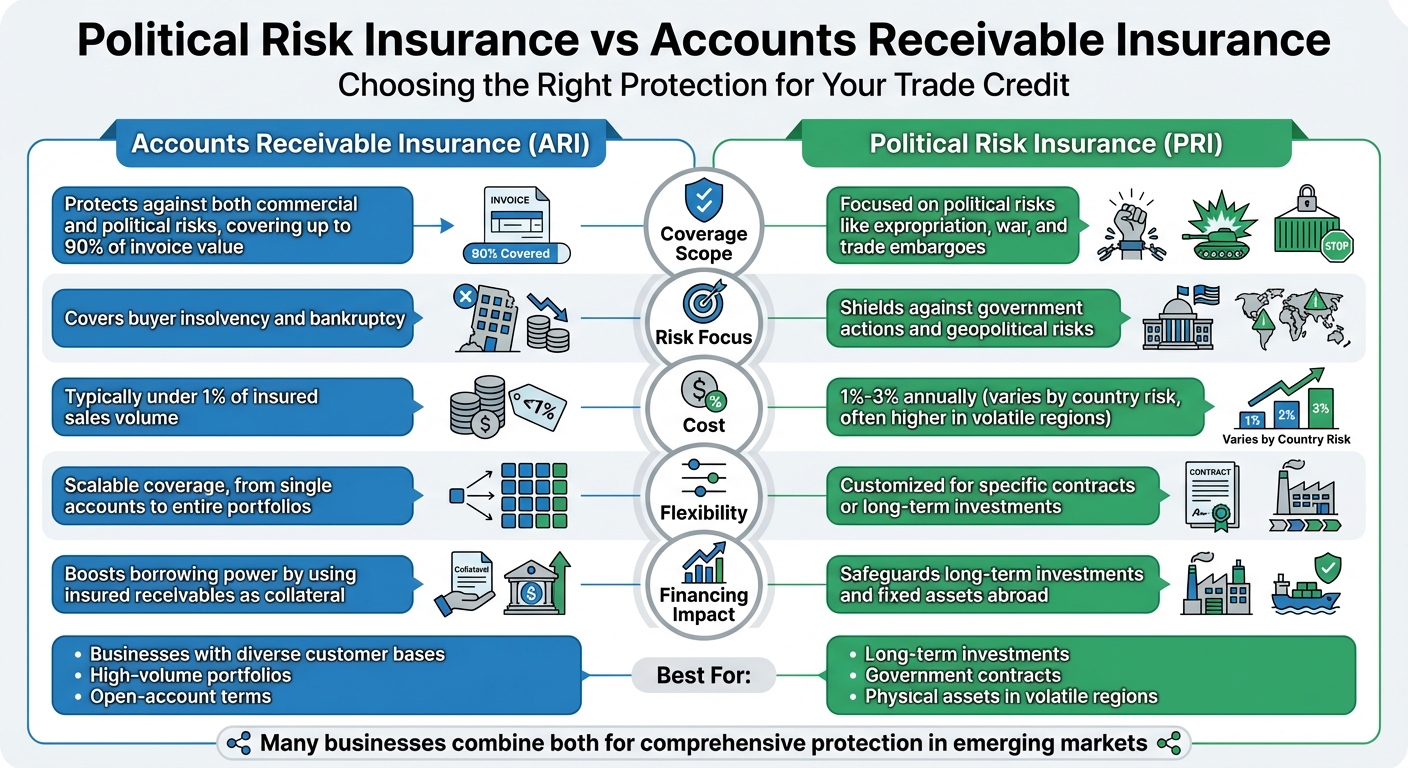

- PRI: Focuses on risks from political events (e.g., expropriation, currency inconvertibility, political violence). Ideal for long-term investments or government contracts in volatile regions. Costs typically range from 1%–3% of insured value annually.

- ARI: Covers both commercial (e.g., buyer insolvency) and political risks for receivables. Suitable for businesses with diverse customer bases. Premiums are often under 1% of insured sales.

Both options can stabilize cash flow, reduce borrowing costs, and provide peace of mind. Choosing the right coverage depends on your risk exposure, market focus, and financial goals. For many businesses, combining PRI and ARI offers the best protection.

1. Political Risk Insurance (PRI)

Coverage Scope

Political Risk Insurance (PRI) offers protection against government actions and political events that disrupt payments from buyers. This includes scenarios like expropriation, currency inconvertibility, and political violence. It also provides trade-specific safeguards, such as coverage for canceled export or import licenses, trade sanctions, and government decrees that prevent goods from being imported. Some policies extend to "Breach of Contract" coverage, which applies when a host government denies legal recourse or fails to honor an arbitration ruling. For exporters dealing with custom-made goods, a "Pre-Shipment endorsement" can cover manufacturing costs if something like a license cancellation occurs during production.

This detailed coverage framework is essential for understanding how PRI adapts to market needs and calculates risk-based pricing.

Risk Focus

Unlike commercial insurance, which addresses operational risks like buyer insolvency, PRI zeroes in on political events and government actions. Its demand is primarily driven by businesses operating in higher-risk regions, especially emerging markets. PRI is designed to quantify and price rare but impactful events – such as coups or currency crises – making it a vital tool for companies managing trade credit in volatile areas.

A study by the Berne Union and ICISA revealed that 75% of respondents believe political risks are on the rise. However, only 27% of companies that suffered political risk-related losses in 2025 had adequate insurance coverage, highlighting a notable gap in protection.

Cost and Flexibility

The cost of PRI generally falls between 1% and 3% annually, though rates for large infrastructure projects in BBB-rated countries can range from 0.5% to 1.5% per year. Policies often come with a 10% deductible, and insurers can quickly tailor coverage to address specific risks in individual countries. Private insurers offer coverage limits of up to $190 million per political risk for periods as long as 10 years. The total private market capacity for a single risk is estimated at about $2.226 billion. This predictable pricing helps exporters manage their financial planning more effectively.

"PRI translates uncertainty about political risk into premium amounts, allowing the investor to make an investment decision based on the economics rather than just perceptions." – Shardul Amarchand Mangaldas & Co

"Pricing for political risk has remained stable" – Dan Riordan, Head of Political Risk and Credit at MSIG USA

Suitability for Emerging Markets

PRI is especially valuable in developing countries where political instability tends to be higher. For example, a Country Risk Investment Model study found that PRI reduced Ghana’s project risk premium from 6.30% to 2.23%. This reduction can make the insurance cost worthwhile, even before considering the potential benefits of claims.

Beyond risk reduction, PRI enhances project bankability. For instance, it can improve the simulated S&P rating of a B-rated project in a developing country to BBB. As Matthew Newman from the Lowy Institute explains:

"PRI reframes geopolitical problems as an opportunity to expand into new geographies and/or asset classes, gaining competitive advantage over unprotected rivals"

With around 80% of multinational corporations planning to incorporate geopolitical risk mitigation strategies within the next five years, PRI is evolving from a niche offering to a standard part of cross-border risk management.

sbb-itb-2d170b0

2. Accounts Receivable Insurance (ARI)

Coverage Scope

Accounts Receivable Insurance (ARI) shields businesses from both commercial risks – like customer insolvency, bankruptcy, or delayed payments – and political risks, such as currency inconvertibility, expropriation, political violence, or government interventions. Policies typically cover between 80% and 95% of the invoice value. Companies can select from various policy types: the Whole Turnover option covers the entire receivables portfolio; the Export Credit Subset focuses on receivables tied to international trade; and Single Buyer coverage protects against risks associated with a specific high-value client. This range of options offers businesses flexibility in managing their receivables and mitigating risks.

Risk Focus

ARI goes beyond basic coverage by addressing risks from both commercial failures and political disruptions. Unlike Political Risk Insurance (PRI), which primarily focuses on political events, ARI takes a more integrated approach, covering all payment-related risks. This is particularly important because commercial and political risks often overlap – civil unrest or a currency crisis can lead to widespread buyer insolvencies or delays in payments from otherwise solvent customers.

Insurers are increasingly using AI tools to enhance risk assessments, particularly as businesses shift their focus to domestic and developed markets to navigate high default risks in some emerging economies. Despite geopolitical uncertainties, like the ongoing Russia–Ukraine conflict and tensions in the China–Taiwan region, the trade credit insurance market remains competitive, with high capacity and favorable pricing. In 2025, the global market grew to $13.3 billion, up from $12.2 billion in 2024, although only about 15% of global trade is insured.

Cost and Flexibility

The financial benefits of ARI are significant. While Single Buyer policies often come with higher premiums due to the concentrated risk, the investment can reduce borrowing costs and minimize bad-debt reserves. As Marc Wagman, Managing Director of Credit and Political Risk at Gallagher, puts it:

"Receivables – the lifeblood of a company fueling cash flow – are the largest uninsured asset on the balance sheet. Having the insurance greases the wheels of global trade."

Insured receivables are considered lower-risk collateral by banks, which can lead to better interest rates and more favorable credit terms. Companies using ARI have reported up to a 20% boost in sales by safely offering larger credit terms. Additionally, some brokers are compensated directly by insurers, allowing businesses to access expert advice without extra costs.

Suitability for Emerging Markets

In regions where credit data is scarce, ARI plays a crucial role in helping exporters compete. By enabling open account terms instead of restrictive Letters of Credit, ARI allows exporters to match or exceed the flexibility offered by local competitors. Insurers also provide ongoing monitoring of foreign buyers’ financial health, a key service in markets with limited or opaque credit information. Sarah Murrow, President and CEO of Allianz Trade Americas, emphasizes this point:

"Trade credit insurance is vital to keeping liquidity in supply chains… It is the glue that keeps world trade going."

ARI also addresses specific challenges in emerging markets, such as currency inconvertibility and political violence, which can disrupt payment processes. With major providers controlling about 70% of global risk capacity, businesses gain access to robust financial backing, even in the most volatile regions.

Advantages and Disadvantages

Political Risk Insurance vs Accounts Receivable Insurance Comparison

Choosing between Accounts Receivable Insurance (ARI) and Political Risk Insurance (PRI) depends largely on your specific risk profile. Both options have their own strengths and limitations when it comes to coverage, cost, and flexibility.

ARI provides a broad safety net, combining protection against both commercial failures and political disruptions. This makes it ideal for companies with diverse customer bases operating across multiple markets. On the other hand, PRI zeroes in on risks stemming from government actions and geopolitical instability, such as expropriation or war. While PRI offers a more focused approach, its narrower scope may not suit every business. The key is to align your choice with your market exposure and risk management strategy.

From a cost perspective, ARI is typically affordable, with premiums usually under 1% of insured sales. This makes it a cost-effective option for protecting cash flow. In contrast, PRI costs can vary significantly, especially in regions with higher political volatility, where premiums tend to rise. As Jerry Paulson, Senior Vice President at HUB International, explains:

"Trade credit insurance absolutely should be on a risk manager’s radar… it helps solve this dilemma by covering the risk of unpaid invoices caused by a customer’s insolvency."

Flexibility is another point of distinction. ARI offers scalable coverage, ranging from single accounts to an entire portfolio, making it a versatile choice for businesses of all sizes. PRI, however, is tailored for specific, long-term contracts or investments, which may be more suitable for companies with high-risk international ventures. During periods of market uncertainty, ARI’s broad coverage can help stabilize cash flow by protecting a significant portion of receivables.

Here’s a quick comparison of the two options:

| Feature | Accounts Receivable Insurance (ARI) | Political Risk Insurance (PRI) |

|---|---|---|

| Coverage Scope | Protects against both commercial and political risks, covering up to 90% of invoice value | Focused on political risks like expropriation, war, and trade embargoes |

| Risk Focus | Covers buyer insolvency and bankruptcy | Shields against government actions and geopolitical risks |

| Cost | Typically under 1% of insured sales volume | Varies widely by country risk, often higher in volatile regions |

| Flexibility | Scalable coverage, from single accounts to entire portfolios | Customized for specific contracts or long-term investments |

| Financing Impact | Boosts borrowing power by using insured receivables as collateral | Safeguards long-term investments and fixed assets abroad |

Conclusion

The choice between Accounts Receivable Insurance (ARI) and Political Risk Insurance (PRI) comes down to the specific risks your business faces. If your primary concern is securing cash flow from commercial transactions, particularly in high-volume portfolios prone to buyer insolvency or prolonged payment delays, ARI is a practical solution. On the other hand, PRI is better suited for protecting physical assets, government contracts, or mitigating risks like expropriation and currency inconvertibility. PRI essentially transforms political uncertainties into measurable premiums, allowing you to base investment decisions on clear financial data rather than subjective risk perceptions.

For businesses selling goods on open-account terms to private companies in uncertain regions, ARI offers affordable protection – often costing less than 1% of insured sales. It also enables competitive payment terms, which can be a significant advantage. Meanwhile, PRI is indispensable for those managing long-term investments, physical assets, or government contracts, as it shields against risks like unilateral cancellations or breaches of contract by host governments.

Combining ARI and PRI often provides the most comprehensive coverage, especially for businesses operating in emerging markets. ARI not only secures receivables but can also improve financing options – lenders are more likely to include insured receivables in the borrowing base. At the same time, PRI safeguards physical assets and protects operations from government interference.

Ultimately, aligning your insurance strategy with your specific risk profile ensures your business is protected while maintaining the agility needed to thrive in global markets. Whether you opt for ARI, PRI, or a combination of both, the goal remains to secure your operations and support sustainable growth in an unpredictable environment.

FAQs

How do I choose between PRI and ARI?

The main distinction between Political Risk Insurance (PRI) and Accounts Receivable Insurance (ARI) is the type of protection they offer. PRI focuses on safeguarding businesses against losses caused by political events – think expropriation, war, or trade embargoes. It’s particularly useful when operating in regions with unstable political climates. On the other hand, ARI is designed to cover risks related to non-payment, including buyer insolvency and certain political risks, for both domestic and international transactions.

Your choice depends on the risks you’re most concerned about. If political instability is your primary worry, PRI might be the better fit. If your main concern is ensuring payment from buyers, ARI could be more suitable. For businesses facing a mix of these challenges, combining both types of coverage may offer broader protection.

What counts as a political risk under PRI?

Political risks covered under PRI (Political Risk Insurance) encompass several key areas:

- Government actions: This includes scenarios like expropriation, nationalization, or the seizure of assets by a government.

- Political violence: Events such as war, terrorism, or civil unrest fall under this category.

- Economic disruptions: Issues like currency inconvertibility, trade embargoes, or sanctions are included here.

- Contract-related issues: These involve challenges such as contract frustration, repudiation, or the wrongful calling of guarantees.

Each of these risks highlights potential challenges businesses or investors might face when operating in politically unstable environments.

Can PRI and ARI be used together?

Yes, PRI (Political Risk Insurance) and ARI (Accounts Receivable Insurance) can complement each other to provide well-rounded protection in international trade. While PRI focuses on shielding businesses from political risks, such as government actions or instability, ARI addresses commercial risks like non-payment or buyer insolvency. Together, they help businesses minimize exposure to a wider range of potential challenges.