Navigating global trade in 2026 is harder than ever for retailers. Unpredictable tariffs, supply chain delays, rising bankruptcies, and geopolitical tensions are creating significant financial risks. Trade credit insurance has become a critical tool to protect businesses from these challenges. It safeguards receivables – the largest uninsured asset for many retailers – against non-payment, insolvency, and political disruptions. Here’s what you need to know:

- Tariff Volatility: Sudden changes in tariffs, like the U.S. imposing a 35% tariff on Canadian goods in 2025, make cost forecasting difficult.

- Supply Chain Disruptions: Customs delays and stricter regulations are increasing costs and shrinking margins.

- Rising Bankruptcies: Nearly 48% of global trade receivables are tied to high-risk markets, exposing $1.1 trillion to collection challenges.

- Trade Credit Insurance Benefits: Covers 75%-95% of unpaid invoices, aids in securing better financing terms, and provides insights into buyer risks.

Retailers can choose between multi-buyer policies for broad coverage or single-buyer policies for specific high-risk accounts. Domestic and international options are available, with add-ons like political risk coverage. Premiums typically cost less than 1% of insured sales, offering affordable protection against financial losses. For tailored solutions, consider working with specialized providers to secure your business’s future.

Global Trade Risks for Retailers 2026: Key Statistics and Insurance Solutions

Main Trade Risks for Retailers in 2026

Tariff Changes and Trade Policy Shifts

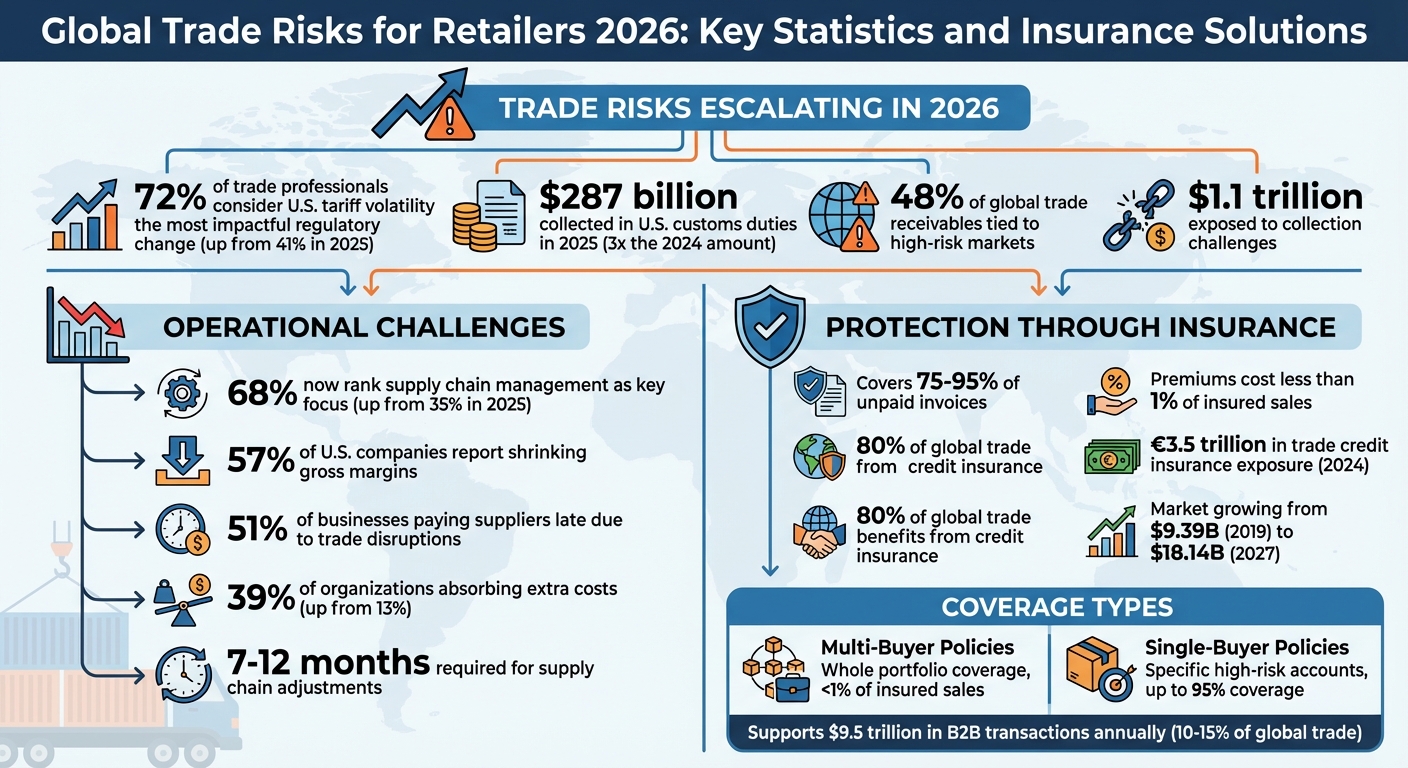

Retailers in 2026 are facing a whirlwind of challenges due to tariff fluctuations. According to recent findings, 72% of trade professionals now consider U.S. tariff volatility the most impactful regulatory change of the year – up significantly from 41% in 2025. The numbers tell a striking story: in 2025, the U.S. government collected $287 billion in customs duties and tariffs, nearly three times the amount recorded in 2024.

The start of 2026 brought dramatic shifts. For example, U.S. tariffs on South Korean goods, including automobiles, lumber, and pharmaceuticals, surged from 15% to 25% in January. Meanwhile, India saw a sharp drop in its tariffs, falling from 50% to 18% in February, following geopolitical negotiations. These changes highlight a growing trend where tariffs are increasingly used as political tools, making trade policy less predictable.

Adding to the complexity, the elimination of the "de minimis" exemption, which previously allowed shipments under $800 to bypass duties, has created bottlenecks at ports. Customs now handle a higher volume of smaller shipments, leading to more frequent delays. This has left 39% of organizations absorbing the extra costs rather than passing them on to consumers – a sharp rise from 13% in the previous year. For retailers, these tariff shifts demand constant adjustments to logistics, further straining supply chains.

Supply Chain Delays and Customs Issues

Supply chain management has become a top priority for businesses in 2026, transforming from a logistical concern into a critical enterprise risk. A striking 68% of trade professionals now rank supply chain management as a key focus, nearly doubling from 35% in 2025. Customs delays have worsened, partly due to stricter enforcement measures like those under the Uyghur Forced Labor Prevention Act, which has led to more frequent detentions of goods.

Adapting to these disruptions isn’t quick. Retailers are finding that supply chain adjustments now take anywhere from seven months to a year. During this transition, businesses face narrower execution windows, leading to missed sales opportunities. On top of that, 57% of U.S. companies report shrinking gross margins due to the higher costs of imported goods. To mitigate risks, many retailers are moving away from "just-in-time" inventory strategies to "just-in-case" models. Nearly half (48%) of businesses have increased their inventory levels, with some boosting stock by as much as 50% to ensure they can weather these challenges.

Supplier Bankruptcy and Non-Payment

Financial instability is adding another layer of risk for retailers. Bankruptcy and non-payment issues are on the rise, with U.S. bankruptcies in early 2025 hitting their highest levels since 2010. This spike is largely tied to the financial strain caused by trade volatility.

Retailers are grappling with two major credit risks: delayed payments, where buyers postpone due to cash flow problems, and outright insolvency, where buyers are unable to pay at all. Economic shocks and tariff hikes only exacerbate these issues, as 51% of U.S. businesses report paying their suppliers late due to recent trade disruptions. These payment delays undermine the stability of receivables, often the largest uninsured asset for retailers.

Another concern is the "invisible stakeholder" risk tied to trade credit insurance. If a retailer’s creditworthiness takes a hit, suppliers may see their insurers cancel or reduce credit limits. This, in turn, forces suppliers to demand upfront payments or even cut off shipments altogether. Ian Watts, Credit Risk Specialty Growth Leader at WTW, explains:

"Most global trade is done on open account terms, where goods are shipped and delivered before payment is due. Companies cannot manage that risk [of non-payment] without trade credit insurance".

sbb-itb-2d170b0

Trade Credit Insurance as a Risk Management Tool

How Trade Credit Insurance Functions

Trade credit insurance serves as a financial safety net for retailers operating in the unpredictable world of global commerce. If a buyer defaults – whether due to insolvency, bankruptcy, or simply failing to pay on time – the policy typically reimburses between 75% and 95% of the unpaid invoice amount. But its protection doesn’t stop there. It also covers political risks, such as war, terrorism, currency restrictions, expropriation, and unexpected changes in trade regulations.

Insurers play an active role in managing risk. They evaluate the creditworthiness of customers, set credit limits for transactions, and continuously monitor the financial health of buyers. Many policies even include professional debt collection services to help recover unpaid funds and reduce losses. For domestic claims, insurers often process payments within 60 days of a reported loss.

The impact of trade credit insurance on global trade is massive. Today, around 80% of global trade benefits from some form of financing or credit insurance, with trade credit insurance exposure reaching a record €3.5 trillion in 2024. This comprehensive safety net not only safeguards businesses from financial losses but also provides operational benefits that enhance their competitiveness.

Benefits for Retail Operations

Beyond its protective role, trade credit insurance offers strategic advantages that can transform retail operations. One key benefit is access to professional credit intelligence. Using a combination of advanced analytics and diverse datasets, insurers provide real-time insights into market conditions and buyer risks – an invaluable resource in volatile markets. This information helps retailers make smarter decisions when extending credit to new customers or exploring unfamiliar markets.

Insured receivables also act as high-quality collateral. Banks and lenders often view these protected assets favorably, which can increase a retailer’s borrowing capacity and secure better financing terms. On top of that, multi-buyer policies are cost-effective, typically priced at less than 1% of insured sales. This is far cheaper than factoring, which can range from 1% to 10% of invoice value. Another financial perk? Trade credit insurance premiums are tax-deductible, unlike reserves set aside for bad debts.

"The ultimate goal of credit insurance is not simply to indemnify losses incurred from a default, but also to provide businesses with the support and knowledge they need to avoid foreseeable losses from the start." – Allianz Trade

By reducing the need for large bad debt reserves, trade credit insurance frees up working capital that can be reinvested into inventory, new markets, or other growth opportunities. It also simplifies compliance with IFRS 9 accounting standards by replacing a buyer’s default probability with the insurer’s higher credit rating, which lowers Expected Credit Loss provisions.

For retailers looking to create a tailored risk management strategy, Accounts Receivable Insurance (https://accountsreceivableinsurance.net) offers customized policies, detailed risk assessments, and ongoing support to help manage both domestic and international exposures effectively.

Tailored Insurance Options for Retail Businesses

Single-Buyer vs. Multi-Buyer Policies

Retail businesses can customize their trade credit insurance to fit their specific needs, especially when it comes to managing customer risk. Retailers generally have two main options: insuring their entire customer portfolio or focusing on specific high-risk accounts.

Multi-buyer policies, also known as "whole turnover" coverage, protect all of a retailer’s domestic or international customers under one comprehensive plan. This type of policy is ideal for businesses with a wide range of customers, especially if they want to use insured receivables as collateral to secure better financing terms.

On the other hand, single-buyer policies are designed to cover risks associated with one particular customer or transaction. This can be a smart choice for retailers heavily reliant on one or two major clients or suppliers, where a single default could have a serious financial impact. Multi-buyer policies, by spreading risk across many customers, often include discretionary limits. These allow retailers to ship to buyers up to a pre-approved amount without needing insurer approval for every transaction. For instance, EXIM Bank‘s multi-buyer policies come with no application fees or annual minimum premiums, though they do require a refundable advance deposit starting at $500.

By choosing between these two policy types, retailers can align their insurance strategy with their business operations, ensuring they are well-prepared for both domestic and international trade challenges.

Coverage for Domestic and International Trade

Trade credit insurance isn’t just about international trade – it’s equally useful for domestic transactions. Domestic policies protect against risks like local insolvencies or extended payment delays, while export policies add coverage for political risks, currency restrictions, and trade embargoes. For retailers, domestic coverage can also help manage risks tied to customer consolidation, where a small number of buyers generate a significant portion of revenue.

EXIM Bank offers policies that cover up to 95% of both commercial and political risks, giving retailers the option to insure their entire buyer portfolio or focus on specific high-risk or high-value accounts. Additionally, modern policies often feature non-cancellable credit limits, ensuring consistent coverage throughout the policy period. This is especially useful for retailers with long-term supply agreements, as it provides greater certainty in financial planning.

Policy Add-Ons and Support Services

Retailers can enhance their insurance coverage with additional policy features and support services. For example, political risk extensions can address "CEND" risks – Confiscation, Expropriation, Nationalization, and Deprivation – as well as losses from government interference or currency restrictions. Coverage for political violence, including terrorism, strikes, and riots, is particularly valuable for retailers with global supply chains.

Insurers also offer proactive services like early intervention and professional debt collection. These services help secure payments before a claim becomes necessary, protecting cash flow and maintaining strong business relationships. Some insurers, such as Allianz Trade, monitor vast databases – tracking over 83 million businesses globally – and send automated alerts when a buyer’s creditworthiness changes.

For retailers with complex portfolios, Excess of Loss (XOL) coverage provides an extra safeguard against catastrophic credit losses that exceed the limits of their primary policy. These policies often reward businesses with strong internal credit management practices by lowering premiums. Companies like Accounts Receivable Insurance specialize in tailoring these features to meet the unique needs of retail businesses, offering access to a global network of credit insurance carriers and ongoing support for both domestic and international risks.

How to Set Up Trade Credit Insurance for Retail

Evaluating Your Risk Exposure

Before diving into trade credit insurance, it’s important to take a close look at your customer base and the risks you might face. Start by auditing your customer portfolio – this includes looking at trade volume, the creditworthiness of your buyers, and any risks specific to your industry. Pay attention to your payment terms and review past payment behaviors to spot patterns of late payments or defaults. Additionally, consider the regions where your trade partners operate. Risks like political instability, currency issues, or trade embargoes can significantly affect your business. With shifting tariffs and geopolitical uncertainties becoming more common, these factors deserve extra attention.

It’s also worth identifying suppliers who already have trade credit insurance. If their credit limits are reduced, it could directly impact your sourcing. Don’t forget to evaluate your internal credit management processes. For instance, if an insurer flags risks by canceling a credit limit, it could result in less credit being extended to buyers. Ian Watts, Trade Credit Growth Leader at WTW, highlights that insurers are paying close attention to sectors like retail, automotive, and metals. Once you’ve identified your risk exposure, you’ll be ready to select and tailor a policy that works for your business.

Choosing and Customizing Your Policy

After assessing your risks, the next step is to choose the right policy structure. Retailers often pick between two main options: whole turnover coverage, which insures your entire portfolio of buyers and spreads out the risk, or selected risks coverage, which focuses on high-value or riskier accounts. If you’re dealing with a one-time, high-value international transaction, a single-transaction policy could be the best fit.

Think about whether your business needs coverage for domestic trade, international trade, or both. Domestic policies typically protect against commercial risks like insolvency or long-term payment delays. Export policies take it further by covering political risks such as confiscation, nationalization, and issues like currency inconvertibility or trade embargoes . Tailor your policy to address specific risks you’ve already identified, such as supply chain disruptions or tariff changes. For many retailers, blended coverage offers a way to create a more comprehensive safety net.

Some policies include discretionary credit limits, which allow you to extend credit to smaller buyers without needing insurer approval – provided you stick to your internal credit guidelines. If you’re working with a high-value buyer and your insurer’s capacity isn’t enough, options like top-up coverage or syndication can provide additional protection.

"The policy coverage also needs to match how your business operates." – Jason Benson, Global Head of Structured Working Capital at J.P. Morgan

Working with specialists, such as Accounts Receivable Insurance, can help you navigate these options and connect with credit insurance carriers that align with your retail needs.

Implementation Timeline and Required Documents

Once you’ve customized your policy, the next step is implementation. Begin by submitting an application that outlines your business needs, financial goals, and credit exposures. Providing accurate documentation is key to securing favorable policy terms. Insurers will usually ask for a list of your key buyers, their requested credit limits, and details about your financial and loss history, including turnover figures and records of past bad debts .

You’ll also need to provide documentation of your internal credit management processes, such as how you handle underwriting, collections, and customer relationships. Include your standard trading terms to ensure everything is enforceable . Policies are generally issued on an annual basis, but they allow for adjustments if you take on new buyers during the year. Once your policy is active, regular updates – like management reports and financial statements – are crucial to maintaining your insurer’s confidence and ensuring your coverage stays intact.

When it comes to costs, premiums for domestic coverage are typically less than 1% of the insured sales volume. For export coverage, premiums may range from 1% to 2% of the credit limits . Most policies also include a minimum premium to account for unpredictable turnover. To get the best rates, consider working with a trade credit insurance broker. They can submit applications to multiple carriers, often at no additional cost to you.

How trade credit insurance secures your business

Conclusion: Building Retail Resilience Through Trade Credit Insurance

Trade credit insurance has become a critical tool for retailers facing the uncertainties of 2026. With U.S. bankruptcies through March 2025 reaching their highest levels since 2010 and tariffs on Chinese imports ranging from 10% to 145% in 2025, protecting receivables is no longer optional – it’s a strategic necessity.

This type of insurance already supports around $9.5 trillion in B2B transactions annually, accounting for 10% to 15% of global trade. The market itself, valued at $9.39 billion in 2019, is expected to nearly double to $18.14 billion by 2027. These numbers highlight the growing recognition of credit risk as a core business asset.

"Receivables – the lifeblood of a company fueling cash flow – are the largest uninsured asset on the balance sheet. Having the insurance greases the wheels of global trade."

– Marc Wagman, Managing Director of Credit and Political Risk at Gallagher

The benefits of trade credit insurance go beyond loss mitigation. It strengthens operational resilience by addressing risks tied to fluctuating tariffs and supply chain disruptions. Insurers provide real-time monitoring of global buyer health, helping retailers steer clear of risky partnerships before problems arise. Additionally, insured receivables can serve as collateral for bank financing, offering a powerful way to optimize working capital.

For retailers looking to safeguard their businesses, Accounts Receivable Insurance offers tailored policies designed to meet unique needs, covering both domestic and international operations. At less than 1% of insured sales, this investment is a practical way to ensure stability and position for growth.

FAQs

What doesn’t trade credit insurance cover?

Trade credit insurance doesn’t step in to handle payment disputes between buyers and sellers or unresolved contractual disagreements. It also won’t cover risks that are specifically excluded in the policy. Common exclusions might include shipments to countries outside the policy’s coverage or receivables from companies where the insured has ownership or control. It’s crucial to carefully review your policy details to fully understand what’s excluded and any limitations.

How do I pick the right credit limits for my buyers?

To determine appropriate credit limits, start by analyzing your buyers’ financial health, payment history, and the risks within their industry. Provide insurers with detailed buyer information, including their payment terms and specific credit requirements, for a thorough review. Based on this data, insurers may decide to fully approve, partially approve, or deny the requested limits.

For international transactions, it’s crucial to account for geopolitical risks that could impact payment reliability. Utilize resources like credit reports and financial statements to make informed decisions, ensuring you strike the right balance between growing sales and managing potential risks effectively.

What causes a claim to be denied or reduced?

Claims can be denied or reduced for several reasons, often tied to missed deadlines, incomplete details, or not following policy terms. For example, filing a claim after the allowed time frame, unresolved disputes over invoices, or failing to meet conditions like ceasing shipment when required can all lead to issues. To avoid these pitfalls, it’s crucial to fully understand your policy’s exclusions, limits, and reporting deadlines. Paying attention to these details can make a big difference in ensuring your claims are processed smoothly.