Construction firms face serious payment risks, including late payments, client bankruptcies, and rising material costs. Trade credit insurance helps protect against these risks by covering up to 90% of unpaid invoices and providing tools to assess client creditworthiness. Here’s why it’s important:

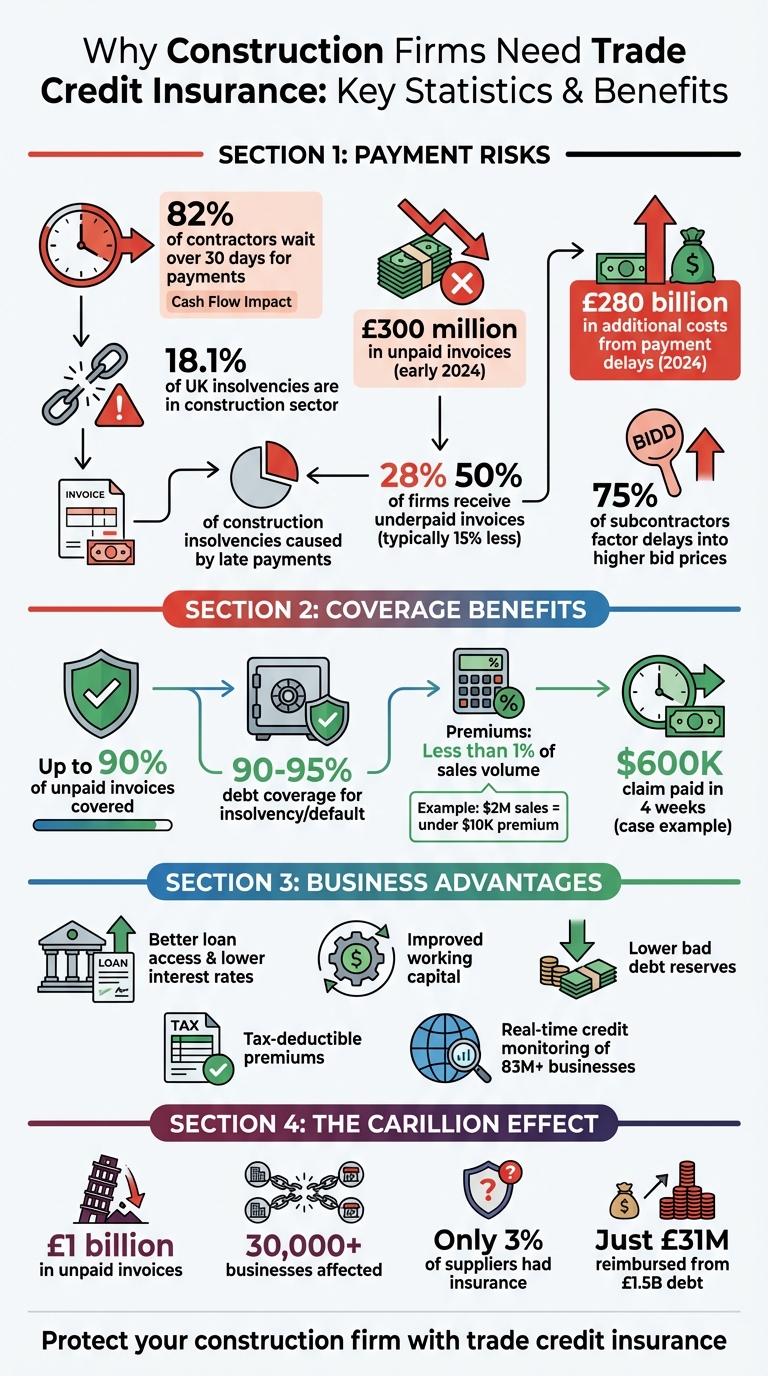

- Payment Delays: 82% of contractors wait over 30 days for payments, causing cash flow issues.

- Client Insolvencies: The construction sector accounts for 18.1% of UK insolvencies, with unpaid invoices reaching £300 million in early 2024.

- Economic Pressures: Inflation, high interest rates, and fixed-price contracts make financial stability harder to maintain.

Benefits of Trade Credit Insurance:

- Covers unpaid invoices due to client bankruptcy or default.

- Stabilizes cash flow, ensuring funds for payroll and materials.

- Improves access to loans and working capital by securing receivables.

- Provides real-time client credit data to avoid risky contracts.

Without it, a single major client default can create a domino effect, harming subcontractors and suppliers. Investing in trade credit insurance safeguards your business and keeps projects moving forward.

Construction Payment Risks and Trade Credit Insurance Benefits Statistics

Main Payment Risks Construction Firms Face

Client Bankruptcy and Non-Payment

When a client goes bankrupt, the financial shockwaves can be immediate and severe. A stark example is the January 2018 collapse of Carillion, the UK’s second-largest construction company at the time. This event left an estimated £1 billion in unpaid invoices, affecting over 30,000 businesses. The fallout didn’t stop there – taxpayers bore an additional £148 million burden, and the entire construction supply chain faced devastating cash flow disruptions. Unfortunately, this wasn’t an isolated case. In the year leading up to March 2024, the construction sector accounted for one in six business insolvencies, placing it at the top of the list for industry failures.

A major driver of these insolvencies is insufficient working capital. Many clients simply don’t have the funds to pay because they themselves are waiting on payments from others. This creates a "domino effect" where one non-payment can cascade through the supply chain. In fact, late payments alone were responsible for 28% of construction sector insolvencies in the UK during 2023.

The scale of unpaid invoices is staggering. By early 2024, this figure had reached £300 million, with projections suggesting it could climb to £1 billion by year’s end. Adding to the strain, half of construction firms reported receiving underpaid invoices – typically 15% less than the agreed amount – often due to disputes over work quality or incomplete documentation.

"The collapse of a single major contractor can trigger a ‘domino effect’ through the entire supply chain, leaving multiple smaller businesses with catastrophic bad debts."

– Compare Credit Insurance

These insolvency and payment issues naturally tie into broader cash flow challenges, as explored next.

Project Delays and Payment Timing Issues

Payment delays have become a widespread issue in the construction industry. Currently, 82% of contractors report waiting over 30 days for payment – nearly double the 49% figure reported just two years ago. These delays come with a hefty price tag: in 2024, they contributed to an estimated $280 billion in additional costs across the sector.

The financial impact goes beyond just waiting for funds. Inflation steadily eats away at the value of delayed payments, while rising material and labor costs only add to the burden. On top of that, firms often have to take out bridging loans to cover gaps, incurring extra interest costs, and miss out on opportunities to reinvest their capital elsewhere.

"If a client doesn’t pay their subcontractors on time each week, they will often walk off site and look for work elsewhere. It can then be very difficult to get that labour back, which in turn affects the ability for the client to deliver work on time."

– Mark Telford, Founder, Telfords Chartered Accountants

The consequences ripple throughout the industry. Subcontractors now consider payment reliability when bidding on projects, with 75% factoring in higher bid prices to account for potential delays. This not only affects current projects but also raises costs for future work.

But payment delays are just one piece of the puzzle. Broader economic challenges bring additional risks.

Economic Downturns and Market Changes

Economic instability poses a significant threat to construction firms. In the UK, there was a 70% year-on-year rise in firms experiencing critical financial distress. Fixed-price contracts exacerbate the problem, as they prevent companies from passing rising material and labor costs on to clients, leading to substantial losses during inflationary periods. High interest rates further tighten margins, delaying project starts and creating unpredictable payment schedules.

The situation isn’t limited to the UK. In Australia, construction insolvencies surged by 82% in the 2023 financial year compared to 2022. Meanwhile, claims paid and reserved on construction buyers reached £76.5 million in the year ending June 2023.

Market volatility also affects trade credit insurance. A survey of British Merchants Federation members revealed that 54% had their trade credit insurance limits reduced due to economic uncertainty. This often forces suppliers to demand earlier payments or halt sales altogether, adding more strain to cash flow.

"Investing in credit insurance is not merely a defensive measure; it is a strategic enabler that supports sustainable growth."

– Marsh

Post-pandemic challenges add another layer of complexity. Firms are grappling with government efforts to recover unpaid taxes and pandemic-related loans, which further stretch operational cash flow. Additionally, 88% of finance directors in the construction sector said growing their business in 2024/2025 was harder than the previous year. To secure projects, 98% of construction companies admitted to extending larger credit lines to clients than they were comfortable with.

These challenges highlight the growing importance of trade credit insurance in managing financial risks.

sbb-itb-2d170b0

How Trade Credit Insurance Protects Construction Companies

Coverage for Unpaid Invoices

Trade credit insurance can cover around 90% of unpaid invoices when a client faces insolvency or prolonged default. Policies can be adjusted to include various construction-specific costs like pre-manufacture expenses, on-site work, payment applications, day work, contract variations, and retention monies.

For example, the Association of British Insurers shared a case where a medium-sized construction company received a $600,000 claim payout within just four weeks after one of their major clients declared insolvency. This quick response not only offset the financial loss but also kept the company’s operations steady.

The collapse of Carillion in January 2018 is a stark reminder of what can happen without trade credit insurance. Only 3% of Carillion’s suppliers had this coverage, and out of the $1.5 billion in debt left behind, just $31 million was reimbursed through insurance payouts.

Maintaining Steady Cash Flow

One of the biggest advantages of trade credit insurance is how it stabilizes cash flow. When a major client fails to pay, the insurance ensures businesses can still cover essential costs like subcontractor payments, payroll, and material purchases for other projects. This kind of financial stability keeps projects moving forward and helps avoid a domino effect of cash flow problems.

Additionally, insured accounts receivable are viewed as more secure by banks and lenders, which can lead to better financing options and increased access to working capital. Plus, trade credit insurance premiums are typically tax-deductible, offering another financial benefit.

"Banks are more likely to lend more capital to businesses with trade credit insurance simply because it demonstrates an extra level of financial security."

– Neon Mavromatis, Kerry London Ltd

Beyond just covering immediate financial gaps, trade credit insurance also supports smarter, long-term decisions by providing detailed credit assessments.

Client Credit Information and Market Data

Trade credit insurance doesn’t just offer financial protection – it also provides critical market insights that construction firms can use to manage risks more effectively. Insurers supply real-time data and credit ratings, giving businesses a clearer picture of the financial health of both current and potential clients. This helps in making well-informed decisions before signing contracts. For instance, Allianz Trade monitors over 83 million businesses globally to deliver these insights.

Such data can help construction companies steer clear of high-risk projects. Insurers set credit limits for each buyer based on their financial standing, acting as a guide for managing exposure. Many insurers also offer online tools to instantly request credit limits, which can be invaluable when assessing new opportunities.

"Trade credit insurance… enhances credit decisions, facilitates stronger and quicker credit assessments, and enables ongoing customer monitoring to identify signs of financial distress."

– Marsh MMA

Providers like Accounts Receivable Insurance go a step further by offering comprehensive risk evaluations and access to a global network of credit insurers. These tools help firms navigate uncertain markets while keeping an eye on potential risks. The continuous monitoring also flags early signs of financial trouble, giving companies the chance to renegotiate terms or avoid risky clients altogether.

Considering that 4,111 construction companies in the UK went insolvent in the 12 months leading to March 2025 – and that the construction sector accounted for 18.1% of all UK insolvencies during that year – having access to this kind of market intelligence is more than just helpful; it’s a lifeline for staying ahead in a volatile industry.

Advantages of Trade Credit Insurance for Construction

Better Access to Loans and Credit

Having trade credit insurance in place secures your receivables, which can make banks more willing to offer favorable financial terms. This can mean lower interest rates, higher borrowing limits, and improved working capital. For construction firms, this policy can be a key bargaining tool during loan negotiations, helping unlock credit lines for upcoming projects. Interestingly, 98% of construction companies acknowledge extending larger credit lines than they’d like, all in the name of maintaining solid business relationships. With this financial backing, companies can confidently explore new opportunities without overextending themselves.

"Businesses with a credit insurance policy are often viewed more favourably by banks, unlocking better financing terms and improving access to working capital."

– Angus Nanan, Head of Construction, Kerry London

Confidence to Grow Your Business

With stronger financing options in place, trade credit insurance also supports business growth by reducing the risks of client non-payment. Policies typically cover 90–95% of invoices, allowing firms to offer competitive payment terms without jeopardizing their financial health. This is especially critical in construction, where 88% of finance directors report facing greater challenges in expanding their operations. By shifting the responsibility of credit risk assessment to the insurer, sales teams can focus on securing new contracts rather than vetting clients. This makes trade credit insurance a practical tool for safe and steady growth.

"Trade credit insurance allows you to take on additional work safely and securely, whether it’s a new customer or expansion from existing customers."

– David Edgell, Regional Commercial Manager, Allianz Trade

Lower Bad Debt Reserves

By transferring the risk of defaults to the insurer, companies can reduce or even eliminate the need for bad debt reserves. This freed-up capital can then be reinvested into operations, new equipment, or project development. Additionally, while reserves for bad debts aren’t tax-deductible, premiums for trade credit insurance often are. This creates a more efficient use of financial resources. Considering that 55% of businesses still deal with unpaid invoices from the previous tax year and nearly one in four SME managers report worsening late payment issues, redirecting this capital can be a game-changer for maintaining competitiveness.

"Trade credit insurance also means firms that keep a bad debt reserve can potentially reduce its size. The capital freed up can be used for a much more useful purpose – growth."

– Allianz Trade

How to Get Trade Credit Insurance for Your Construction Firm

Assess Your Payment Risks

Start by identifying the areas where your business is most exposed to payment risks. Dive into your historical financial records to spot patterns – are there customers who frequently pay late or require write-offs? Review your clients’ year-end financial statements, but don’t stop there. Request quarterly updates on their operating results to catch any decline in their creditworthiness early. As Gary Mendell, President of Meridian Finance Group, aptly put it, "90 days is the new net 30".

Expand your analysis beyond internal records. If your revenue depends heavily on a few major clients or specific regions, your risk increases if a single project fails. Use tools like credit bureau reports or industry creditor groups to uncover warning signs that might not surface in your direct dealings. Consider scheduling virtual site visits or video calls with key clients to discuss their financial health and upcoming projects. The goal is to distinguish between temporary payment delays and deeper financial instability.

Once you’ve pinpointed your risks, it’s time to find a policy that matches your business needs.

Select a Policy That Fits Your Needs

Trade credit insurance policies can be tailored to your operations, whether you need coverage for all accounts, just key clients, or single high-value partners. Premiums are typically less than 1% of your sales volume. For instance, a company with $2 million in annual sales would generally pay under $10,000 in premiums. Providers like Accounts Receivable Insurance offer policies customized to your project size, customer base, and whether your work is domestic or international. If you’re handling international projects, it’s wise to include political risk coverage.

Most policies protect against commercial risks like insolvency or prolonged payment defaults, often covering 90–95% of the debt owed. When applying, include a detailed cover memo explaining how factors like rising material costs or labor shortages are affecting your business. This helps underwriters better understand your risk profile and provide appropriate coverage.

After securing a policy, ongoing monitoring becomes crucial for effective claims management.

Monitor Accounts and Manage Claims

Once your policy is in place, your insurer will actively monitor the financial health of your customers. They use financial statements, public records, and data from other policyholders to assess risks. Each customer is assigned a specific credit limit, which can be adjusted in real time as their risk profile changes. This system works like an early warning mechanism, alerting you to potential issues before they escalate into significant losses.

You’ll need to notify your insurer about overdue invoices – typically when they’re more than 30 days past due or exceed the maximum invoicing period specified in your policy. Insurers often start with amicable recovery efforts or renegotiate payment terms. If the debt remains uncollectible due to insolvency or prolonged default, you can file a claim and receive reimbursement for the agreed percentage of the loss. With dedicated claims management support, Accounts Receivable Insurance helps ensure that your cash flow remains steady, even when a customer fails to pay.

Trade Credit Insurance: Safeguard Your Business in 2022

Conclusion: Protect Your Construction Firm’s Financial Health

Managing payment risks in construction isn’t just important – it’s essential. The construction industry consistently ranks among the top three sectors for business failures, making up 18.1% of all UK insolvencies in the 12 months ending March 2025. Non-payment risks are a constant challenge, but trade credit insurance offers a practical solution. By covering up to 90% of outstanding debts when clients default or go insolvent, it transforms uncertainty into a manageable risk.

Beyond protection, trade credit insurance strengthens your financial standing. Insured accounts receivable are seen as reliable collateral by banks, which can lead to improved financing terms and greater access to working capital. This added financial security allows you to confidently take on larger projects and explore new markets without the looming threat of devastating losses.

"Banks are more likely to lend more capital to businesses with trade credit insurance simply because it demonstrates an extra level of financial security."

– Neon Mavromatis, Kerry London Ltd

In construction, the failure of one major contractor can set off a chain reaction, impacting subcontractors and suppliers. This interconnected nature of the industry makes having financial safeguards even more critical.

Accounts Receivable Insurance understands these unique challenges. Their team specializes in creating tailored trade credit insurance solutions specifically designed for construction firms. They offer thorough risk assessments, dedicated claims support, and access to a global network of credit insurance providers. Coverage options extend to domestic and international projects, including work-in-progress, unbilled labor, materials, and retention monies.

Don’t wait for a payment crisis to threaten your business. Reach out to Accounts Receivable Insurance today at accountsreceivableinsurance.net to explore how a customized policy can protect your cash flow, strengthen your financial foundation, and support your growth ambitions.

FAQs

What doesn’t trade credit insurance cover on construction projects?

Trade credit insurance is specifically designed to protect against non-payment caused by financial instability or bankruptcy of a buyer. However, it does not cover losses stemming from unrelated issues. For example, problems like contractual disputes, product defects, or political risks that fall outside the policy’s scope are excluded. To address these kinds of risks, separate solutions or policies are usually needed.

How do insurers set and change credit limits for my customers?

Insurers set credit limits by closely examining a buyer’s financial standing, payment track record, the risks tied to their industry, and the amount of credit requested. Based on this evaluation, they may fully approve, partially approve, or deny the requested limits.

These credit limits aren’t static. Insurers regularly revisit and adjust them, keeping an eye on changes in the buyer’s financial health or shifts in market conditions. This ongoing process ensures your trade credit insurance remains in step with evolving risks.

How fast can I get paid after filing a claim for non-payment?

The time it takes to receive payment after filing a claim for non-payment can vary based on your policy and the details of your situation. Generally, claims are handled within 180 days from the invoice date. Once you’ve provided all the necessary documentation, payments are usually processed faster, helping to resolve the matter promptly.