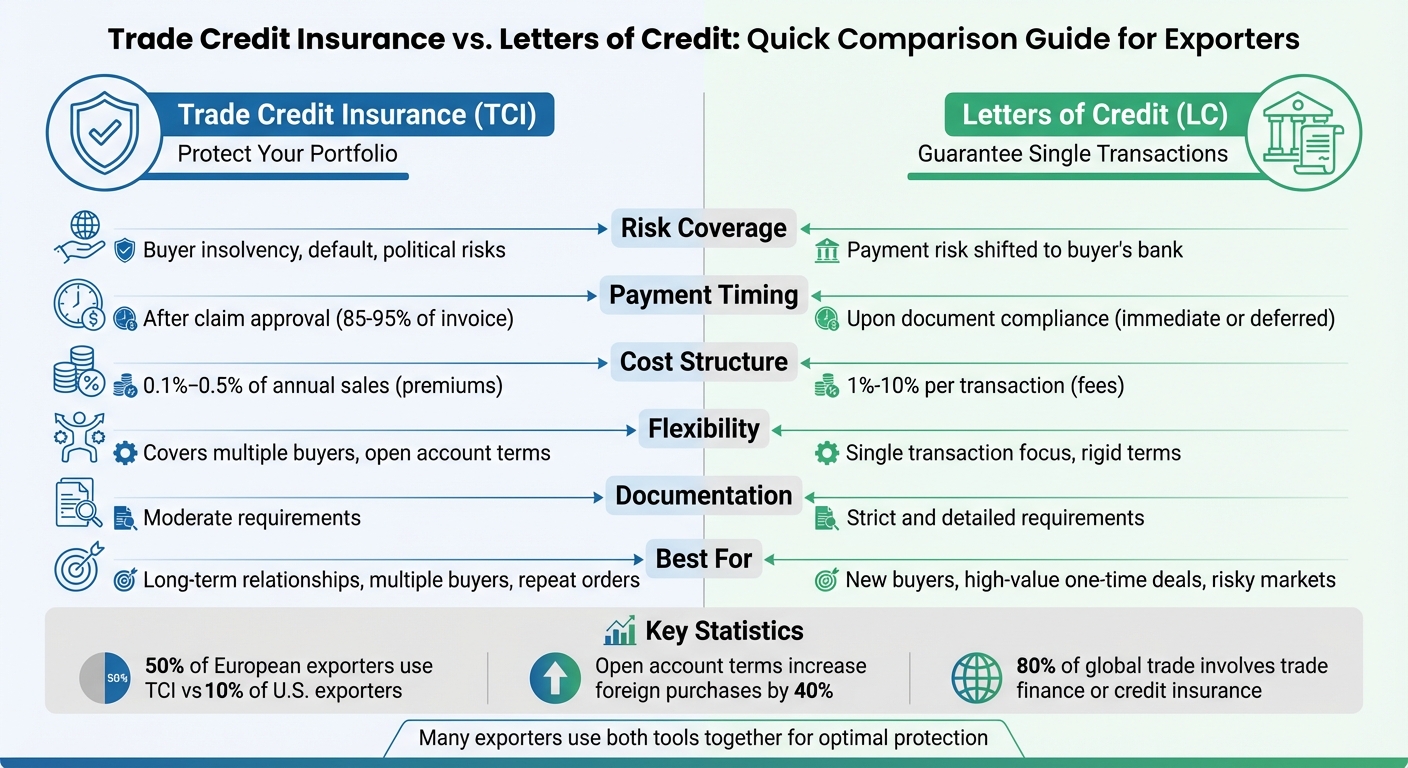

When selling internationally, ensuring you get paid is often a challenge. Two common tools can help: Trade Credit Insurance (TCI) and Letters of Credit (LCs). Here’s how they differ and when to use them:

- Trade Credit Insurance (TCI): Protects against buyer non-payment due to insolvency, default, or political risks. Covers 90-95% of invoice value and works well for managing multiple buyers or offering open account terms.

- Letters of Credit (LCs): Guarantees payment from the buyer’s bank once shipping documents meet requirements. Best for high-value, one-time deals or working with new buyers in risky markets.

Quick Comparison:

| Factor | Trade Credit Insurance | Letters of Credit |

|---|---|---|

| Risk Coverage | Buyer insolvency, default, political risks | Payment risk shifted to buyer’s bank |

| Payment Timing | After claim approval | Upon document compliance |

| Cost | Premiums (0.1%-0.5% of sales) | Transaction fees (1%-10%) |

| Flexibility | Covers multiple buyers | Single transaction focus |

| Documentation | Moderate requirements | Strict and detailed |

Use TCI for long-term relationships or diverse buyers. Choose LCs for new, high-risk, or large transactions. Combining both can provide security and flexibility for exporters.

Trade Credit Insurance vs Letters of Credit: Key Differences for Exporters

What is Trade Credit Insurance? | Credit Insurance explained in 5 minutes

sbb-itb-2d170b0

What is Trade Credit Insurance?

Trade Credit Insurance (TCI) is designed to safeguard your business from financial losses when customers fail to pay for goods or services. This could happen due to reasons like insolvency, bankruptcy, or prolonged delays in payment. Essentially, it acts as a safety net for your working capital, protecting it from the impact of unpaid debts.

But TCI doesn’t stop there. It also shields businesses from political risks, such as currency transfer restrictions, trade embargoes, government actions, or civil unrest. This makes it especially valuable for exporters dealing with markets in unstable regions. These protections form the foundation of TCI’s broader benefits, which can be tailored to specific business risks.

"TCI – sometimes referred to as accounts receivable insurance, debtor insurance, or export credit insurance – therefore helps businesses protect their capital and stabilize cash flows." – Investopedia

Key Features and Benefits

TCI goes beyond basic coverage, offering flexible options that can strengthen your financial position.

One of its standout features is its scalability. You can customize coverage to include either your entire customer base or focus on specific high-risk accounts, depending on your business needs and risk tolerance.

Another advantage is the credit enhancement benefit. Insured receivables are often considered high-quality collateral by banks, which can help businesses secure better financing terms or increase their credit limits.

When it comes to claims, TCI typically reimburses 85% to 95% of the invoice amount if a buyer defaults. This reimbursement range – commonly used by EXIM – helps keep premiums manageable while encouraging businesses to maintain sound credit practices.

Beyond providing protection, TCI can also act as a competitive tool. Offering open account terms backed by insurance allows businesses to attract more buyers. In fact, foreign buyers offered these terms tend to purchase about 40% more compared to those required to pay upfront.

How it Works

The process starts with insurers assessing the creditworthiness of your buyers and setting credit limits before any sales are made.

Premiums are calculated monthly, typically based on a percentage of either that month’s sales or total outstanding receivables. These premiums generally range from 0.1% to 0.5% of annual sales. For smaller exporters with less than $7.5 million in export sales, policies like EXIM’s Express Multi-Buyer insurance often come with added benefits, such as no issuance fees or first-loss deductibles.

If a buyer fails to pay, you can file a claim after the specified waiting period. The insurer will investigate and, if approved, reimburse the agreed-upon percentage of your loss. For example, during the 2008 financial crisis, trade credit insurance in the UK saw a 48% surge in claims during the first quarter of 2009, showcasing its importance during challenging times.

One important note: TCI typically excludes disputes over product quality or quantity until those issues are resolved. To ensure smooth coverage, businesses should maintain strong credit underwriting and collection processes, as these factors influence premium rates. This structured approach underscores TCI’s role in protecting your working capital effectively.

What is a Letter of Credit?

A Letter of Credit (LC) shifts the payment obligation from your foreign buyer to their bank, guaranteeing payment once you provide the necessary documents. This is particularly helpful when working with new customers or trading in regions where payment reliability might be uncertain. Unlike trade credit insurance, which insures against non-payment risk, an LC ensures payment through a bank’s commitment.

"A Letter of Credit is a contractual commitment by the foreign buyer’s bank to pay once the exporter ships the goods and presents the required documentation to the exporter’s bank as proof." – International Trade Administration

Under the Principle of Abstraction, the bank’s role is strictly tied to the documents presented, separate from the actual sales contract. While this separation offers protection, it also demands meticulous attention to detail in documentation.

Key Components and Types

Letters of Credit include several key players and come in various forms to suit different trade scenarios.

The main parties involved are:

- Applicant: The buyer who requests the LC from their bank.

- Beneficiary: The seller or exporter who will receive payment.

- Issuing Bank: The buyer’s bank that guarantees the payment.

- Advising Bank: Usually the exporter’s bank, which confirms the LC issuance.

For added security, especially when dealing with buyers in high-risk regions or banks with lower credit ratings, you might consider a Confirmed Letter of Credit. This involves your bank acting as a second guarantor. For instance, Citibank Global Trade Services offers confirmed LCs for transactions in economically unstable areas like Latin America, Africa, Eastern Europe, and Asia. The additional layer of protection typically comes with a fee of around 0.75% of the transaction amount.

LCs also differ based on payment timing and guarantees:

- At Sight: Payment is made immediately upon presenting the required documents.

- Deferred Payment: Payment is made at a later, agreed-upon date.

- Standby Letter of Credit: Acts more like a safety net, ensuring payment only if the buyer fails to meet their obligations.

According to the International Chamber of Commerce‘s UCP 600 rules, all LCs are considered irrevocable by default. This means changes or cancellations can only happen with the consent of all involved parties.

How it Works

The LC process ensures payment security, regardless of the buyer’s performance, by following a structured workflow.

First, you and your buyer agree to use an LC for the transaction. The buyer applies to their bank to issue the LC, which is then sent to your bank for review. It’s crucial to confirm the terms with your bank before moving forward.

Once you ship the goods, present the required documents to your bank for verification. Accuracy is critical – banks can reject payments for even minor errors in the paperwork.

"The bank’s obligation is defined by the terms of the LC alone, and the contract of sale is not considered." – Wikipedia

After your bank confirms the documents meet the LC terms, they forward them to the buyer’s bank. The buyer’s bank then releases payment to your bank, which deposits the funds into your account. At the same time, the buyer receives the documents needed to claim the goods.

To manage risk, banks often require buyers to provide collateral, ensuring they can recover funds if the buyer defaults. This collateral system adds another layer of security for all parties involved in international trade.

Key Differences Between Trade Credit Insurance and Letters of Credit

Trade Credit Insurance (TCI) and Letters of Credit (LCs) both serve to protect exporters from payment risks, but they operate in distinct ways. TCI acts as a safeguard by reimbursing a portion of losses if a buyer defaults. On the other hand, LCs shift the payment risk to the buyer’s bank, ensuring payment as long as specific document requirements are met.

Flexibility is a key distinction between the two. TCI provides more freedom, enabling exporters to build relationships through open account terms. In contrast, LCs rely on rigid, document-driven conditions.

"Sellers should know their clients better than anybody. If a company isn’t doing its due diligence, it may be purchasing more insurance than is otherwise needed, or its insurance may be more expensive than it should be." – Jason Benson, Global Head of Structured Working Capital in Trade & Working Capital, J.P. Morgan

Another major difference lies in the scope of coverage. TCI can protect an entire sales portfolio across multiple buyers, while LCs are typically designed to secure payment for individual transactions. This distinction became particularly apparent during the COVID-19 pandemic. Products heavily reliant on LCs experienced a much smaller decline in exports – 2.5 log points less – compared to those with minimal LC usage. Meanwhile, global trade flows saw a sharp year-over-year drop of 16% in April 2020 and 18% in May 2020.

Comparison Table

| Factor | Trade Credit Insurance | Letter of Credit |

|---|---|---|

| Payment Timing | After a loss occurs and claim is processed | Upon presentation of compliant documents (sight) or at a fixed future date (deferred) |

| Risk Coverage | Commercial risks (insolvency, default) and political risks | Non-payment risk of the buyer and the buyer’s bank |

| Cost Structure | Premiums based on sales volume or specific buyer risk | Transaction-based fees (issuing, advising, confirming) |

| Documentation | Requires credit management, reporting, and due diligence | Strict adherence to terms; discrepancies can delay payment |

| Flexibility | High; allows open account terms and relationship building | Low; involves rigid bank-controlled conditions |

| Coverage Scope | Can cover entire portfolios or specific transactions | Typically covers a single, specific transaction |

These differences highlight how exporters can choose between TCI and LCs based on their specific business needs and risk management strategies.

When to Use Trade Credit Insurance vs. Letters of Credit

Deciding between Trade Credit Insurance and Letters of Credit depends on factors like transaction size, your relationship with buyers, and how much risk you’re willing to take. Here’s a closer look at when each option makes sense.

When Trade Credit Insurance Shines

Trade Credit Insurance is ideal for businesses managing multiple buyers or looking to strengthen long-term relationships. If you’re working with established customers who place repeat orders, this tool allows you to offer open account terms. These terms can encourage customer loyalty and even boost order volumes by up to 40% – a clear way to support business growth.

Another major advantage is its ability to protect your entire portfolio. Instead of insuring individual transactions, you can safeguard your entire sales book, covering dozens or even hundreds of buyers. This is especially important for small businesses, where accounts receivable can make up 40% of total assets. By offering flexible payment terms, you can stay competitive in global markets. In fact, while only 10% of U.S. exporters use trade credit insurance, 50% of European exporters rely on it regularly.

"Trade credit insurance is more than just insurance; it’s a front-end risk management and credit enhancement tool in addition to being a sales tool." – Office of Small Business, EXIM Bank

When Letters of Credit Are the Better Choice

In certain situations, Letters of Credit (LCs) are the go-to option, especially when you need the highest level of payment security. They’re particularly useful for high-risk transactions, such as working with new buyers, entering unfamiliar markets, or dealing with buyers whose creditworthiness is uncertain. The bank guarantee provided by an LC eliminates much of the payment risk.

LCs are often the best choice for large, one-time deals. For instance, a significant order from a first-time customer may justify the added documentation requirements and bank fees. This tool is also critical when importing from economically unstable countries, as the bank’s backing ensures payment even if the buyer’s financial situation deteriorates.

"Letters of Credit are one of the most secure payment instruments available but can be labor-intensive and relatively expensive due to bank fees." – International Trade Administration

However, this level of security comes with costs. LC issuing fees typically range from 1% to 10% of the transaction value, with advising fees between 0.1% and 0.25%. In riskier scenarios, banks might even require collateral covering up to 100% of the transaction value.

Using Both Tools Together

For exporters dealing with diverse transactions, combining both tools can offer the perfect balance of security and flexibility. For instance, you might use an LC for a first large shipment to a new buyer, then switch to trade credit insurance–protected open account terms as the relationship develops. This approach lets you secure high-value deals while also protecting your broader portfolio.

Trade credit insurance also allows more flexible payment terms, extending up to 180 days, which can be a game-changer compared to the stricter terms often tied to LCs. With 80% of global trade involving some form of trade finance or credit insurance, having both options available ensures you’re ready to handle a variety of scenarios.

For businesses looking to customize their approach, Accounts Receivable Insurance provides tailored solutions, detailed risk analysis, and dedicated support to protect your receivables, whether you’re operating domestically or internationally.

Benefits, Costs, and Considerations for Exporters

Benefits and Drawbacks of Trade Credit Insurance

Trade credit insurance provides a safety net for exporters by covering multiple transactions at a cost of 0.5% to 1.5% of the invoice value. This coverage allows exporters to offer open account terms, which helps build trust with buyers. Another advantage is the ability to extend payment terms up to 180 days, making your offers more appealing in competitive international markets.

However, the process isn’t without challenges. Filing claims can be complicated, often requiring extensive documentation that may delay payouts. Additionally, these policies typically exclude certain risks, such as those associated with war or civil unrest, leaving exporters vulnerable in specific situations.

Benefits and Drawbacks of Letters of Credit

For exporters considering letters of credit (LCs), the main appeal lies in the certainty of payment. With the bank taking on the risk of non-payment, LCs are particularly suitable for high-value, one-time transactions with buyers you may not know well.

"The primary advantage of an LC is the assurance of payment… By doing this, the possibility of non-payment is reduced." – Saddam Hussain, Digital Marketing and Supply Chain Finance Expert at KredX

That said, this level of security comes with higher costs. Fees for LCs range from 1% to 10% of the transaction value, and additional advising fees may apply. The strict documentation requirements can also be a hurdle – minor errors in shipping documents could lead to payment refusals by the bank. If changes are needed, formal amendments add both time and expense. Furthermore, some banks may require buyers to post 100% collateral, potentially straining their cash flow.

Factors to Consider for Exporters

Choosing between these tools depends on several factors, including transaction frequency, buyer risk, and market conditions.

For exporters handling frequent shipments to the same buyer or managing a large, diverse customer base, trade credit insurance can be a cost-effective alternative to issuing multiple letters of credit. On the other hand, for one-time, high-value deals with new buyers, the payment security of an LC may outweigh its higher costs.

Buyer risk and market stability also play a key role. If you’re working in unfamiliar markets or with buyers whose creditworthiness is uncertain, LCs transfer the payment risk to the bank, offering peace of mind. However, for trusted buyers in stable markets, trade credit insurance provides better value while maintaining a strong relationship.

Exporters should also explore coverage options. For instance, EXIM Bank offers export credit insurance for transactions in over 175 countries, providing additional flexibility and assurance. Tailored solutions are available, allowing exporters to choose the best fit for both domestic and international operations.

Conclusion

Deciding between trade credit insurance and letters of credit isn’t about picking a one-size-fits-all solution – it’s about aligning the right tool with your specific business needs. Letters of credit offer unmatched payment security through bank guarantees, making them a solid choice for high-risk, one-time transactions with unfamiliar buyers. On the other hand, trade credit insurance provides flexibility and a competitive edge by allowing open account terms, which works particularly well for ongoing relationships with multiple buyers.

Earlier, we highlighted that 50% of European exporters rely on trade credit insurance, compared to only 10% in the U.S. It’s also worth noting that open account terms can increase foreign purchases by 40%. With global trade expected to reach $68.5 trillion by 2050, much of it driven by emerging markets with higher risks, U.S. exporters who effectively use these tools will be better positioned to thrive.

Ultimately, your choice should be guided by factors like transaction frequency, the nature of your buyer relationships, market conditions, and your tolerance for risk and cost. For stable markets and long-term partners, trade credit insurance often offers better value while fostering stronger business ties. Conversely, for high-value or high-risk transactions with new buyers, letters of credit shift the risk to banks, providing peace of mind.

For a well-rounded strategy, consider combining both tools to enhance your risk management approach. Specialists like Accounts Receivable Insurance can help you create tailored solutions that balance security, cost, and growth objectives, whether you’re focused on domestic or international markets.

FAQs

Which option is better for repeat orders: trade credit insurance or a letter of credit?

When dealing with repeat orders, trade credit insurance often stands out as the smarter option. It offers consistent protection against risks like non-payment, bankruptcy, and political instability. This makes it particularly useful for businesses managing credit risks across multiple transactions. Plus, it enables more flexible payment terms, which can help build stronger trust and smoother relationships in ongoing dealings.

On the other hand, a letter of credit – though highly secure – tends to work better for one-time transactions. Its higher costs and more complex procedures make it less practical for businesses handling frequent orders.

What documents most often cause a letter of credit payment to be rejected?

When it comes to letter of credit (L/C) payments, rejections often occur because of errors or inconsistencies in shipping and commercial documents. Some frequent problems include invoices with incorrect details, bills of lading that don’t match the terms, or certificates that fail to comply with the L/C requirements. To minimize the risk of rejection, it’s crucial to double-check that all documents are accurate and fully aligned with the terms outlined in the letter of credit.

Can I use a letter of credit and trade credit insurance on the same sale?

Yes, you can use both a letter of credit and trade credit insurance for the same transaction, as they fulfill distinct roles. A letter of credit ensures payment as long as specific conditions are met, acting as a safeguard during the transaction. On the other hand, trade credit insurance provides protection against risks such as non-payment or buyer insolvency. By combining these tools, businesses can achieve greater security by covering a broader range of potential risks – especially in international trade.