Trade credit insurance protects logistics companies from financial losses when customers fail to pay invoices. It’s especially useful for businesses operating on extended payment terms or dealing with high-risk clients. By covering most unpaid debts, this insurance ensures smoother cash flow, supports business growth, and provides security for both domestic and international transactions.

Key Takeaways:

- What It Covers: Non-payment due to insolvency, bankruptcy, or refusal to pay.

- Industry Risks: Extended payment cycles, customer concentration, seasonal fluctuations, and international challenges.

- Benefits: Improved cash flow, better financing options, and confidence to pursue larger contracts or new markets.

- Coverage Types: Domestic, international, political risk, and sector-specific options.

- Exclusions: Service disputes, intentional misconduct, and high-risk regions.

Trade credit insurance is a practical tool for logistics companies to manage risks, protect receivables, and maintain financial stability in a competitive market.

Managing Risks: How EDC helped MELLOHAWK Logistics protect international shipments

Key Benefits of Trade Credit Insurance for Logistics Companies

Understanding and managing risk is crucial for logistics companies navigating today’s competitive landscape. Trade credit insurance provides a safety net that can mean the difference between steady growth and financial setbacks. Here’s how it benefits logistics companies:

Improved Cash Flow and Risk Management

Trade credit insurance helps ensure smoother cash flow by protecting companies from the financial strain caused by unpaid invoices. If a customer defaults, this coverage helps maintain operations and ongoing investments without disruption. It also encourages logistics companies to adopt smarter credit and collection practices, fostering partnerships with trustworthy clients and creating a more stable financial foundation for growth.

Enabling Business Expansion

With trade credit insurance, logistics companies can confidently explore new opportunities. By reducing the risk of non-payment, businesses can extend credit to new and existing customers, fueling sales growth and market expansion. This added security is especially valuable when entering less familiar markets, as it helps mitigate concerns about customer payment reliability and broader economic uncertainties, opening doors to new customer bases and long-term growth.

Enhanced Financing Options

Having insured receivables can make a company more attractive to lenders. Since these receivables are considered less risky, businesses may secure better financing terms and easier access to working capital. This stronger financial position allows logistics companies to seize growth opportunities and invest in their operations with greater confidence, ensuring they can adapt and thrive in a competitive environment.

Coverage Options and Features for Logistics Companies

Trade credit insurance policies are specifically designed to address the unique challenges faced by logistics companies. By understanding the various options available, you can select the right protection to suit your business operations and financial exposure.

Types of Coverage

Domestic coverage safeguards against non-payment caused by insolvency or bankruptcy of customers within the United States. For logistics providers working across multiple states, this type of coverage helps mitigate risks associated with regional economic shifts that could impact several clients at once.

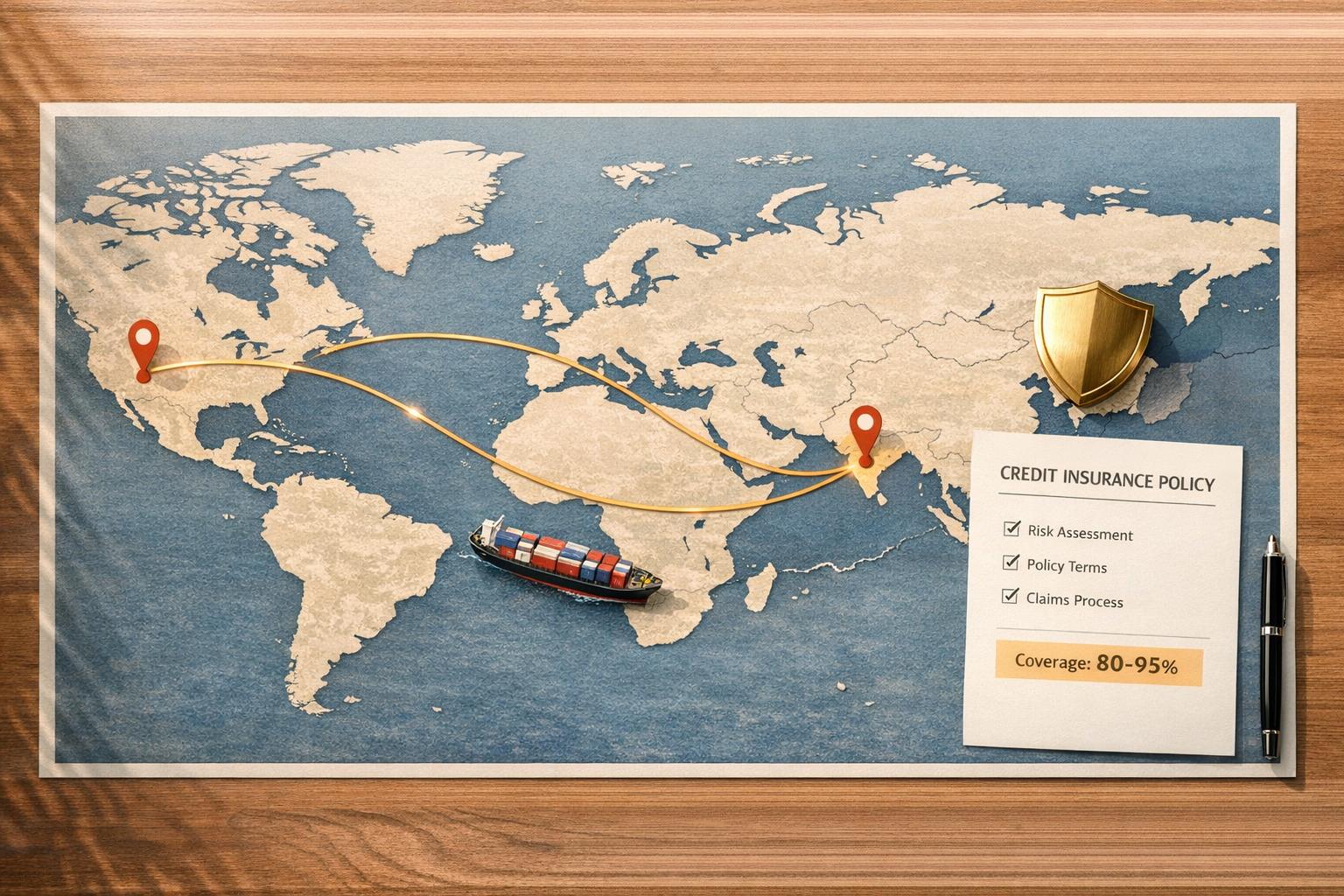

International coverage extends protection to cross-border operations, addressing both non-payment risks and political uncertainties. This policy is particularly valuable for logistics companies operating globally, as it covers customer insolvency and political disruptions – such as trade restrictions or sudden changes in government policies – that might prevent payment.

Political risk coverage focuses on risks tied to currency controls, government interventions, war, or civil unrest. This option is essential for logistics businesses operating in emerging markets or regions prone to political instability, providing protection where standard commercial insurance falls short.

Sector-specific additions allow companies to tailor their policies further. These might include coverage for extended payment terms, disputes arising from service agreements, or adjustments for seasonal fluctuations common in retail logistics.

These coverage types form the backbone of a comprehensive policy, offering protection against a wide array of financial risks.

Policy Features and Processes

Modern trade credit insurance policies are designed with features that streamline credit management and enhance operational efficiency.

Risk assessment tools help evaluate the creditworthiness of customers. Using global databases filled with financial records, payment histories, and credit ratings, these tools provide logistics companies with a clear picture of a customer’s reliability.

Account monitoring services add an extra layer of protection by continuously tracking the financial health of insured customers. Real-time alerts notify businesses of any changes in creditworthiness, enabling proactive decision-making.

Claims procedures require thorough documentation. If a customer fails to pay, logistics companies must show they’ve adhered to agreed-upon collection processes and fulfilled their contractual obligations. Typically, claims can only be filed after a waiting period of 90 to 180 days from the invoice due date.

Credit limit management allows for dynamic adjustments to customer credit limits. Insurers assess each customer’s financial stability and set specific coverage limits, which can be revised as relationships evolve or circumstances change.

Policy renewal and adjustment processes ensure that annual reviews keep policies aligned with a company’s shifting business needs and operational goals.

Exclusions and Limitations

While trade credit insurance provides valuable protection, it’s important to be aware of its exclusions and limitations.

Service-related disputes are generally not covered. For instance, if a customer refuses to pay due to damaged goods, delayed deliveries, or unmet service terms, the policy typically does not apply. Coverage is limited to cases where the customer acknowledges the debt but is unable or unwilling to pay for financial reasons.

Fraud and intentional misconduct by the policyholder void the policy. This includes knowingly extending credit to customers with poor financial stability without informing the insurer or failing to follow agreed collection procedures.

Coverage percentages usually range from 80% to 95% of the invoice value. This co-insurance arrangement means logistics companies still bear some risk, encouraging careful client selection and diligent payment collection.

Geographic limitations may exclude certain high-risk regions or countries under economic sanctions. Some policies may impose additional premiums for coverage in emerging markets or exclude specific areas altogether.

Payment term restrictions limit coverage to invoices with payment terms of up to 180 days. Logistics companies offering extended payment terms beyond this period might find such receivables excluded or subject to reduced protection.

sbb-itb-2d170b0

Steps to Get Trade Credit Insurance for Logistics

Securing trade credit insurance for your logistics company involves careful planning and a multi-step process. From the initial application to underwriting and ongoing management, each stage requires attention to detail and solid internal systems.

Application and Underwriting Process

The journey starts with gathering essential financial documents. Insurers typically ask for audited financial statements, including income statements, balance sheets, and cash flow reports. They also often need detailed customer credit data.

Customer concentration plays a big role in underwriting. If a large portion of your receivables comes from just a few customers, insurers may request additional documentation or adjust premiums to reflect the higher risk.

Underwriting also involves a close look at your credit management practices. Insurers examine how you evaluate new customers, set credit limits, and handle collections. Strong credit policies can lead to more favorable terms.

When calculating premiums, insurers consider factors like your annual turnover, customer mix, and claims history. Your overall risk profile will shape the pricing, and the timeline for underwriting may vary based on the complexity of your operations, particularly if you deal with international markets or high-risk clients. Once the policy is in place, it’s essential to align it with your credit management systems.

Combining Insurance with Credit Management

After securing coverage, integrating the policy with your credit practices strengthens your financial safeguards. For example, you can update your customer onboarding process to include insurer reviews, ensuring that internal credit limits match the coverage provided. If a customer requests a higher credit limit, both your internal team and the insurer typically need to approve the change.

Standardizing payment terms is another important step. Aligning your credit agreements with insurer requirements helps avoid potential coverage gaps. Additionally, training your accounts receivable team on the insurer’s documentation and reporting standards can help quickly identify and resolve issues.

Leveraging technology – such as customer relationship management (CRM) tools – can make the process smoother by tracking insured accounts and monitoring credit limits in real time. Once your systems are aligned, continuous monitoring becomes the key to maintaining protection.

Monitoring and Claims Management

Ongoing monitoring and efficient claims management are essential to safeguarding your business. Regular account reviews can spot potential problems early, and tracking customer payment behavior helps you catch signs of financial trouble before they escalate.

Proper documentation is critical when filing a claim. Keep records such as invoices, delivery confirmations, contracts, and any communication about payment issues. Claims should only be filed after you’ve made documented collection efforts.

When you do file a claim, you’ll need to provide evidence showing the debt exists, delivery was completed, and collection attempts were made. Straightforward claims are usually processed quickly, but more complex cases may take longer to resolve.

Even after filing a claim, recovery efforts often continue, with any recovered amounts shared between you and the insurer. Staying diligent with monitoring and documentation ensures that your business remains protected over the long term.

Accounts Receivable Insurance (ARI) Solutions for the Logistics Industry

Accounts Receivable Insurance (ARI) takes the principles of trade credit insurance and adapts them to meet the needs of logistics companies. Whether you’re a freight forwarder, third-party logistics provider, or transportation company, ARI understands the specific risks you face. Their solutions go beyond standard insurance offerings, addressing both domestic and international challenges unique to the logistics sector.

Custom Policies for Logistics Companies

Logistics operations often involve multi-party payment structures that can complicate transactions. ARI designs policies to cover these complexities, ensuring protection for scenarios where shippers, consignees, and intermediaries are all part of a single deal. Unlike generic trade credit insurance, their policies are crafted with these intricacies in mind.

For businesses operating on high volume but slim margins, ARI adjusts deductibles and coverage thresholds to make policies practical and effective. They also account for the global nature of logistics, offering protection against political risks and currency fluctuations – factors that can significantly impact receivables. This tailored approach ensures companies only pay for the coverage they truly need.

Key Services Offered by ARI

ARI provides a comprehensive suite of credit risk management services tailored to logistics companies. These include:

- Risk Assessment: ARI evaluates potential customers across multiple countries, helping logistics businesses make informed decisions about extending credit to new clients.

- Claims Management and Pre-Claim Support: Quick claims processing and proactive intervention help resolve disputes before they escalate, protecting cash flow.

- Global Network Access: ARI’s partnerships with credit insurance carriers worldwide allow logistics companies to secure coverage in high-risk markets or for specialized operations.

- Export Credit Insurance: For international logistics, ARI covers risks like political instability, currency inconvertibility, and sovereign default – essential protections for businesses operating in emerging or volatile regions.

Why Choose ARI for Trade Credit Insurance?

ARI understands the tight margins typical in the logistics industry and provides affordable, flexible policies that deliver meaningful protection without straining budgets. Their pricing structures are designed to align with the financial realities of logistics companies.

Flexibility is another hallmark of ARI’s approach. As businesses grow – whether by entering new markets, taking on larger clients, or diversifying services – ARI policies can adapt without requiring a complete overhaul. This adaptability ensures companies can scale confidently.

Beyond policy setup, ARI offers expert broker support to guide logistics companies through challenges like customer financial distress, international payment disputes, or changes in trade regulations. Their brokers are well-versed in the logistics industry and provide ongoing assistance to help businesses navigate complex situations.

With a strong understanding of both U.S. business practices and international trade requirements, ARI enables logistics companies to manage credit risk effectively while expanding their operations. Their combination of domestic expertise and global reach ensures businesses can thrive in an increasingly interconnected world.

Conclusion: Protecting Logistics Businesses with Trade Credit Insurance

Trade credit insurance plays a crucial role in safeguarding the financial health of logistics companies. According to the International Credit Insurance & Surety Association, over $7 trillion in shipments were insured by trade credit insurance in 2022, highlighting how indispensable this protection has become for mitigating payment risks.

For logistics businesses, a single customer default can cause significant disruption. Trade credit insurance transforms this uncertainty into a manageable risk, allowing companies to offer competitive credit terms while maintaining financial stability. This is especially critical when entering new markets or dealing with unfamiliar customers, where payment reliability may be uncertain.

By ensuring steady cash flow, trade credit insurance also unlocks working capital that can be directed toward growth-focused investments. This financial flexibility is often the key for companies looking to expand their operations or venture into international markets.

Industry experts stress the importance of personalized solutions for logistics companies.

"We can work with you to tailor an insurance policy to your needs", states ARI Global, underscoring the value of customized coverage.

Given the complexities of logistics operations – ranging from multi-party payment structures to international exposure – specialized insurance solutions are a necessity. Tailored policies can address unique challenges such as political risks, currency fluctuations, and intricate transaction chains, offering comprehensive protection.

Secured receivables also enhance lender confidence, leading to improved borrowing options and more favorable financing terms. For logistics companies, which often operate in capital-intensive environments, these benefits can be the difference between stagnation and growth.

The significance of trade credit protection in global commerce is evident in the numbers. In 2023, export credit agencies facilitated $191.5 billion in international deals, making global trade more secure and viable for businesses. This statistic underscores the growing reliance on credit protection tools across industries.

For logistics companies exploring trade credit insurance, it’s vital to partner with providers who understand the specific demands of their industry. The ability to customize policies, adapt to evolving business needs, and provide expert support during challenging situations – such as payment disputes or customer financial distress – can significantly impact the success of the partnership.

"We’ll also provide competitive quotes to find you the right custom policy for your business needs and budget", notes ARI Global, emphasizing the importance of accessible and flexible insurance options.

In today’s interconnected and rapidly growing logistics market, trade credit insurance is no longer optional – it’s a necessity. Businesses that prioritize the protection of their receivables are better positioned to maintain stable cash flow and seize new opportunities with confidence.

FAQs

How does trade credit insurance benefit logistics companies uniquely?

Trade credit insurance plays a crucial role for logistics companies by protecting their cash flow from risks like customer non-payment, insolvency, or default. Given the industry’s dependency on prompt payments for domestic and international shipments, this protection is indispensable.

It also helps logistics businesses navigate the financial unpredictability of global trade, including challenges like political instability or economic upheavals. By mitigating these risks, trade credit insurance enables logistics companies to confidently explore new markets and maintain financial stability in an ever-changing landscape.

How can logistics companies incorporate trade credit insurance into their credit management processes?

To make trade credit insurance a part of your credit management strategy, begin by assessing your customer accounts to pinpoint those with higher financial risk. This step helps you identify where protection is most needed. From there, collaborate with a credit insurance provider to design a policy that aligns with your business goals, covering both local and international transactions for comprehensive protection.

Take advantage of the digital tools offered by your insurer. These tools can make tasks like setting credit limits and tracking risks much easier, ensuring smoother day-to-day operations. Additionally, it’s important to regularly review your credit policies and insurance coverage. Doing so helps safeguard your business and supports steady cash flow over time.

What should logistics companies consider when choosing between domestic and international trade credit insurance?

When logistics companies are deciding between domestic and international trade credit insurance, there are several key factors to consider. Domestic policies often come with benefits like simpler claims processes, faster resolutions, and generally lower premiums. These advantages stem from reduced risks and protections provided by U.S.-specific regulations.

International coverage, however, introduces additional layers of complexity. Businesses must account for challenges such as political instability, currency fluctuations, and differences in legal systems across countries. These risks often necessitate more extensive policies, which can lead to higher premiums. For companies with global operations, it’s crucial to thoroughly assess their exposure to these uncertainties to ensure adequate protection. Meanwhile, those focused solely on U.S. markets can concentrate on safeguarding against domestic credit risks and potential insolvencies.