Trade credit insurance is essential for protecting your business from unpaid invoices, but premiums can quickly add up. The good news? There are practical ways to reduce these costs without compromising coverage. Here’s how you can save:

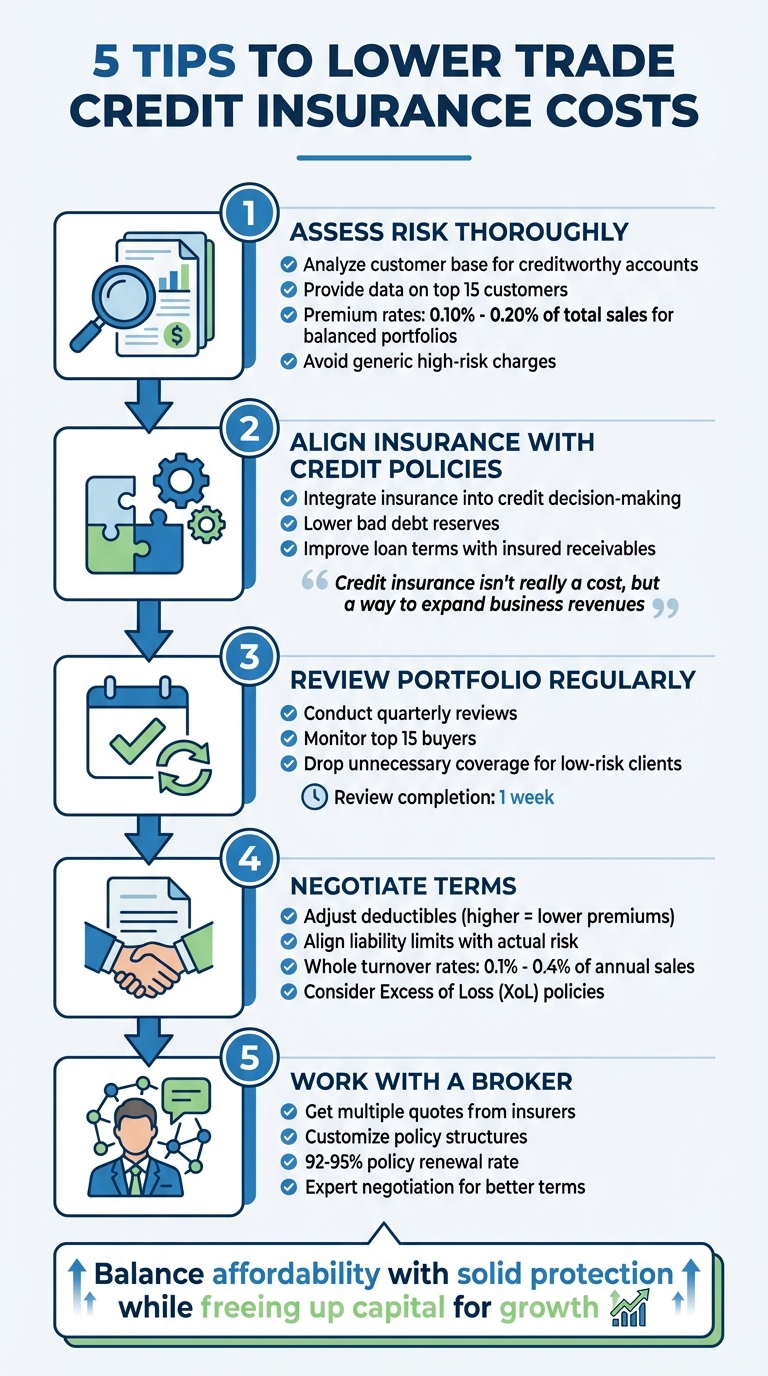

- Assess Risk Thoroughly: Analyze your customer base to highlight creditworthy accounts and avoid generic high-risk charges.

- Align Insurance with Credit Policies: Use insurance as part of your credit management process to show insurers you’re proactive.

- Review Your Portfolio Regularly: Drop unnecessary coverage and update policies to match your current needs.

- Negotiate Terms: Adjust deductibles, limits, and policy structures to better fit your risk exposure.

- Work with a Broker: Brokers can help customize policies, gather multiple quotes, and secure better deals.

These steps not only cut costs but also ensure your policy aligns with your business’s unique risks and goals. By staying proactive and informed, you can balance affordability with solid protection.

5 Strategies to Reduce Trade Credit Insurance Costs

1. Perform Complete Risk Assessments

Conducting a thorough risk assessment can lead to better premium rates. When you show underwriters that you’ve carefully evaluated your customer base, they’re less likely to pad your premium with generic high-risk buffers. As Atradius points out:

Knowing that you maintain a solid process in place will lower the risks of insuring your business, and in return will keep the premium lower.

This in-depth evaluation not only helps underwriters but also provides insights into management effectiveness, cost savings, and policy adjustments.

Risk Management Effectiveness

Start by gathering detailed data on your top 15 customers. Include their average sales volumes, credit needs, and up-to-date aging reports to highlight the health of your receivables. This transparency allows underwriters to assess your actual risks instead of applying broad assumptions. If you’re involved in exporting, be specific about the countries you trade with rather than using general regional labels – this can help avoid unnecessary charges for areas that don’t align with your operations.

Cost Reduction Potential

A detailed risk assessment can result in significant premium savings. Businesses with balanced risk profiles and strong internal controls often pay rates between 0.10% and 0.20% of total sales. Kirk Elken, Co-founder of Securitas Global Risk Solutions, highlights this dynamic:

A spread of risk can reduce the premium rate, while insuring only high-risk accounts can increase costs.

If your portfolio is concentrated in just a few buyers or includes financially unstable accounts, premiums are likely to rise. Diversifying your customer base and showcasing strong creditworthiness across your portfolio can help lower these costs.

Policy Optimization

Your risk assessment should also address how much loss your business can handle out-of-pocket. Opting for higher deductibles is a straightforward way to reduce premiums. By managing smaller losses internally, you lower the insurer’s potential exposure. Additionally, keeping a clean loss history or documenting isolated incidents can prevent premium increases at renewal. Lastly, providing evidence of your internal credit checks and collection processes demonstrates a strong safety net, signaling reduced risk to underwriters.

sbb-itb-2d170b0

2. Integrate Insurance into Your Credit Policy

Incorporating trade credit insurance into your credit management strategy can do more than just protect your business – it can actually help lower premiums by demonstrating proactive risk management. Instead of viewing insurance as a backup plan after deals are finalized, use it as a key part of your initial credit assessment process. This approach strengthens your risk controls and can lead to cost savings.

Risk Management Effectiveness

When insurance becomes part of your credit decision-making, it creates a more standardized and reliable approval process. For example, if an insurer declines coverage or limits exposure for a particular buyer, it’s a clear signal to reevaluate your internal credit terms. Aligning your policy with the insurer’s risk appetite not only helps you set consistent credit limits but also minimizes the chance of making decisions based on personal relationships, which can sometimes result in costly defaults. Keeping an eye on downgraded ratings or reduced limits also allows you to adjust your exposure before issues arise.

Cost Reduction Potential

Using trade credit insurance can lower the bad debt reserves on your balance sheet, which frees up capital to invest in growth or other operational needs. Additionally, insured receivables are often considered more secure by lenders, potentially leading to better loan terms or higher credit limits. As David Patten, CEO & CFO of Everchem LLC, explains:

Securitas and credit insurance have allowed us to focus on expanding our business with confidence. They helped Everchem realize that credit insurance isn’t really a cost, but a way to expand business revenues while reducing risk.

By leveraging these financial advantages, you can further fine-tune your coverage to align with your actual risk profile.

Policy Optimization

A tailored approach to credit insurance can help you select the best policy structure for your needs. For instance, instead of insuring your entire turnover, you might opt for named buyer coverage, focusing on high-value accounts that carry the most risk. You can also choose between cancelable and non-cancelable limits. Non-cancelable limits provide greater certainty, while cancelable ones may offer more flexibility in pricing. This allows you to balance cost and coverage effectively.

Ease of Implementation

To make integration seamless, start by documenting your existing credit safety procedures, such as credit scoring, collection processes, and aging report reviews. Sharing this information with underwriters during the application process can reduce the insurer’s perceived risk, which may lead to lower premiums right away. Additionally, using insurer-approved credit limits as a benchmark can simplify your processes and reduce administrative burdens. And don’t forget – trade credit insurance premiums may be tax-deductible, further lowering the overall cost of implementation.

3. Review and Update Your Insured Portfolio Regularly

Your insurance needs aren’t static – they shift as customer dynamics and market conditions change. Yet, many businesses treat their trade credit insurance policy as if it’s set in stone. Conducting regular portfolio reviews, preferably every quarter, can help you spot opportunities to save money and ensure you’re not paying for coverage you no longer need. These reviews also help you identify early warning signs, enabling you to make timely, strategic adjustments.

Risk Management Effectiveness

Take a close look at your top 15 buyers to identify changes in their risk profiles and update your coverage as necessary. Keep an eye out for insurer signals like downgraded buyer ratings or reduced credit limits – these are red flags that demand immediate attention. By acting quickly, you can reduce exposure, renegotiate payment terms, or even move to prepayment arrangements before a default occurs. Jason Benson, Global Head of Structured Working Capital in Trade & Working Capital at J.P. Morgan, emphasizes this point:

Sellers should know their clients better than anybody. If a company isn’t doing its due diligence, it may be purchasing more insurance than is otherwise needed, or its insurance may be more expensive than it should be.

Cost Reduction Potential

Portfolio reviews can also help you identify "dead weight" – low-risk, legacy clients who no longer bring in significant revenue. Dropping coverage for these accounts can free up premium dollars, which you can then allocate to higher-risk, high-growth customers. Additionally, maintaining a diverse portfolio with a broad spread of risk often leads to lower premiums. On the other hand, focusing solely on high-risk accounts tends to drive costs higher. Accurate sales forecasts are essential here, as they ensure you’re only paying for the risk levels that currently exist.

Policy Optimization

Regular reviews also highlight inefficiencies in your policy, allowing you to make adjustments that better reflect your current needs. For instance, you might switch from whole turnover coverage to named buyer coverage for high-value accounts, which can help lower costs. Keeping your insurer in the loop about your internal credit checks and aging reports shows that you’re actively managing risk, which can help keep premiums competitive.

Ease of Implementation

The good news? Most insurers can complete a full review of your buyer portfolio in as little as a week. Use digital dashboards and automated alerts to monitor changes in client solvency in real time. This lets you make immediate adjustments before small issues grow into major problems. By staying proactive, you’ll ensure your policy keeps pace with your business’s evolving needs.

4. Negotiate Coverage Limits and Policy Terms

Once you’ve completed a thorough risk assessment and updated your portfolio, the next step is negotiating your policy terms to trim premium costs. By focusing on specific adjustments, you can often secure better terms without sacrificing essential coverage.

Most insurers are open to discussions, making it possible to tweak your policy in ways that reduce costs while maintaining the protection you need. This step not only saves money but also strengthens your overall risk management approach.

Cost Reduction Potential

One effective way to lower premiums is by increasing deductibles. A higher deductible means the insurer has less financial exposure, which translates to a lower premium. As PIB Insurance explains:

A higher deductible generally leads to a lower premium, as the insurer’s potential payout decreases.

If your business has the financial strength to handle smaller losses, this strategy could significantly cut your annual premium expenses.

Another area to explore is the limit of liability – the maximum amount your insurer will pay during a policy period. If your current limit far exceeds your actual risk exposure, you’re likely paying for coverage you don’t need. Adjusting this limit to align with realistic expectations can lead to noticeable savings.

Policy Optimization

Beyond adjusting limits and deductibles, the structure of your policy plays a key role in managing costs. For example, whole turnover policies, which cover all receivables, often have lower rates (ranging from 0.1% to 0.4% of annual sales) because the risk is distributed across your accounts. In contrast, named buyer policies, which focus on specific high-risk or high-value accounts, typically come with higher rates.

For businesses with strong internal credit management, Excess of Loss (XoL) policies can be a cost-effective option. These policies cover only catastrophic losses above a predetermined threshold, allowing you to handle routine risks internally while keeping premiums lower. Additionally, negotiating non-cancellable limits – which guarantee coverage for the policy year even if a buyer’s credit risk worsens – can provide stability in uncertain markets.

Ease of Implementation

Negotiating policy terms doesn’t have to be complicated. Building on your portfolio reviews, you can refine your coverage by working with specialized trade credit brokers. These experts help balance higher deductibles with tailored liability limits, ensuring your policy aligns with your specific needs.

For multinational businesses, negotiating a Master Agreement can simplify global risk pooling and secure better terms across all subsidiaries. Many insurers also allow adjustments during annual renewals, making it easy to implement changes without a complete policy rewrite.

If you need assistance, the team at Accounts Receivable Insurance is available to help you customize coverage limits and fine-tune policy terms. They can ensure your trade credit insurance remains cost-effective while addressing the unique risks your business faces.

5. Work with a Broker for Customized Policies

Managing trade credit insurance can feel overwhelming, especially when you’re juggling coverage needs and budget limitations. This is where a specialized broker steps in. With their market knowledge and negotiation expertise, brokers help fine-tune policies to fit your specific requirements. By combining strategies like risk assessments and policy adjustments with expert negotiation, brokers can help you secure better coverage while keeping costs in check.

Cost Reduction Potential

One of the biggest advantages of working with a broker is their ability to lower costs by gathering multiple quotes from various insurers. As Kirk Elken, Co-founder of Securitas Global Risk Solutions, puts it:

The best way to determine credit insurance cost is to obtain multiple quotes. Through the quotation process, businesses gain a better understanding of how credit insurers view their risk.

This process not only highlights how different underwriters assess and price your buyer portfolio but also helps you identify the right deductibles. Opting for higher self-insured retentions often leads to reduced premiums. It’s worth noting that between 92% and 95% of trade credit insurance policyholders renew their policies annually, which reflects the consistent value this coverage provides.

Policy Optimization

Brokers don’t just save you money – they also help design policies tailored to your business’s unique risk profile and budget. They can guide you in choosing the most suitable type of coverage, whether it’s a whole turnover policy, a named buyer policy, or single buyer coverage. Additionally, brokers can negotiate for non-cancelable limits, which provide more consistent protection compared to standard policies where coverage might be withdrawn if a buyer’s creditworthiness declines.

David Patten, CEO & CFO of Everchem LLC, shares how this approach benefited his business:

Securitas and credit insurance have allowed us to focus on expanding our business with confidence. They helped Everchem realize that credit insurance isn’t really a cost, but a way to expand business revenues while reducing risk.

Ease of Implementation

Beyond savings and tailored solutions, brokers simplify the entire implementation process. They handle the complexities of managing insurer relationships and make policy terms easier to understand. For example, the team at Accounts Receivable Insurance specializes in crafting policies and negotiating terms that align with your business goals. This ensures you get the protection you need without unnecessary administrative headaches or extra costs.

Conclusion

Cutting trade credit insurance costs doesn’t have to mean sacrificing protection. The strategies shared here – conducting detailed risk assessments, aligning insurance with credit policies, routinely reviewing your portfolio, and negotiating terms with skilled brokers – offer a way to strike a balance between affordability and strong coverage. By implementing these steps, you can reduce premiums while maintaining, or even improving, the quality of your protection.

The benefits extend well beyond lower premiums. Keeping a portfolio of reliable, creditworthy customers and setting an appropriate deductible can reduce upfront expenses and release funds that would otherwise be locked in bad debt reserves. This extra capital can then be redirected toward growth initiatives. Plus, lenders often view insured receivables as safer collateral, potentially leading to better borrowing terms and expanded access to working capital.

With 92% to 95% of businesses renewing their policies each year, it’s evident that companies see trade credit insurance as more than just a safety net. These investments often pay off through increased sales potential and the confidence to take on growth opportunities that might otherwise feel too uncertain.

Trade credit insurance evolves alongside your business. As your customer base and market conditions shift, regular reviews ensure your policy stays aligned with your current risks, rather than relying on outdated assumptions. This proactive approach helps businesses stay ahead – treating insurance not as a mere expense, but as a tool for strategic growth.

FAQs

What information do insurers need to price my risk accurately?

To determine your premiums and assess your risk, insurers typically need specific details about your business. These include factors like your sales volume, the creditworthiness of your customers, the type of industry you’re in, your geographic location, your loss history, and the risk profile of your accounts. Supplying accurate and thorough information ensures they can evaluate your situation properly and offer premiums that reflect your actual risk.

Should I choose whole-turnover or named-buyer coverage?

When deciding, it all comes down to your customer base and how much risk you’re comfortable taking on. Whole-turnover coverage offers protection for your entire customer portfolio. This approach spreads the risk across multiple buyers, which usually means lower premiums. On the other hand, named-buyer coverage zeroes in on a single customer. It’s a good option if your business depends heavily on a few key clients, but it comes with higher premiums because the risk is more concentrated. Think about how diversified your customer base is and how much risk you’re willing to handle before making your choice.

How often should I review and adjust my policy to cut costs?

Regularly reviewing your trade credit insurance policy is a smart move to ensure it keeps up with your business’s evolving risks and market conditions. By conducting periodic assessments, you can fine-tune your coverage to better reflect your needs. This might mean negotiating more favorable premiums, adjusting coverage limits, or addressing shifts in customer creditworthiness or industry-specific risks. Taking this proactive step not only helps you stay prepared but could also lead to cost savings while keeping your coverage effective.