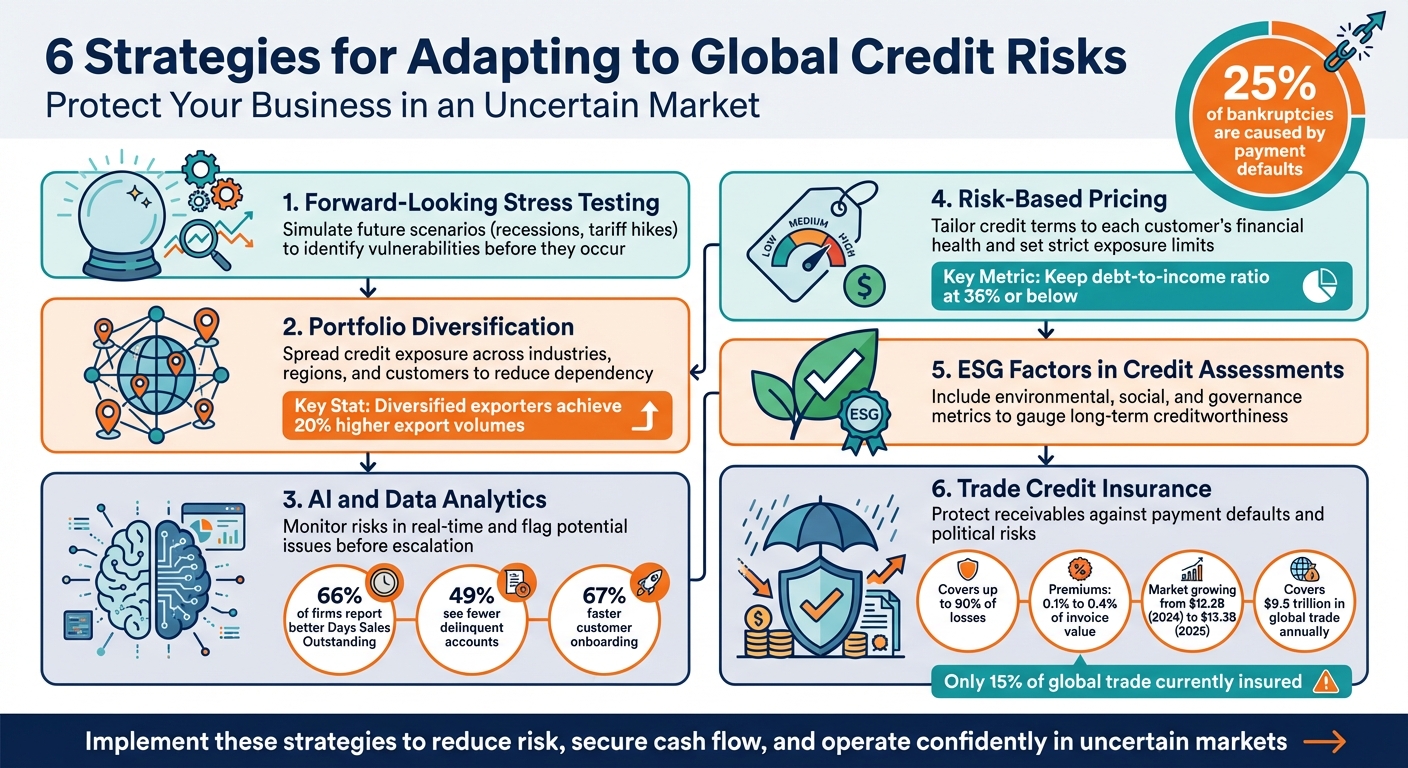

Businesses are facing unprecedented credit risks, with global bankruptcies at their highest levels in over a decade. To stay ahead, companies must rethink how they manage credit exposure and protect their financial health. Here’s a quick summary of six practical strategies to safeguard your business against global credit risks:

- Forward-Looking Stress Testing: Simulate future scenarios like recessions or tariff hikes to identify vulnerabilities.

- Portfolio Diversification: Spread credit exposure across industries, regions, and customers to reduce dependency on any single source.

- AI and Data Analytics: Use AI tools to monitor risks in real time and flag potential issues before they escalate.

- Risk-Based Pricing: Tailor credit terms to each customer’s financial health and set strict exposure limits.

- ESG Factors in Credit Assessments: Include environmental, social, and governance metrics to better gauge long-term creditworthiness.

- Trade Credit Insurance: Protect receivables – the largest uninsured asset for many businesses – against payment defaults and political risks.

With defaults accounting for 25% of bankruptcies, these strategies can help you reduce risk, secure cash flow, and operate confidently in uncertain markets.

6 Strategies for Adapting to Global Credit Risks

1. Use Forward-Looking Stress Testing

Risk Management Planning

Traditional credit models often struggle to keep up with today’s fast-changing market dynamics. As Marsh points out, these models "often don’t capture the rapid market shifts caused by evolving trade policies", leaving businesses vulnerable to unexpected risks. This is where forward-looking stress testing comes in. It helps assess how your credit portfolio might hold up under extreme but plausible future scenarios – think of events like a deep recession, a sudden increase in tariffs, or the bankruptcy of a major client.

This approach encourages asking critical "what if" questions. For example, what happens if interest rates surge overnight? Or if an entire industry tied to your largest customer faces collapse? By running these simulations, you can shift from merely reacting to crises to proactively identifying vulnerabilities. This way, you can uncover weak spots in your portfolio and ensure you have enough capital reserves to handle potential disruptions.

Technology Integration

Stress testing has evolved with the help of modern tools like AI and real-time simulators. These technologies allow businesses to incorporate forward-looking indicators into complex scenarios. For instance, they can simulate how a sudden spike in interest rates might trigger higher unemployment, which in turn could lead to increased customer defaults. By analyzing multiple risk factors together, rather than in isolation, these tools provide a more realistic and comprehensive view of potential threats. The insights generated enable businesses to move quickly from analysis to implementing effective risk management strategies.

Credit Risk Reduction

The results of stress tests can guide targeted actions to reduce credit risk. For example, you might adjust credit limits in high-risk sectors, diversify your portfolio to avoid over-concentration, or work with customers facing temporary financial challenges by offering flexible payment terms. It’s worth noting that trade credit insurance plays a significant role here, covering around $9.5 trillion in global trade transactions annually. These measures not only protect your business but also strengthen its ability to adapt to future challenges.

sbb-itb-2d170b0

Global Credit Risk Outlook

2. Diversify Your Portfolio Exposures

Expanding on proactive risk assessments, spreading your portfolio exposure can help shield your business from isolated disruptions.

Risk Management Planning

Relying too heavily on just a few customers can leave your business vulnerable. When a significant portion of your revenue comes from one or two buyers, a single missed payment could cause serious financial strain. Mike Seff, Senior Vice President of Specialty Lines at Intact Insurance Specialty Solutions, emphasizes this point:

"You are especially vulnerable if one or two buyers represent most of your receivables. Consider adjusting terms or seeking out new markets to reduce dependency".

Start by evaluating your current exposure. Are your receivables concentrated in a particular region or industry? Look for early warning signals like currency fluctuations, sanctions, or commodity price shifts that could impact specific markets. Combining a global perspective with local market insights can help you better understand the risks tied to various regions.

Portfolio Diversification

Spreading credit exposure across different markets, industries, and customer segments can act as a buffer against localized disruptions. For instance, in Canada, exporters selling to at least 10 markets account for 51% of the country’s total export value, despite making up only 6% of all exporters. These diversified exporters often achieve 20% higher export volumes compared to those focused on a single market.

Geographic diversification can help protect against risks like currency restrictions, tariff increases, or political instability. Similarly, spreading exposure across industries can stabilize cash flow during sector-specific downturns . Trade credit insurance portfolios, often less tied to broader economic shocks, can also provide financial stability through different economic cycles. By diversifying, your business becomes more resilient to disruptions, strengthening your overall risk management approach.

Credit Risk Reduction

A well-diversified portfolio of receivables not only reduces risk but can also improve your borrowing capacity. Lenders are more likely to offer favorable terms to businesses with varied receivables, as they are seen as less risky. Diversifying suppliers across multiple regions – whether through nearshoring or friend-shoring – can also minimize supply chain disruptions caused by geopolitical or environmental events .

It’s equally important to avoid relying solely on past payment histories when assessing customers. Request updated financial statements regularly and perform periodic health checks, especially for buyers in unpredictable industries. If customer concentration remains an issue, trade credit insurance master agreements can help by pooling global risks and securing better terms.

3. Use Data Analytics and AI for Credit Decisions

Technology Integration

Incorporating AI into credit decisions takes risk management to the next level by identifying potential issues in real time. Traditional credit assessments often fall short in spotting early warning signs, but AI can continuously monitor transactions and trade activities, flagging anomalies like unusual invoice patterns or delivery delays as they happen.

Switching from static to dynamic risk models changes the game. AI tools can sift through unstructured data – such as news reports on layoffs or investigations – far more efficiently than manual processes. For example, platforms like StratiFi consolidate different risk indicators into one dashboard, while tools like Marsh’s Sentrisk provide deeper insights into supply chain vulnerabilities.

Credit Risk Reduction

AI doesn’t just refine traditional credit assessments; it enhances them by combining financial data with behavioral patterns. Machine learning algorithms analyze factors like payment timing, transaction volume shifts, and regional economic pressures, comparing them against vast datasets . This approach can flag potential defaults – whether due to cash flow problems or looming insolvency – long before they escalate. The results speak for themselves: 66% of firms using accounts receivable automation reported better Days Sales Outstanding, and 49% saw fewer delinquent accounts. AI can also speed up customer onboarding by as much as 67%.

Carl Torrence, Content Marketer at Marketing Digest, puts it well:

"The goal is not automation for its own sake, but constant visibility. Leaders can see where exposure is building and address it before a problem turns into a loss".

Risk Management Planning

Start with core transactions and reliable data, then expand AI applications gradually. Assigning clear roles ensures that AI alerts lead to immediate action. Scenario analysis during market expansion is another powerful tool, allowing businesses to simulate the effects of factors like currency fluctuations, tariff adjustments, or supplier instability. While AI speeds up decision-making and provides data-driven insights, it doesn’t replace human judgment. Instead, it equips your team to respond more effectively to evolving market conditions. By integrating AI strategically, companies can adopt a more proactive approach to credit risk, enhancing their overall risk management efforts.

4. Apply Risk-Based Pricing and Exposure Limits

Risk Management Planning

To effectively manage risk, customize credit terms based on each client’s financial situation. Key factors to evaluate include liquidity ratios, debt-to-equity levels, payment history, credit scores, and any external risks related to their industry or location. For instance, the Consumer Financial Protection Bureau suggests keeping the debt-to-income ratio at 36% or below to maintain healthy borrowing capacity.

Regularly reviewing accounts receivable – on a monthly or quarterly basis – ensures your risk assessments stay up-to-date. If a client’s financial condition starts to decline, act swiftly by tightening payment terms and following up on overdue payments earlier. Taking these steps early can prevent small problems from turning into major financial setbacks.

Credit Risk Reduction

In addition to tailored pricing, setting strict exposure limits can safeguard your cash flow by minimizing concentration risk. Exposure limits help avoid over-reliance on a single client or group. If a key client defaults, the financial impact on your business could be severe. Consistent credit policies provide a structured approach to decision-making and help mitigate financial risks.

Leveraging data-driven scoring models that use real-time agency data allows you to classify customers by their risk levels. High-risk accounts can then be monitored more closely and assigned stricter limits. Standardized approval workflows further prevent unauthorized credit extensions, while automated alerts notify you of critical changes in a customer’s profile – such as mergers, bankruptcies, or other warning signs.

Technology Integration

Automated credit management tools integrate seamlessly with ERP systems to adjust exposure limits based on real-time customer behavior. This eliminates guesswork and speeds up decision-making. Stress testing provides an additional layer of insight, helping to identify vulnerabilities before they become serious issues. By combining flexible scoring models with ongoing monitoring, you can strike a balance between pursuing growth opportunities and managing potential risks. These strategies strengthen your business’s ability to navigate an unpredictable global market.

5. Include ESG Factors in Credit Assessments

ESG Alignment

Incorporating ESG factors into credit risk assessments is no longer optional – it’s a necessity. Conducting materiality assessments at the global, sector, and borrower levels helps identify what matters most in different contexts. Scoring methodologies are particularly useful for comparing a borrower’s ESG performance against industry peers, ensuring that sector-specific nuances are taken into account. For instance, energy-efficiency ratings may carry more weight for real estate portfolios, whereas a manufacturing firm’s carbon footprint could be a critical metric. Collaborative ESG action plans between lenders and borrowers can provide a framework for ongoing monitoring and improvement throughout the business cycle. By embedding these assessments into risk models, you can make more informed and confident funding decisions.

Risk Management Planning

ESG factors should be integrated directly into Probability of Default (PD) and Loss Given Default (LGD) models, making them a core part of funding decisions. Rather than treating ESG as an afterthought, this approach positions it as a key driver of creditworthiness . ESG metrics can act as early warning signals for credit rating changes, offering insights into a borrower’s future financial health before traditional metrics catch up. Effective risk management also requires considering "double materiality." This means evaluating both the company’s societal impact (inside-out risk) and how ESG risks could affect the company financially (outside-in risk). By doing so, you can build a credit portfolio that’s more resilient to global challenges. As M Indira Priyadarsini, Head of Solution and Delivery for Sustainable Banking and Finance at TCS, explains:

"Improved ESG performance across the financial ecosystem would deliver more authenticated ESG commitments rather than insubstantial ESG targets that lack substance and leads to greenwashing".

Technology Integration

Advancements in technology, particularly machine learning, are transforming how ESG factors are integrated into credit models. These tools can analyze media reports and alternative data in real time, generating dynamic ESG ratings. This capability allows credit models to identify emerging risks that may not be evident in historical data. By leveraging these technologies, lenders can better anticipate and manage ESG-driven risks.

Financial Protection through Insurance

Trade credit insurance plays a vital role in mitigating risks tied to ESG factors, such as defaults caused by climate-related events, supply chain disruptions, or geopolitical issues like sanctions and civil unrest. This type of insurance not only provides a safety net but also enables businesses to offer more competitive credit terms and explore markets with higher ESG-related volatility. In doing so, it addresses risks that traditional credit assessments might overlook, offering a more comprehensive layer of financial protection.

6. Secure Trade Credit Insurance Coverage

Credit Risk Reduction

Trade credit insurance (TCI) plays a key role in reducing risks like payment defaults, counterparty issues, and liquidity challenges. It typically covers up to 90% of losses caused by commercial or political risks, providing a safety net for businesses when payments fail. As defaults remain a leading cause of business closures, this type of coverage has become increasingly important.

Financial Protection through Insurance

Despite its benefits, only about 15% of global trade transactions are insured. However, projections show that the TCI market will grow from $12.2 billion in 2024 to $13.3 billion in 2025. Marc Wagman, Managing Director of Credit and Political Risk at Gallagher, highlights the critical role of TCI:

"Typically, receivables – the lifeblood of a company fueling cash flow – are the largest uninsured asset on the balance sheet. Having the insurance facilitates global trade".

Premiums for TCI are relatively affordable, ranging from 0.1% to 0.4% of the invoice value. This makes it a cost-effective way to strengthen the risk management strategies already in place.

Technology Integration

Modern technology has further improved the efficiency of TCI. Providers now use AI-powered systems to deliver real-time data, send automated alerts about client rating changes, and simulate tariff impacts. These tools streamline claims processing and make daily credit monitoring more efficient, allowing businesses to adjust credit limits proactively.

Portfolio Diversification

TCI also enables businesses to explore new or higher-risk markets with greater confidence. By combining global economic insights with local underwriting expertise, insurers adopt a "glocal" approach that supports competitive open-account terms in challenging markets. Additionally, insured receivables often improve banking relationships, leading to better funding options and interest rates.

Risk Management Planning

Beyond financial coverage, TCI providers offer expert risk management services. These include conducting due diligence, negotiating payment terms, and running scenario analyses. Sarah Murrow, President and CEO of Allianz Trade Americas, underscores the importance of TCI during uncertain times:

"As was demonstrated during COVID, trade credit insurance is vital to keeping liquidity in supply chains. It is critical for maintaining liquidity and supply chain stability".

Sharing financial information and maintaining open communication with insurance providers can help businesses secure better terms and build stronger partnerships.

For customized solutions to manage trade credit risks, visit Accounts Receivable Insurance to explore tailored policies designed to meet your needs.

Conclusion

In 2026, navigating global credit risks requires a proactive and multi-faceted approach that turns credit management into an opportunity for growth. The six strategies discussed – forward-looking stress testing, portfolio diversification, AI-powered analytics, risk-based pricing, ESG integration, and trade credit insurance – work together to create a comprehensive framework. This approach allows businesses to offer competitive credit terms, confidently operate in higher-risk markets, and maintain financial stability during economic uncertainty.

With about 25% of business bankruptcies stemming directly from payment defaults, the gap between risk exposure and protection remains a critical concern. Andy J. Arduini, SVP at Huntington Bank, poses a vital question:

"How are companies going to protect themselves in the context of a much slower global economic environment?".

Technology stands out as a key enabler for addressing this challenge. AI-powered tools provide real-time monitoring, automated alerts, and tariff simulators, helping businesses predict defaults before they happen. This level of foresight offers the agility needed to adapt to rapid changes like geopolitical fragmentation, rising tariffs, or supply chain disruptions. Moreover, improved credit protection directly enhances financing conditions by reducing lender risk, which in turn strengthens working capital and financing terms. By centralizing global credit policies and automating routine tasks, companies can redirect internal resources toward growth-oriented activities instead of being bogged down by administrative work.

Adopting these strategies does more than just safeguard receivables – it supports business expansion, aligning with the broader goal of adapting to evolving credit risks. For businesses looking for tailored solutions, Accounts Receivable Insurance offers policies designed to protect both domestic and international trade. In today’s unpredictable economic landscape, acting swiftly to secure robust protective measures is essential.

FAQs

How do I run a credit stress test without a big data team?

Running a credit stress test doesn’t have to be complicated – you can use straightforward tools and scenarios to get the job done. Start by focusing on essential financial metrics, such as sales, accounts receivable, and cash reserves. From there, create simple "what-if" scenarios. For example, consider the impact of a 20% drop in sales or delayed customer payments on your cash flow.

To stay ahead, keep a close eye on your accounts receivable. You can also leverage third-party risk data to uncover potential weaknesses in your financial setup. This proactive approach helps you spot challenges early and prepare accordingly.

What’s the fastest way to reduce customer concentration risk?

To reduce customer concentration risk quickly, the best approach is to diversify your customer base. By entering new markets or targeting different customer segments, you can create a more balanced and reliable revenue stream. On top of that, trade credit insurance can be a valuable tool in this process. It helps safeguard your business against risks like non-payment or financial instability when dealing with new customers, giving you added protection as you grow.

When does trade credit insurance make sense for my receivables?

Trade credit insurance becomes essential when offering credit to buyers involves a significant risk of non-payment, default, or insolvency. It proves particularly helpful during periods of economic or geopolitical uncertainty, as it protects cash flow and reduces exposure to bad debt. This type of coverage allows businesses to stay financially stable while managing unpredictable credit challenges.