Sanctions compliance is critical for businesses engaged in international trade. Violating sanctions – whether intentional or not – can result in severe penalties, disrupted operations, and long-term reputational damage. Here’s what you need to know:

- What Are Sanctions? Restrictions imposed by governments to block transactions with specific countries, industries, or individuals. Examples include embargoes on Cuba, Iran, and North Korea or restrictions targeting Russia’s energy and defense sectors.

- Consequences of Noncompliance: Financial penalties can reach $377,700 per violation in the U.S., with criminal fines up to $1,000,000 and 20 years in prison for intentional breaches.

- Key Regulations: U.S. OFAC, EU, and UN sanctions require businesses to monitor and avoid dealings with sanctioned parties. Compliance spans industries, from finance to shipping.

- Compliance Essentials: Build a program with management commitment, risk assessments, screening tools, regular audits, and employee training. Automated tools help flag risks, while tailored policies ensure proper oversight.

- Protective Measures: Accounts receivable insurance can mitigate financial risks from sanctions-related disruptions, offering coverage for unpaid debts and political instability.

Staying compliant requires vigilance, strong internal controls, and ongoing education. This guide outlines actionable steps to safeguard your business from sanctions risks.

OFAC Sanctions Programs and Compliance Guidelines: Navigating U.S. Financial Controls

sbb-itb-2d170b0

Major Sanctions Regulations You Need to Know

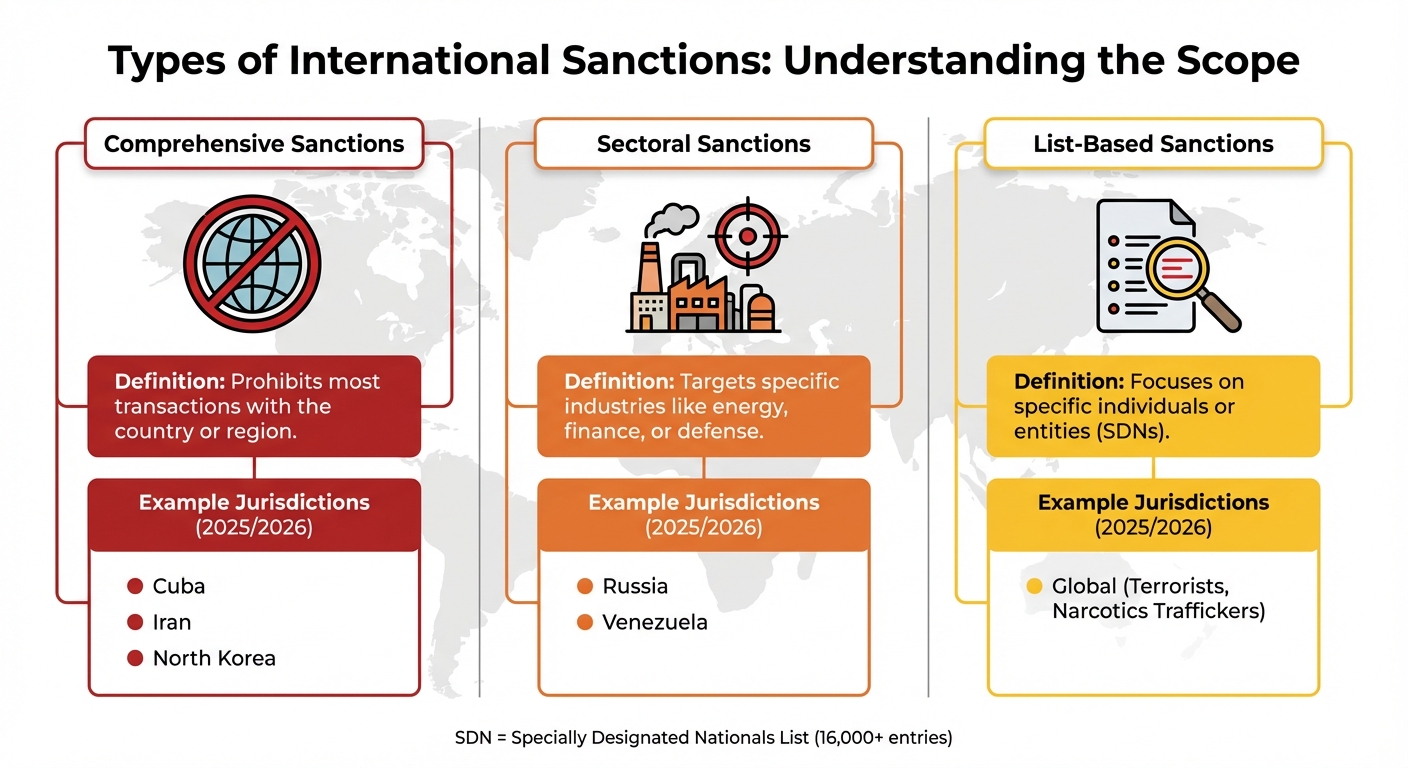

Types of International Sanctions and Their Scope

Understanding key sanctions regulations is essential when creating an effective compliance program. These frameworks often overlap, with distinct rules, enforcement strategies, and penalties, making compliance a complex undertaking.

US OFAC Sanctions

The Office of Foreign Assets Control (OFAC), part of the U.S. Department of the Treasury, oversees the most extensive sanctions program globally. OFAC regulations apply to U.S. citizens, permanent residents (regardless of location), individuals physically present in the U.S., and U.S.-incorporated entities, including their foreign branches.

OFAC enforces comprehensive sanctions against countries such as Cuba, Iran, and North Korea, prohibiting nearly all transactions with these nations. It also implements sectoral sanctions targeting industries like energy, finance, and defense in countries like Russia, and list-based sanctions that focus on individuals and entities included on the Specially Designated Nationals (SDN) List, which currently exceeds 16,000 entries.

U.S. persons are required to block and report any property linked to sanctioned parties within 10 business days. Additionally, they are prohibited from facilitating transactions by foreign affiliates that would be illegal if conducted directly by a U.S. person. For example, referring business involving sanctioned regions to a non-U.S. subsidiary is not allowed.

OFAC’s enforcement actions highlight the consequences of noncompliance. In January 2025, GVA Capital faced a record penalty of $215.99 million for managing U.S. investments tied to a sanctioned Russian oligarch and failing to respond to an OFAC subpoena. That same year, Interactive Brokers LLC paid $11.83 million for servicing clients in sanctioned jurisdictions, revealing lapses in automated screening and internal controls. Other notable cases include Unicat Catalyst Technologies, LLC, which paid $3.88 million for violations related to Iran and Venezuela, and Harman International Industries, which faced a $1.45 million penalty for Iran sanctions violations.

Businesses can seek relief through OFAC’s licensing system. General Licenses allow certain activities without prior approval, while Specific Licenses are granted on a case-by-case basis for transactions that would otherwise be prohibited. However, using these licenses requires thorough legal review and documentation.

EU and UN Sanctions

The United Nations Security Council imposes sanctions that all UN member states must implement through their national laws. The U.S. enforces UN sanctions under the United Nations Participation Act (UNPA), while the EU incorporates them directly into EU law, making them mandatory across its Member States.

In addition to UN sanctions, the European Union adopts its own "autonomous sanctions" under its Common Foreign and Security Policy (CFSP). According to the European Commission:

EU restrictive measures are not punitive. They are intended to bring about a change in bad or harmful policies or activities by targeting the non-EU countries, including organisations and individuals, responsible.

EU sanctions apply to EU nationals worldwide, individuals within the EU, and entities operating or incorporated in the EU. The EU currently enforces over 40 sanctions regimes, which include arms embargoes, travel bans, asset freezes, and restrictions on imports and exports.

For U.S. companies with global operations, this creates a dual compliance challenge. Navigating both OFAC and EU requirements can be tricky, as their scopes and targets may differ. To assist businesses, the EU offers tools like the EU Sanctions Map and a Consolidated List of sanctioned persons and entities. Small and medium-sized businesses can also use the EU Sanctions Helpdesk for free due diligence support.

A notable complication is the EU’s "blocking statute" (Council Regulation (EC) No 2271/96), which protects EU entities from the extraterritorial application of certain non-EU laws, including some U.S. sanctions. This can put multinational companies in a tough spot, caught between conflicting legal obligations.

Other International Sanctions Programs

In addition to OFAC, UN, and EU sanctions, businesses must track regulations from countries like the United Kingdom, Canada, and the G7 coalition. While each jurisdiction has unique enforcement priorities, they often collaborate on major initiatives.

A prominent example is the G7 Price Cap, a collective effort to limit the maritime transport of Russian oil and petroleum products unless purchased at or below a specified price. This measure directly impacts shipping, insurance, and logistics businesses involved in energy trade.

The U.S. also enforces anti-boycott laws, which prohibit American companies from complying with unauthorized foreign boycotts, such as the Arab League boycott of Israel. Violations can result in civil and criminal penalties, adding another layer of complexity for companies operating in the Middle East.

Secondary sanctions are another key area to watch. These target non-U.S. entities engaging in "significant transactions" with sanctioned sectors or individuals in countries like Iran, Russia, and North Korea, even if the transaction has no direct U.S. connection. U.S. authorities frequently use a "tri-seal" approach – coordinating efforts between the Department of Justice (DOJ), OFAC, and the Bureau of Industry and Security (BIS) – to pursue foreign actors.

For instance, in April 2022, Toll Holdings Limited, an Australian freight company, paid $6,131,855 to settle liability for 2,958 apparent violations involving North Korea, Iran, and Syria. Similarly, in June 2023, Swedbank Latvia AS paid $3,430,900 for 386 violations of Crimea sanctions after a customer accessed its e-banking platform from a sanctioned jurisdiction.

| Sanctions Type | Scope | Example Jurisdictions (as of 2025/2026) |

|---|---|---|

| Comprehensive | Prohibits most transactions with the country or region. | Cuba, Iran, North Korea |

| Sectoral | Targets specific industries like energy, finance, or defense. | Russia, Venezuela |

| List-Based | Focuses on specific individuals or entities (SDNs). | Global (Terrorists, Narcotics Traffickers) |

Effective compliance requires robust screening against all relevant sanctions regimes. This includes monitoring updates from multiple jurisdictions, screening transactions against various lists, and maintaining detailed records for at least five years. The next section will guide you through developing a compliance program to address these challenges.

How to Build a Sanctions Compliance Program

Creating a sanctions compliance program isn’t just about meeting legal requirements – it’s about protecting your business from penalties that can climb as high as $377,700 per violation under the International Emergency Economic Powers Act. To help organizations navigate this, the Office of Foreign Assets Control (OFAC) outlines five key pillars for success: management commitment, risk assessment, internal controls, testing and auditing, and training.

The first step? Gaining full buy-in from senior management. As OFAC puts it:

"Senior Management’s commitment to, and support of, an organization’s risk-based ICP is one of the most important factors in determining its success."

This involves appointing a dedicated Sanctions Compliance Officer (SCO) who has the authority to enforce policies and direct access to leadership. Your compliance efforts should reflect the unique risks tied to your business – whether that’s your customer base, supply chain, geographic reach, or the products and services you offer. Keep in mind that sanctions violations operate under strict liability, meaning your company can face consequences even if the breach was unintentional or due to lack of awareness.

Failures in compliance often stem from weak internal controls and oversight. For example, British American Tobacco p.l.c. paid $508 million in April 2023 to settle allegations involving North Korea and weapons proliferators. Similarly, Seagate Technology LLC and its Singaporean subsidiary reached a $300 million settlement over export control violations. Adding to the challenge, recent legislation (U.S. HR 815, signed in April 2024) extended the statute of limitations for sanctions violations to 10 years, requiring businesses to maintain detailed documentation for a decade.

Let’s break down the essential components of a compliance program: crafting internal policies, using advanced screening tools, and ensuring employees are well-trained.

Creating Internal Policies and Procedures

Your compliance program starts with strong, written policies. These documents should clearly define responsibilities, outline approval processes for high-risk transactions, and establish clear escalation pathways when potential violations arise. Here’s what to focus on:

- Departmental roles and escalation protocols: Specify how each department involved in international transactions should respond to red flags. For instance, when a screening tool flags a potential issue, there should be a clear process for escalating it to the compliance officer within set timeframes.

- Record-keeping: Maintain detailed documentation for every compliance decision – recording why a transaction was approved or denied, the screening checks performed, and the individuals involved in the decision-making process.

Your policies should also address merger and acquisition (M&A) due diligence. By integrating compliance into the M&A process, you can identify sanctions risks before finalizing deals, ensuring risks are managed across all activities. Common pitfalls include software errors (e.g., failing to account for alternative spellings like "Habana" vs. "Havana"), decentralized compliance efforts, and misunderstandings of how U.S. regulations apply to foreign subsidiaries.

Using Screening and Monitoring Tools

Automated screening tools are critical for identifying sanctioned parties and preventing prohibited transactions. Since sanctions lists can update multiple times a week, manual checks simply aren’t feasible.

Here’s how to make screening effective:

- Name screening: Use this during customer onboarding and for periodic database reviews.

- Transaction screening: Monitor payment messages, invoices, and shipping documents in real time.

- Advanced programmatic screening: Deploy software that uses risk-based scoring to cross-check parties against global databases.

Advanced matching techniques – like fuzzy matching, phonetic algorithms, and alias detection – help account for misspellings, alternative writing systems (Cyrillic, Arabic), and shell companies. The key is finding the right balance: overly strict thresholds could lead to missed sanctions (false negatives), while overly loose thresholds may overwhelm you with irrelevant matches (false positives).

Keeping your data fresh is non-negotiable. Update screening systems daily or even hourly, and consider automated screening APIs that deliver near-instant results with high reliability. Transaction-level screening is also crucial – flagging risks such as ports in sanctioned regions or vessels of concern. Additionally, tools that map corporate ownership structures can uncover hidden sanctioned entities. For seamless operations, integrate these tools with your CRM, ERP, or procurement systems, and maintain a detailed audit trail of every screening decision.

Once your tools are in place, the next step is ensuring your staff knows how to use them effectively.

Training Your Employees

Training is the glue that holds your compliance program together. Employees need to understand their responsibilities and recognize potential violations. As Kristine Kelleher, Trade Compliance Consultant at Export Solutions, explains:

"Employees must receive thorough training on screening procedures and understanding how sanctions impact various transactions. This knowledge empowers them to avoid prohibited activities."

Annual training is a must, but it shouldn’t be one-size-fits-all. Tailor sessions to different roles: sales teams should learn to spot red flags in customer behavior, while finance teams need to master payment screening processes. Use real-world case studies and knowledge checks to reinforce learning on key topics like:

- Identifying and reporting prohibited transactions

- Recognizing suspicious activity

- Following due diligence protocols

- Maintaining mandatory records

- Escalating potential violations appropriately

Extend training to all subsidiaries, affiliates, and third-party contractors involved in compliance. Encourage a workplace culture where employees feel safe reporting potential issues without fear of retaliation.

Finally, emphasize the importance of voluntary self-disclosure. Reporting a violation within 30 days of discovery can significantly reduce penalties, so employees should understand the urgency of flagging issues promptly. With the right training, your team becomes a vital part of your compliance strategy.

Sanctions Compliance Best Practices

Creating a strong sanctions compliance program goes beyond just drafting policies. It’s about actively identifying weaknesses, staying ahead of new threats, and layering protections effectively. Here’s how you can strengthen your compliance strategy.

Conducting Risk-Based Assessments

Start by reviewing every aspect of your operations – clients, products, supply chains, intermediaries, and geographic reach. The goal? Understand your inherent risk, which is your exposure before implementing any controls. Risks are often categorized as High, Moderate, or Low.

Pay close attention to these three risk areas:

- Geographic Risk: Look at operations or transactions tied to sanctioned countries or regions known for facilitating prohibited activities, often referred to as "circumvention hubs".

- Customer Risk: Screen for Politically Exposed Persons (PEPs), high-net-worth individuals, or complex corporate structures that may obscure ownership.

- Product Risk: Assess items like dual-use goods (those with both civilian and military applications) and high-risk sectors such as arms, energy, or luxury products.

Don’t forget the 50 Percent Rule, which addresses ownership risks. Once you’ve identified your inherent risks, evaluate how well your internal controls – like screening tools or alert review processes – reduce those risks. Regularly reassess these risks, especially when entering new markets or as sanctions laws evolve.

As sanctions.io describes it:

A sanctions risk assessment is a systematic evaluation of an organisation’s exposure to the risks associated with violating sanctions laws and regulations.

With inherent risks mapped out, the next step is diving deeper with enhanced due diligence.

Performing Enhanced Due Diligence

While standard screening can catch obvious issues, Enhanced Due Diligence (EDD) digs deeper into complex or high-risk situations. EDD employs methods like applying the 50 Percent Rule, reconciling transliteration variations (e.g., "Habana" vs. "Havana"), and conducting adverse media checks to uncover legal or reputational risks.

In mergers and acquisitions, EDD is critical to avoid inheriting sanctions liabilities. Scrutinize the target company’s transaction history, geographic reach, and compliance track record. Ensure your screening systems account for transliteration differences and regularly review "false hit" lists to avoid suppressing valid alerts when sanctions lists are updated.

The UK’s Office of Financial Sanctions Implementation (OFSI) advises:

Internal policies should provide robust and explicit guidance to staff regarding the escalation of potential sanctions concerns.

Clear escalation protocols are essential. Employees should know exactly how and when to report potential issues. Remember, voluntary self-disclosure can reduce penalties by up to 50%.

These thorough checks set the stage for effective audits and continuous improvement.

Running Regular Audits and Reviews

Once you’ve addressed risks and completed due diligence, regular audits ensure your compliance framework stays effective and adaptable. Audits verify that your program works as intended. Conduct annual internal audits and biennial external audits for an unbiased perspective. Key areas to examine include transaction sampling, screening logic, record-keeping, and reporting.

The U.S. Department of Justice evaluates compliance programs with three critical questions:

Is the corporation’s compliance program well designed? Is the compliance program being applied earnestly and in good faith? Does the corporation’s compliance program work in practice?

Audit findings should go straight to senior management and the Board of Directors. For example, in March 2025, the UK’s OFSI fined Herbert Smith Freehills CIS LLP £465,000 for failing to follow its own internal policies – proving that having procedures isn’t enough.

When audits reveal issues, conduct a root cause analysis to address systemic problems rather than just isolated incidents. Use these findings to refine screening tools, improve data quality, and adjust risk-scoring models as geopolitical conditions change.

Protecting Your Business with Insurance

Having strong internal controls is important, but safeguarding your business from financial risks is just as crucial for thorough sanctions compliance.

Even the best compliance program can’t eliminate every risk. Sanctions can shift overnight, buyers may unexpectedly default, and political turmoil can disrupt payments mid-transaction. This is where accounts receivable insurance steps in, offering a safety net against unforeseen financial shocks.

How Accounts Receivable Insurance Works

Export accounts receivable insurance (EARI) is designed to protect businesses when foreign buyers fail to pay due to sanctions, political instability, or bankruptcy. It also covers challenges like currency inconvertibility, transfer restrictions, and government actions such as expropriation, especially when sanctions target specific regions. For example, if new sanctions require you to exit a market – like Russia, Iran, or Cuba – this insurance can help soften the financial blow during the wind-down period.

But the benefits go beyond just protection. Businesses with this insurance often find it easier to secure financing because banks view them as lower-risk borrowers. This means trade credit may still be available, even in unpredictable markets. As ARI Global explains:

Export accounts receivable insurance is more than just a safety net. It is a strategic tool that empowers your business to navigate the complexities of international trade with confidence.

Considering that trade debts often account for about 40% of assets, the stakes are high. For a company operating on a slim 5% profit margin, losing $100,000 to bad debt would require generating about $2 million in new sales just to break even. This makes having the right insurance not just a precaution but a necessity.

Tailoring Coverage for International Markets

Standard insurance policies often fall short in addressing the unique challenges of international trade. Instead, you need coverage tailored to the specific risks tied to your trade destinations. For instance, if you’re exporting to Turkey, which borders sanctioned countries like Iran and Syria, your policy should account for the possibility of goods being diverted to prohibited markets.

Most tailored policies offer indemnity covering 80% to 100% of the debt amount. Premiums typically range from 0.1% to 0.9% of total sales, depending on factors like industry, trade regions, past losses, and the creditworthiness of your buyers. Leading insurers, such as Allianz Trade, assess risks by monitoring over 85 million companies across 52 countries. They also process 83% of credit limit requests in under 48 hours, ensuring timely support. Additionally, it’s wise to choose policies that address secondary sanctions, which could impact your business even without direct U.S. ties. Professional risk assessments can help uncover these exposures before they become problematic.

Using Professional Risk Assessment Services

Professional risk assessments add another layer of protection by thoroughly examining your business’s exposure and ownership structures.

These assessments go beyond basic sanctions list checks. They include "Know Your Business" (KYB) evaluations to uncover beneficial ownership structures, ensuring compliance with the 50 Percent Rule, which blocks entities largely owned by sanctioned parties. Investigators also conduct "outside-in" reviews, using local language searches and corporate registry checks to gain a clear picture of a target’s risk profile.

The insights gained from these assessments can enhance your compliance efforts. For example, you can use the findings to create role-specific training for employees working in high-risk trade areas, reducing the chances of screening errors caused by alert fatigue. Aligning your due diligence with your bank’s expectations may also improve your financing options.

By combining tailored insurance with thorough compliance strategies, you can build a strong defense against the complex risks of international trade. As Friling Law aptly states:

The cost of underinvesting in compliance far exceeds the investment required to build a strong program. In this environment, robust compliance is not just a legal necessity – it is a strategic advantage.

Conclusion

Key Points to Remember

U.S. sanctions come with strict liability, meaning even unintentional violations can result in penalties. Under laws like IEEPA, these penalties can be severe, including substantial fines and criminal charges.

These regulations have a global reach. If your business processes payments in U.S. dollars or uses U.S. financial institutions, U.S. sanctions apply to you, no matter where you’re located. And don’t overlook the 50 Percent Rule, which automatically blocks entities owned 50% or more by sanctioned individuals.

An effective compliance program is built on five essential pillars: management commitment, risk assessment, internal controls, testing and auditing, and role-specific training. These serve as your foundation for navigating the constantly shifting sanctions landscape. Pairing this program with accounts receivable insurance adds an extra layer of protection, shielding your business from compliance missteps and financial disruptions.

Action Steps for Your Business

To strengthen your compliance program, consider these practical steps:

- Appoint a Sanctions Compliance Officer: This individual should have direct access to senior management and the resources needed to enforce compliance effectively.

- Conduct a Thorough Risk Assessment: Evaluate your supply chain, customer base, and geographic exposure to identify vulnerabilities before regulators do.

- Automate Screening Processes: Use real-time software that updates against OFAC, EU, and UN sanctions lists. Manual methods can’t keep up with the frequent changes in designations. Ensure your systems can handle fuzzy matching, transliterations, and aliases to uncover hidden risks.

- Provide Role-Specific Training: Train employees in key areas like logistics and finance annually to help them recognize potential red flags and stay ahead of new risks.

If a violation does occur, report it immediately to OFAC or the DOJ. Early reporting often leads to reduced penalties or even a "no action" decision. For instance, in April 2023, Microsoft Corporation faced a fine of just under $3 million after showing significant improvements to its compliance practices.

Finally, bolster your compliance strategy with accounts receivable insurance. This added protection not only helps cover financial losses but also supports your efforts in managing risks across global markets. It’s a practical way to safeguard your business while staying compliant.

FAQs

Do U.S. sanctions apply to my non-U.S. company?

U.S. sanctions primarily focus on U.S. individuals and businesses, but they can extend beyond U.S. borders in specific situations. For instance, if your company has ties to the U.S. – like employing U.S. citizens, working with U.S. banks, or conducting transactions within the U.S. – you might fall under these sanctions. It’s crucial to grasp these rules to stay compliant and steer clear of any legal or financial consequences.

How can I verify beneficial ownership under the 50% Rule?

To verify ownership under the 50% Rule, you need to examine a company’s ownership structure to see if any individual or entity on the SDN (Specially Designated Nationals) list owns 50% or more, whether directly or indirectly. According to OFAC guidelines, if a sanctioned party holds 50% or more of a company, that company is automatically blocked. Engaging in transactions with such entities would violate sanctions regulations. Conducting thorough due diligence, like reviewing ownership documents, is essential to stay compliant.

What should I do if a transaction is flagged or I suspect a violation?

If you come across a flagged transaction or suspect a possible violation, take the time to investigate thoroughly. Determine whether it could involve a potential sanctions breach. To guide your investigation, follow OFAC’s risk-based approach to spot any red flags.

If you uncover evidence of a violation, it’s crucial to act quickly and self-disclose the issue to OFAC. Prompt disclosure can help reduce potential penalties. Additionally, consulting with legal or compliance professionals who are well-versed in OFAC regulations is a smart move to ensure the situation is handled appropriately.