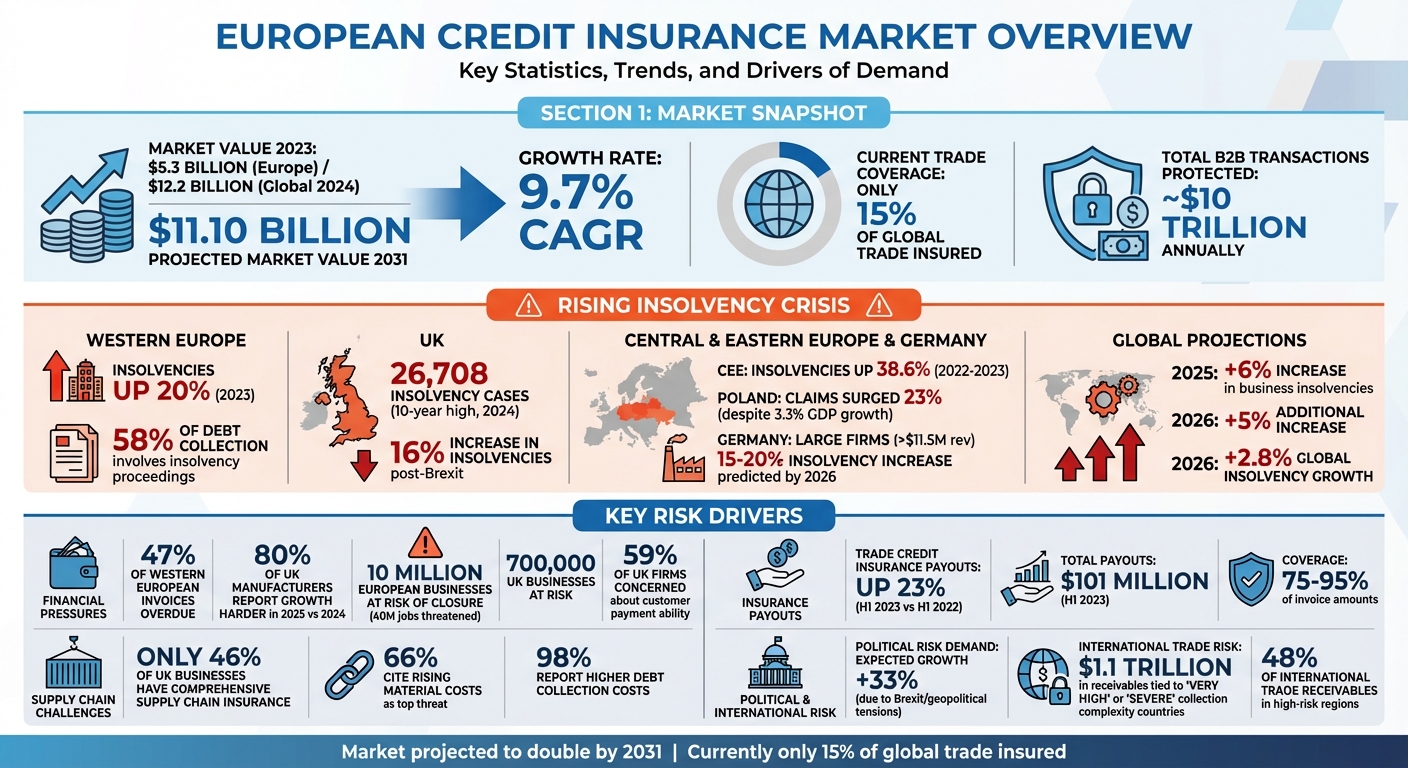

European businesses are facing rising financial and political risks, pushing many to seek credit insurance as a safety net. With insolvencies climbing across Europe – up 20% in Western Europe and 38.6% in Central and Eastern Europe in 2023 – companies are grappling with high borrowing costs, geopolitical tensions, and supply chain disruptions. Trade credit insurance, covering up to 95% of unpaid invoices, has become essential for maintaining cash flow and protecting against client defaults. The market, valued at $5.3 billion in 2023, is expected to double by 2031, highlighting its growing importance. Here’s why:

- Insolvencies Rising: Global insolvencies are predicted to increase by 2.8% in 2026, with large firms in Germany and the UK particularly vulnerable.

- Economic Pressures: Sluggish growth and tightened credit lines are straining liquidity, putting millions of businesses and jobs at risk.

- Geopolitical Instability: Brexit and conflicts like the Russia-Ukraine war are disrupting trade and increasing political risks.

- Supply Chain Challenges: Persistent disruptions and rising costs are leaving many businesses underinsured.

Credit insurance not only shields businesses from financial losses but also helps secure financing by guaranteeing receivables. With only 15% of global trade currently insured, the opportunity for expansion is vast. For companies navigating today’s volatile market, credit insurance is no longer optional – it’s a critical tool for survival and growth.

European Credit Insurance Market: Key Statistics and Growth Drivers 2023-2031

Economic and Financial Risks Driving Demand

Rising Insolvency Rates and Non-Payment Risks

When large firms collapse, the ripple effect on their suppliers and subcontractors can be devastating. In just the first half of 2023, trade credit insurance payouts surged by 23% compared to the same period in 2022, reaching $101 million to cover unpaid invoices. This sharp rise highlights how quickly payment defaults can escalate.

The situation is particularly concerning in the UK, where insolvency cases hit a 10-year high in 2024, with 26,708 cases recorded. In Germany, experts predict insolvencies among large companies – those generating over $11.5 million in revenue – could climb by 15% to 20% by 2026. France faces its own challenges, as a mere 1% reduction in credit availability results in a 2% rise in insolvencies, a far steeper impact than the 1% increase seen in the UK or the 0.4% rise in Germany.

In Western Europe, insolvency proceedings now account for 58% of the complexity in debt collection. High interest rates and sluggish growth are putting immense pressure on industries like construction and manufacturing, where thin profit margins and growing debt are common challenges. In this climate, trade credit insurance has become a critical safety net, covering 75% to 95% of invoice amounts and protecting businesses from client defaults and bankruptcies. These insolvency pressures are further intensified by the broader slowdown in economic growth.

Impact of Slow Economic Growth

Slow economic growth is squeezing liquidity across the board. Up to 10 million European businesses could be forced to shut down within two years if conditions don’t improve, placing 40 million jobs in jeopardy. In the UK alone, around 700,000 businesses are at risk, with 59% of firms expressing concerns about their customers’ ability to pay on time.

The tightening credit environment is adding to the strain. Banks and suppliers are restricting credit lines just as companies need them most. In 2025, 80% of UK manufacturing firms reported that growing their businesses had become more difficult due to credit risk constraints. Aylin Somersan Coqui, CEO of Allianz Trade, summed up the situation:

"The business environment has rarely been so complex and volatile, and corporates should remain alert to avoid non-payment risk".

In this uncertain economic landscape, credit insurance has become a vital tool. It safeguards insurer-backed credit limits, giving lenders the confidence to keep financing operations. These figures paint a clear picture of the financial challenges European businesses are grappling with today.

sbb-itb-2d170b0

Credit Insurance as a Risk Mitigation Tool for International Trade

Political Risks and Geopolitical Tensions

Beyond economic challenges, political risks are driving a growing demand for strong credit protection across Europe.

Brexit and Regulatory Changes

Brexit has reshaped the regulatory framework for trade between the UK and Europe. Hugh Savill, Director of Regulation at the Association of British Insurers, pointed out:

"It would be crazy not to admit that British influence on the future make up of Solvency II is diminished".

This diminished influence has led to a regulatory divide, complicating how insurers allocate capital and handle cross-border risks. The UK is revising Solvency II rules to unlock funds for infrastructure projects, while European regulators are taking separate paths on elements like the Volatility Adjustment and Risk Margin calculations. These differences add layers of complexity to compliance across borders.

For UK manufacturers and exporters, the fallout from Brexit has resulted in supply chain disruptions, increased input costs, and longer production timelines. These challenges have strained working capital and heightened credit risks. UK insolvencies rose by 16% as businesses grappled with post-Brexit challenges, and the demand for political risk insurance is expected to grow by 33% due to tariff uncertainties and unstable trading conditions.

While regulatory changes create hurdles in Northern Europe, broader geopolitical conflicts are adding to the instability.

Regional Conflicts and Political Instability

Ongoing conflicts in Ukraine and the Middle East are disrupting trade routes and creating payment uncertainties. These geopolitical tensions have elevated insolvency risks, especially in areas directly affected by conflict.

Maritime shipping routes, critical to global trade, are becoming increasingly vulnerable. As Credendo highlighted:

"Prominent sea routes that act as vital arteries for the global economy have become areas of tension and vulnerability in several parts of the world".

Heightened tensions have made shipping riskier, forcing companies to reroute cargo and absorb rising logistics costs. For instance, a June 2025 escalation involving Israel, Iran, and the US significantly impacted the Middle East, threatening energy supplies and global logistics networks.

In this volatile environment, trade credit insurance plays a crucial role in mitigating both regulatory and geopolitical risks. Sarah Murrow, President and CEO of Allianz Trade Americas, underscored its importance:

"Trade credit insurance is vital to keeping liquidity in supply chains. It is the glue that keeps world trade going".

Currently, about 15% of global trade is covered by trade credit insurance. With the market expected to grow from $12.2 billion in 2024 to $13.3 billion by 2026, businesses are increasingly turning to this protection to navigate geopolitical uncertainties and safeguard their operations.

Supply Chain and Commercial Insurance Pressures

Structural supply chain issues and changes in the insurance market are pushing European businesses to reassess how they protect their credit, on top of navigating political instability.

Global Supply Chain Vulnerabilities

Supply chain disruptions are no longer occasional hiccups – they’ve become a constant hurdle. However, insurance coverage hasn’t kept up with this new reality. Neil Hodgson highlighted this gap:

"Supply chain disruption has become a structural feature of the trading environment, while insurance protection has not kept pace".

The numbers paint a concerning picture. Only 46% of affected UK businesses have comprehensive insurance to cover these disruptions. On top of that, 66% of UK companies see rising material costs as their biggest supply chain threat. For manufacturers, the situation is even tougher – 80% say growth in 2025 is harder than in 2024.

These pressures are squeezing cash flow across Europe. For instance, 47% of invoices in Western Europe are overdue, and 98% of businesses outsourcing debt collection report higher collection costs over the past year. These ongoing challenges are forcing insurers to rethink their approach, leading to tighter coverage in commercial insurance.

Shift to Commercial Lines Insurance

Insurers in Europe are feeling the heat from these supply chain challenges. In Poland, for example, GDP grew by 3.3% in 2024, but insurance claims skyrocketed by 23% during the same period. Marcin Olczak, Head of Credit Risk at Marsh Poland, cautioned:

"We may soon pass the 60% loss ratio mark, which means insurers will tighten limits, raise premiums and restrict coverage for higher-risk sectors such as transport, construction and furniture".

This shift reflects a broader trend: traditional insurance profitability is becoming less tied to economic growth. Rising costs from tariffs and raw materials are driving claims inflation, especially in property and casualty lines. As a result, insurers are turning their focus to commercial lines, such as trade credit insurance.

The urgency for businesses to secure credit protection is growing. Global business insolvencies are expected to climb by 6% in 2025, with another 5% increase in 2026. For companies, now is the time to act while market capacity is still available and pricing remains competitive.

Trade Credit Insurance as a Risk Management Solution

With insolvencies on the rise and supply chains under pressure, trade credit insurance acts as a safeguard against financial and political risks that can disrupt cash flow and business operations.

Protection Against Financial and Political Risks

Trade credit insurance steps in to cover risks like insolvency and extended payment delays. Marc Wagman, Managing Director of Credit and Political Risk at Gallagher, highlighted its importance:

"Typically, receivables – a company’s lifeblood, essential for maintaining cash flow – are the largest uninsured asset on the balance sheet. Having the insurance greases the wheels of global trade."

Beyond financial risks, it also covers political challenges such as government interference, currency restrictions, expropriation, and the cancellation of import/export licenses. This is especially relevant given that 48% of international trade receivables, valued at approximately $1.1 trillion, are tied to countries with "Very High" or "Severe" collection complexity.

Additionally, lenders often use credit insurance limits as a basis for funding, meaning insured receivables can help businesses secure more financing. This combination of protection and financial flexibility supports companies in maintaining and growing their operations.

Trends in the Trade Credit Insurance Market

The European trade credit insurance market is on an upward trajectory. Valued at $5.29 billion in 2023, it’s expected to more than double to $11.10 billion by 2031, with a growth rate of 9.7% CAGR. Despite its potential, only 15% of global trade is currently insured, leaving a vast opportunity for expansion.

In 2023, large enterprises dominated the market, particularly for international transactions. However, small businesses are increasingly adopting trade credit insurance to strengthen credit management and optimize working capital.

Even as bankruptcies rose 7% in 2023 and are projected to climb another 9% by late 2024, the market remains in a "soft market" phase. This means competitive pricing, abundant capacity, and an aggressive appetite for risk. Ian Watts, Credit Risk Specialty Growth Leader at WTW, stressed the importance of this coverage:

"Most global trade is done on open account terms, where goods are shipped and delivered before payment is due. Companies cannot manage that risk [of non-payment] without trade credit insurance."

The market’s stability is further bolstered by major players like Allianz Trade, Coface, and Atradius, which together account for approximately 70% of the global risk capacity.

Custom Solutions from Accounts Receivable Insurance (ARI)

Europe’s complex risk environment calls for insurance solutions designed to handle unique challenges. Accounts Receivable Insurance (ARI) steps in by crafting policies that address both financial and political risks in domestic and international trade. These personalized solutions tackle the growing issues of insolvency and geopolitical uncertainty, forming the backbone of ARI’s specialized offerings.

Customized Policies for Domestic and International Markets

ARI begins by conducting a thorough due diligence analysis of each policyholder’s customers. This involves assigning tailored credit limits based on detailed financial evaluations. What sets these policies apart is their flexibility during the coverage period, as terms are adjusted to reflect real-time changes in a customer’s financial health and creditworthiness.

For businesses expanding into European markets, ARI collaborates with leading global carriers like Allianz Trade, Coface, and Atradius. These partnerships bring together localized expertise and extensive market data, enabling companies to request custom credit limit increases for high-value or new clients within their existing policies. Political risk coverage is another key feature, offering protection against issues such as currency inconvertibility, government expropriation, transfer restrictions, and breaches of contract by foreign entities. These safeguards are especially critical in light of Brexit-related regulatory changes and ongoing geopolitical challenges.

"Accounts receivable (trade credit) insurance is not a one-size-fits-all solution; we work with you to design a policy that aligns perfectly with your business model and risk tolerance."

Additionally, ARI’s access to the International Credit Brokers Alliance provides businesses with early warnings about unfavorable economic conditions in specific markets. This allows companies to make better-informed decisions before extending credit to new trading partners. Advanced risk analytics further enhance these policies, supporting proactive claims management and helping businesses stay ahead of potential risks.

Risk Assessment and Claims Support

ARI employs AI-powered analytics and big data to predict payment defaults and market trends with greater precision than traditional methods. These tools also enhance fraud detection and enable continuous monitoring of customer financial health, identifying potential insolvency risks before they escalate into losses.

Unlike many providers that delegate claims handling to administrative staff, ARI ensures that the licensed broker who structured the policy provides expert guidance throughout the claims process. As one of fewer than a dozen U.S. credit insurance advisors recognized as an Elite/Preferred Broker by major insurers, ARI brings a level of expertise that few competitors can match.

Another standout feature is ARI’s non-cancelable policies, which guarantee coverage remains intact even if an insurer’s risk assessment of a specific buyer changes during the policy term. This stability is particularly valuable during uncertain economic times when consistent protection is most needed. Through the Global Credea Network, ARI also offers support for navigating complex claims across European and global markets, ensuring businesses recover losses caused by non-payment efficiently and effectively.

Practical Strategies for Risk Management

Managing risk effectively requires taking proactive steps, especially when it comes to credit insurance. Insurers play a key role as partners by consistently monitoring the financial health of your customers and adjusting credit terms before any defaults occur. Early warning systems are particularly useful, allowing for timely adjustments that can help prevent financial setbacks. These measures create a foundation for customized policy solutions.

Policy Customization and Pre-Claim Interventions

Maintaining open communication with your insurer is essential. Sharing management information and financial statements not only builds trust but can also lead to better coverage terms. Addressing late payments as soon as they arise is another critical step to avoid defaults.

Strengthening your credit controls is equally important. Train your accounts receivable team to recognize warning signs and implement a structured escalation process to speed up collections and reduce bad debt. Mike Seff, Senior Vice President of Specialty Lines at Intact Insurance Specialty Solutions, underscores this approach:

"In uncertain times, companies often pull back by delaying investments, cutting costs and reducing risk exposure. But when done strategically, trade credit management helps you avoid the trap of false confidence".

Diversifying your customer base is another way to manage risk. If a single buyer accounts for a large share of your receivables, consider expanding into new markets to spread that risk. For high-value clients whose coverage needs exceed what your primary insurer can provide, explore syndicated solutions or supplemental coverage to close the gap.

Using Market Analysis for Better Decisions

Internal controls are vital, but combining them with market analysis can refine your risk management strategy even further. Tools like ARI’s market analysis platforms offer valuable insights into carriers, coverage options, and regional risks. Working with trusted broker networks can also provide early warnings about economic challenges in specific markets, helping you make informed credit decisions before engaging with new trading partners.

AI-powered analytics take this a step further by simulating how changes in tariffs or trade policies might affect credit risk. Unlike traditional models that rely on historical data, these tools allow businesses to map their supply chains and assess risks such as disruptions or over-concentration. With credit insurers covering roughly $10 trillion in B2B transactions annually – about 10–15% of global trade – their data and expertise become invaluable for managing exposure to unstable regions or industries under stress. Together, these strategies can enhance your ability to navigate the complex risks of today’s markets.

Conclusion

Europe’s business environment is grappling with a serious convergence of financial and political challenges. Between 2015 and the second quarter of 2023, bankruptcies across the EU surged by 8.4%, while insolvency rates in Central and Eastern Europe climbed an alarming 38.6% from 2022 to 2023. Compounding this issue, nearly half of all international trade receivables – representing approximately $1.1 trillion – are tied to countries with "Very High" or "Severe" collection complexity. Once a buyer falls into formal insolvency, the likelihood of full recovery diminishes sharply, particularly in regions with slow or expensive legal systems.

Credit insurance has emerged as a key response to these risks, offering businesses a way to safeguard their financial health. It ensures more predictable cash flow, lowers the need for large bad debt reserves, and improves access to financing. Insured receivables give lenders greater confidence, enabling businesses to secure the working capital necessary for growth. The increasing demand for credit insurance highlights its importance in maintaining financial stability.

Beyond offering protection, credit insurers play an active role in global trade. They support trillions in B2B transactions, protecting a substantial share of commerce. Their services go beyond simple coverage, offering real-time insights into buyer solvency, market trends, and portfolio risks. This data-driven support empowers businesses to make forward-looking decisions rather than relying solely on historical payment patterns.

As insolvencies rise, geopolitical tensions persist, and supply chain disruptions continue, credit insurance has become an essential tool for navigating financial uncertainty. Companies that adopt tailored policies, strengthen internal controls, and utilize market analysis are far better equipped to weather these challenges. Allianz Trade emphasizes this urgency, noting:

"Recovering commercial debt is set to become even more challenging for exporters as business insolvencies remain elevated in most countries and global fragmentation accelerates".

In this volatile European market, prioritizing credit risk management isn’t optional – it’s a necessity. By integrating credit insurance into their broader strategy, businesses can bolster their resilience and position themselves for long-term success. This proactive approach is critical for addressing the complexities of today’s economic landscape.

FAQs

How do I know if my business needs trade credit insurance now?

Your business might benefit from trade credit insurance if you offer credit terms to customers or suppliers and worry about risks like non-payment, bankruptcies, or political instability. In times of increasing insolvencies and economic unpredictability, this type of coverage can safeguard your cash flow, support liquidity, and help manage financial risks. It’s particularly useful if your industry is deeply tied to international trade or frequently faces challenges like delayed payments or global political upheaval.

What payments and political events does trade credit insurance cover?

Trade credit insurance helps businesses shield themselves from financial setbacks caused by buyer non-payment or political upheaval. This coverage steps in during situations like a buyer defaulting on payments, currency becoming non-convertible, import or export licenses being revoked, or even expropriation. By addressing these risks, it helps businesses maintain stability even in the face of political or economic disruptions.

How can insured receivables help me get more working capital from lenders?

Insuring receivables helps stabilize cash flow and provides dependable collateral, which can simplify securing favorable financing terms. When receivables are safeguarded against risks like non-payment or bankruptcy, lenders feel more secure and are often willing to extend larger credit lines, knowing their risk of loss is reduced.