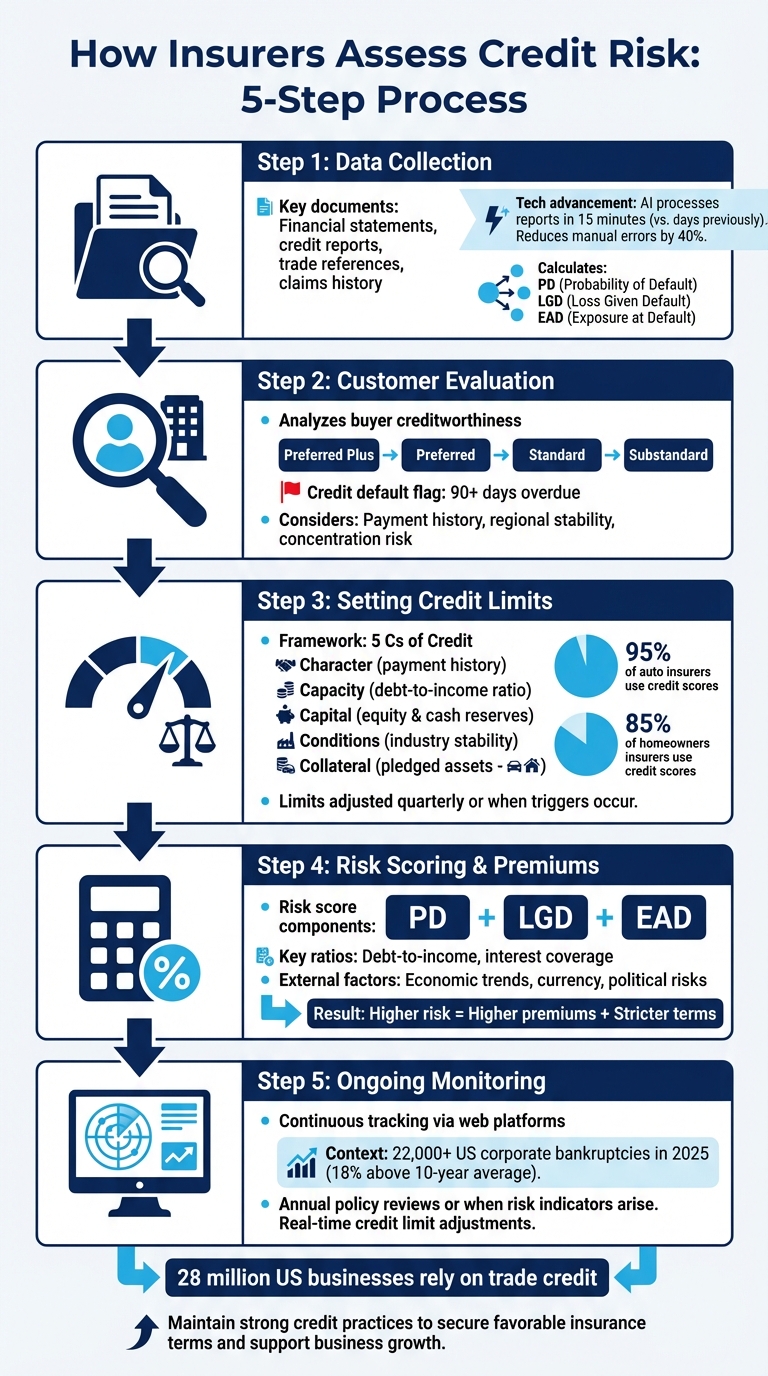

When you apply for trade credit insurance, insurers evaluate your financial risk to decide coverage, limits, and premiums. Their process answers one key question: How likely is it that your customers won’t pay? This involves analyzing your financial data, customer profiles, and market conditions to calculate risk metrics like Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD).

Here’s a quick breakdown of the process:

- Data Collection: Insurers gather financial statements, credit reports, trade references, and claims history to assess your business’s stability.

- Customer Evaluation: They analyze your buyers’ creditworthiness and classify them into risk categories based on payment history and financial health.

- Setting Credit Limits: Credit limits are determined using frameworks like the "5 Cs of Credit" (Character, Capacity, Capital, Conditions, Collateral).

- Risk Scoring and Premiums: Risk scores are calculated to determine premiums. Higher risk means higher costs and stricter terms.

- Ongoing Monitoring: Insurers continuously track financial health and adjust coverage as conditions change.

This detailed analysis helps insurers balance risk while offering you coverage tailored to your needs. Keeping your financials strong and maintaining open communication with your insurer can improve your terms.

5-Step Credit Risk Assessment Process for Trade Credit Insurance

Credit Risk Managment – Credit Analysis and Risk Assessment

Step 1: Collecting Financial Data and Documents

Before an insurer can assess your credit risk, they need a comprehensive understanding of your financial situation. This begins with gathering key documents that demonstrate financial stability and confirm your ability to meet payment obligations. This initial data collection forms the basis for decisions about credit limits, premium rates, and overall risk evaluation.

Required Documents

Insurers usually ask for core financial statements, such as income statements and balance sheets, to evaluate your profitability, debt levels, and overall financial health. They also request trade and bank references to verify payment reliability and establish a track record of timely transactions.

Another essential document is the business credit report, which provides a snapshot of your creditworthiness based on public records and historical payment data. If your business owns significant property, insurers may require a Statement of Values (SOV) and property condition reports. Additionally, loss runs, which detail claims history, help insurers estimate the likelihood and impact of future claims. In cases where financial data reveals potential risks, insurers might ask for personal or corporate guarantees to secure the proposed credit exposure.

Thanks to advancements in technology, this process is now much quicker. AI-powered tools can process financial reports and property assessments in about 15 minutes, a task that previously took days. Automated tools also reduce manual data entry errors by up to 40%.

These documents serve as the foundation for assessing risk and determining creditworthiness.

Building the Risk Foundation

Once the necessary data is collected, insurers calculate key risk metrics to evaluate your credit profile. This includes three main factors: Probability of Default (POD), which estimates the likelihood of non-payment; Loss Given Default (LGD), which predicts potential losses in case of default; and Exposure at Default (EAD), which measures the total financial exposure at risk. As noted by the CFI Team:

If the lender fails to detect the credit risk in advance, it exposes them to the risk of default and loss of funds.

Insurers often use frameworks like the "5 Cs of Credit" to organize and analyze the data. For example, a low debt-to-income ratio is a strong indicator of creditworthiness and can lead to better terms.

To ensure accuracy, insurers cross-check your financial data with external factors like market conditions and industry standards. They also independently verify references, rather than relying solely on the contacts you provide, to avoid missing any red flags. In most cases, credit default risk is identified when a borrower falls 90 days behind on a loan repayment.

Step 2: Evaluating Customer and Buyer Profiles

Once financial data has been collected, insurers turn their attention to evaluating the buyers connected to your business. This step ensures that external credit factors align with your financial standing. Even if your internal finances are solid, high-risk buyers can still increase your overall risk profile. Timely payments from your buyers play a critical role in keeping that risk low.

Evaluation Criteria

When assessing a buyer’s creditworthiness, insurers consider several important factors. One of the primary metrics is the Probability of Default (POD), which estimates the likelihood that a buyer will fail to meet payment obligations. For corporate buyers, this figure often comes from trusted credit rating agencies like Moody’s or Standard & Poor’s.

Additionally, insurers review two other metrics:

- Loss Given Default (LGD): This measures the potential financial loss if a buyer does default.

- Exposure at Default (EAD): This reflects the total financial exposure tied to that particular buyer.

Beyond these metrics, insurers also take into account regional and political stability, which can influence a buyer’s ability to make payments. Another key consideration is concentration risk – relying too heavily on a single buyer or industry sector could lead to substantial financial losses. As the CFI Team highlights:

“If the lender fails to detect the credit risk in advance, it exposes them to the risk of default and loss of funds”.

To track changes in buyers’ creditworthiness over time, insurers use tools like transition matrices, which help forecast potential shifts in credit ratings.

Risk Classification

After gathering and analyzing buyer data, insurers categorize customers into risk groups based on their credit profiles. These classifications are then combined with financial data to create a full picture of your risk exposure. This process helps insurers set accurate premiums and manage risk effectively. Common risk categories include:

- Preferred Plus: Buyers with excellent payment histories and minimal risk.

- Preferred: Buyers considered low-risk.

- Standard: Buyers with average risk profiles.

- Substandard or Rated: Buyers with higher risk due to past issues.

A buyer is often flagged as a credit default risk if they are more than 90 days overdue on a payment. To streamline this process, many insurers now use automated underwriting systems and predictive modeling, which allow for faster and more precise risk classification.

Since risk profiles can shift over time, it’s important to inform your insurer about major business changes – like losing a key customer or entering a new market. This ensures your classification and premiums remain accurate and reflect your current situation.

Step 3: Setting Credit Limits

Once buyers are categorized into risk groups, insurers decide how much credit exposure they’re willing to cover for each one. This step involves a mix of data-driven metrics and professional judgment, building on the earlier risk classifications. These decisions directly shape the credit limits insurers set and adjust for your buyers.

Credit Limit Calculations

Credit limits are determined based on the buyer’s risk profile and classification. Insurers often rely on the "5 Cs of Credit" – Character, Conditions, Capital, Capacity, and Collateral – as a framework to guide their decisions.

- Character: A buyer’s payment history is scrutinized, including credit reports that highlight late payments, collections, or tax liens.

- Capital: Insurers examine balance sheets to confirm positive equity and adequate cash reserves.

- Capacity: This involves assessing the buyer’s ability to meet financial obligations, often through income verification and debt-to-income ratios.

- Conditions: External factors, such as the stability of the buyer’s industry, are also considered.

- Collateral: Any pledged assets that could help mitigate potential losses are reviewed.

Additionally, insurers use credit scores derived from credit report data to guide their decisions. These scores play a significant role in setting credit limits. In fact, about 95% of auto insurers and 85% of homeowners’ insurers use credit scores in states where it’s permitted.

Adjusting Limits Over Time

Credit limits aren’t static – they evolve as new financial data becomes available. Insurers regularly monitor buyers and may adjust limits to reflect changes in risk profiles. For example, if a buyer demonstrates improved financial health, such as better cash flow or stronger balance sheets, insurers might ask if you’d like to request a higher limit. Similarly, seasonal businesses may need temporary increases during high-demand periods, like retailers preparing for holiday inventory.

On the flip side, credit limits can be reduced or even removed if negative indicators arise. Payment behavior is a critical factor; consistently late payments beyond the Maximum Extension Period can lead to reduced coverage. As Allianz Trade explains:

In some cases we will reduce or remove cover after receiving negative information. Any reduction or withdrawal will take effect in accordance with the terms of your Policy.

If a limit is lowered, insurers typically offer a 30-day grace period to cover existing deliveries. However, any new shipments after that point become the policyholder’s responsibility. It’s essential to respond quickly to Buyer Review Forms requesting updated information, as failing to provide the necessary details could result in immediate coverage removal.

To stay proactive, many insurers conduct regular reviews of buyer financial statements, often on a quarterly basis. Smaller accounts with a strong track record of timely payments might be reviewed only when certain triggers, like a payment default, occur. Maintaining open and transparent communication with your insurer is crucial to ensure credit limits remain aligned with both your business needs and the current risk landscape.

sbb-itb-2d170b0

Step 4: Calculating Risk Scores and Premiums

Once credit limits are established, insurers analyze financial data to generate risk scores. These scores play a crucial role in determining premiums and shaping policy terms.

Risk Score Components

Risk scores are built using metrics like Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD). Key financial ratios also come into play, such as the debt-to-income ratio, which measures obligations against earnings, and interest coverage ratios, which assess a buyer’s ability to cover interest payments with current earnings.

Beyond these, insurers take into account broader factors like economic trends, currency fluctuations, political risks, and potential trade sanctions – especially for businesses involved in international trade.

With the help of advanced technology, insurers can continuously monitor risks by comparing individual buyer profiles against vast datasets of industry transactions. These metrics directly feed into the calculations for premiums, which will be further explored in the next section.

How Risk Affects Premiums

Risk scores are a key driver of premium levels. Higher risk scores typically lead to higher premiums and stricter policy terms. For instance, businesses with buyers showing elevated PD scores or operating in unstable industries face increased premiums to offset the greater likelihood of claims. Similarly, a high LGD percentage might result in reduced coverage or require additional collateral.

EAD, which represents the total potential exposure an insurer could face, also impacts policy limits and premium rates. On the other hand, businesses with lower debt-to-income ratios often benefit from reduced premiums.

Insurers must carefully balance these factors. Policies that are too conservative might limit credit access for dependable customers, leading to missed opportunities. Conversely, overly lenient terms could leave insurers vulnerable to significant financial losses.

At Accounts Receivable Insurance, these sophisticated calculations form the foundation of our tailored trade credit policies. This ensures that premiums align closely with the specific credit risk profile of each business, offering both precision and fairness.

Step 5: Monitoring and Updating Risk Assessments

After the initial data collection and risk scoring, monitoring remains a vital step in refining credit limits and premiums. Risk assessment doesn’t end with the issuance of a policy. Instead, insurers continuously track the financial health of buyers and adjust coverage as conditions change. This ongoing vigilance safeguards both insurers and policyholders from unforeseen losses.

Continuous Risk Tracking

Insurers rely on web-based platforms to keep a close eye on financial health and to flag emerging risks. These tools track critical metrics like delinquency rates and debt-to-income ratios, offering early warnings of potential issues. For example, models like the FRISK® Score are specifically designed to detect early signs of financial distress.

"By continuously tracking and alerting you to changes in the financial health of every company in your supply chain, you can stay ahead of emerging risks." – CreditRiskMonitor

Timeliness is key. In 2025, corporate bankruptcies in the U.S. surged to over 22,000 filings – 18% higher than the 10-year average of 18,700. With bankruptcy filings reaching an 11-year high by Q3 2025, insurers need tools that can quickly identify worsening conditions. These systems analyze credit metrics and monitor credit migration, ensuring that deteriorating creditworthiness is detected and addressed without delay.

In addition to internal performance data, insurers incorporate external information such as market trends, industry developments, and public records. This blend of internal and external insights provides a well-rounded view of evolving risks.

By maintaining continuous monitoring, insurers can conduct timely reviews and ensure that policy terms remain appropriate as risks change.

Policy Reviews and Renewals

Formal policy reviews are typically conducted annually, during renewals, or whenever risk indicators arise. These evaluations take a comprehensive look at loan quality, documentation, and the overall performance of the portfolio.

"An effective credit risk review system provides for review and evaluation of an institution’s significant loans, loan products, or groups of loans typically annually, on renewal, or more frequently when internal or external factors indicate a potential for deteriorating credit quality." – Federal Reserve Regulatory Service

Periodic reviews often focus on higher-value loans, accounts flagged for elevated risk (such as those with low credit scores), or sectors experiencing rapid growth. Watch lists are used to track accounts showing early signs of trouble, even if they currently hold a "pass" rating. If new, material information comes to light – such as unpaid taxes, insurance lapses, or defaults – credit ratings are updated immediately, bypassing the usual annual review cycle.

At Accounts Receivable Insurance, this proactive monitoring ensures that policy terms reflect the latest conditions. Credit limits are adjusted in real-time, balancing protection for cash flow with appropriate coverage for dependable buyers. Additionally, quarterly reports to senior management and boards help insurers respond swiftly to evolving risk trends.

Conclusion

Gaining a clear understanding of how insurers assess risk can help you strengthen your financial standing. The process – from gathering data to continuous monitoring – highlights critical factors like on-time payments, a diverse customer base, and essential financial metrics. These elements play a key role in reducing delinquency and default rates, which insurers heavily weigh when determining risk scores and premium costs.

"Proactive credit risk prevention is your first line of defense. Remember, every invoice has the potential to become a bad debt." – ariglobal.com

In the United States, around 28 million businesses depend on trade credit to keep their operations running smoothly. Maintaining solid credit practices not only protects your business but also signals financial responsibility to insurers and lenders alike.

To secure better insurance terms, it’s important to regularly monitor key ratios like debt-to-income and interest coverage. Establish formal credit policies within your organization to demonstrate a structured approach to managing financial exposure. Keep open lines of communication with creditors and provide up-to-date financial statements, especially when approaching policy renewals. Leveraging AI tools can also enhance the accuracy of your risk assessments.

This proactive approach aligns with broader industry expectations.

"By measuring and reporting its credit risk performance and practices, an organization can demonstrate its compliance with regulatory requirements, its adherence to ethical principles, and its commitment to social responsibility." – FasterCapital

FAQs

How do the ‘5 Cs of Credit’ influence credit limit decisions?

The ‘5 Cs of Credit’ – Character, Capacity, Capital, Collateral, and Conditions – serve as a critical framework for insurers and lenders when determining credit limits. These factors work together to assess both the borrower’s financial situation and their reliability, ensuring decisions are grounded in a balanced evaluation.

Here’s a quick breakdown:

- Character speaks to the borrower’s trustworthiness and reputation, often gauged through credit history or references.

- Capacity focuses on the borrower’s ability to repay, based on their income and existing financial obligations.

- Capital examines the borrower’s financial reserves or net worth, which can act as a buffer in challenging times.

- Collateral looks at assets the borrower can offer as security, reducing risk for the lender.

- Conditions consider external influences like the state of the economy or specific industry trends that might impact repayment ability.

By carefully weighing these elements, insurers and lenders can establish credit limits that match the borrower’s risk profile, safeguarding cash flow and reducing the likelihood of financial losses.

How do insurers use AI tools to evaluate credit risk?

AI tools are changing the game for insurers by making credit risk evaluation faster and more precise. Using advanced technologies like machine learning and predictive analytics, these tools sift through vast amounts of financial and behavioral data to uncover actionable insights. They can perform real-time credit scoring, flag potential defaults, and offer early warning signals, empowering insurers to make well-informed decisions.

By integrating AI into credit assessment, insurers can improve accuracy, cut down the chances of bad debt, and simplify their workflows. These tools also support dynamic risk adjustments and ensure consistent criteria application, helping insurers manage their portfolios more effectively while minimizing financial risks. In short, AI is reshaping how credit risk is evaluated, delivering smarter and more dependable results.

What steps can businesses take to improve their credit risk scores and qualify for better insurance terms?

Businesses can improve their credit risk scores and unlock better insurance options by practicing solid financial management. This starts with paying bills on time, keeping outstanding balances low, and steering clear of unnecessary debt. These habits signal reliability and help establish a strong credit profile – something insurers often prioritize when evaluating risk.

Another important step is to regularly check credit reports for errors and address any inaccuracies promptly. A clean, accurate credit history not only reflects financial stability but also demonstrates transparency, both of which can positively impact risk assessments. By staying on top of credit management, businesses can reduce their perceived risk, opening the door to more competitive insurance terms and broader coverage options.