Cross-border credit insurance, also known as Export Credit Insurance (ECI), helps U.S. exporters manage the risk of foreign buyers failing to pay. It shields businesses from losses caused by buyer insolvency, political disruptions, or payment delays. Coverage typically ranges from 80% to 95% of the invoice value, with some policies offering up to 95% without deductibles. Here’s what you need to know:

- Compliance: Regulations vary by region. In the U.S., state-level licensing applies, while the EU uses the "single passport" system for insurers. Documentation, like invoices and bills of lading, must be accurate to avoid claim denial.

- Risks Covered: Includes commercial risks (e.g., buyer bankruptcy) and political risks (e.g., war or currency restrictions). Exclusions include fraud, product disputes, and pre-existing financial issues.

- Benefits: Insured receivables can serve as collateral for working capital loans, improving financial flexibility. Premiums are typically less than 1% of insured sales.

- Policy Management: Assign a dedicated policy owner, follow reporting deadlines, and regularly review coverage to ensure it meets your business needs.

Properly managed credit insurance not only reduces financial risks but also supports global trade confidence. Partnering with experienced brokers simplifies the process and ensures compliance with international regulations.

Credit Insurance as a Risk Mitigation Tool for International Trade

sbb-itb-2d170b0

Compliance Requirements for Cross-Border Credit Insurance

Understanding the compliance landscape for cross-border credit insurance means grappling with a mix of international frameworks and localized rules. Here’s a breakdown of the key areas, including regulations, licensing, and documentation.

Regulatory Frameworks Explained

Cross-border credit insurance operates under a web of regulations that differ widely by region. In the U.S., insurance laws are handled at the state level. This means foreign insurers must meet individual state licensing requirements if they engage with businesses or individuals within that state. As a result, compliance can vary significantly depending on the jurisdiction.

In contrast, the European Union employs the "single passport" principle. This allows insurers authorized in one EEA member state to operate across the EU without needing additional local approvals. However, this advantage doesn’t apply to non-EU insurers, including those from the UK post-Brexit. These insurers often need specific local authorization and may even be required to establish a physical branch to operate within the EEA.

Location also plays a critical role in compliance. For example, Canadian insurers are considered to be "carrying on business" in Ontario if they market products, solicit insurance, or collect premiums in the province – even without a physical office. This triggers licensing requirements that could restrict coverage options.

These regional differences underline the importance of understanding the specific licensing and operational rules for each market.

Licensing and Local Presence Requirements

Whether an insurer needs a local presence depends largely on the jurisdiction. Within the EU, insurers can operate under "freedom of services" (no physical branch required) or "freedom of establishment" (simplified branch setup). For instance, Croatia had 537 non-Croatian EU insurers offering cross-border services, compared to just 14 domestic providers.

Capital requirements are another factor. Under Solvency II, the Minimum Capital Requirement (MCR) for non-life insurers is set at €2.7 million, or €3.4 million if liability risks are included. In the UK, the Prudential Regulation Authority expects third-country branches with over £500 million in insurance liabilities covered by the Financial Services Compensation Scheme to establish a local subsidiary.

For U.S. exporters using government-backed programs like UK Export Finance (UKEF), an additional hurdle exists: businesses must typically have an established presence in the insurer’s country, such as the UK, Isle of Man, or Channel Islands.

Once licensing and local presence are in place, insurers must also adhere to detailed reporting and documentation requirements.

Reporting and Documentation Standards

Proper documentation is a cornerstone of cross-border credit insurance. Standard commercial paperwork – like invoices, bills of lading, packing lists, and certificates of origin – must be accurate and consistent. Any discrepancies in descriptions, quantities, or consignee details among these documents can lead to claim denial.

Notification deadlines are equally critical. Policyholders must inform insurers of potential losses within 15 business days and report payment failures within 30 days of the due date. Missing these deadlines can void coverage, so it’s wise to assign someone on your credit team to oversee compliance tasks, including limit requests, overdue reporting, and stop-shipment protocols.

Additionally, all transactions are subject to Know Your Customer (KYC), Anti-Money Laundering (AML), and sanctions screening. Sales to sanctioned parties cannot be insured, and insurers often require buyer financial statements, credit reports, and a detailed sales history. Coverage is strictly tied to credit risks linked directly to the delivery of goods or services. Without this connection, the amount is not insurable. Regulations also typically exclude coverage for financial guarantees, reverse factoring, or government buyers unless specific political risks are involved.

"The insurer shall have a comprehensive ‘Claims Manual’ which gives the manner in which the claims shall be processed, documentation, delegation of authority, policy holders servicing, grievance redressal etc."

- IRDAI (Trade Credit Insurance) Guidelines, 2021

To support potential claims, maintain a complete claims pack that includes purchase orders, invoices, bills of lading, delivery notes, and all correspondence related to debt collection. In India, insurers are required to report any loss exceeding 1% of their net worth to the regulatory authority (IRDAI), highlighting the intense scrutiny these policies face worldwide.

Risks Covered and Excluded in Cross-Border Credit Insurance

Now that we’ve discussed compliance standards, it’s equally important to dive into the types of risks cross-border credit insurance covers – and those it doesn’t.

Covered Risks

Cross-border credit insurance is designed to shield businesses from both commercial and political risks. On the commercial side, policies typically cover situations like nonpayment due to buyer insolvency, formal bankruptcy, or extended payment delays – usually between 60 and 180 days past due. Coverage often ranges from 80% to 95% of the invoice value, with some EXIM Bank small business policies offering up to 95% coverage without a deductible.

Political risks, on the other hand, include events that neither party can control. These might involve war, terrorism, civil unrest, sudden regulatory changes, currency restrictions, or government actions that disrupt payments or contracts. For instance, if a foreign government enforces export restrictions or blocks currency transfers, the political risk portion of your policy may step in. For sovereign buyers, these risks are often covered at 100%.

"Political risk is an event or situation that is outside you or your buyer’s control and obstructs the payment or delivery of goods." – Lawrie Insurance Group

It’s important to note that coverage applies only to risks tied directly to the delivery of goods or services. If a loss occurs outside of these transactions, it won’t be covered. Once a claim is validated and paid – usually within 30 days – the insurer typically takes over the debt recovery process through subrogation.

While these policies provide extensive protection, they do have clear exclusions, which are explained below.

Common Exclusions

One key exclusion is fraud. Credit insurance is meant to cover legitimate nonpayment events, such as bankruptcy or default. This means businesses must have strong fraud prevention measures and robust know-your-customer (KYC) protocols in place.

"Fraudulent transactions are excluded. Insurance covers legitimate nonpayment events like bankruptcy and default. Strong fraud prevention measures are still required." – Kirk Elken, Co-founder, Securitas Global Risk Solutions

Another exclusion involves disputes over product quality or quantity. For example, if a buyer refuses to pay because they claim goods were defective or short-shipped, the insurer won’t cover the loss until the dispute is resolved. Likewise, amounts beyond approved credit limits are excluded, as insurers cap their exposure to minimize potential losses. Shipments made in violation of policy terms – like shipping after a stop-shipment notice – will also void coverage for those shipments.

For political risks, coverage may be denied if the buyer fails to deposit local currency within a specified period, such as three months from the invoice due date. Similarly, pre-existing financial issues identified during underwriting are not covered.

Understanding these exclusions is critical for U.S. exporters to ensure their policies align with both industry regulations and their specific business needs.

| Risk Category | Common Exclusions | Reason for Exclusion |

|---|---|---|

| Commercial | Fraud / Criminal Activity | Not a legitimate commercial default; requires internal controls |

| Commercial | Disputes / Non-trade debts | Risks must directly link to delivery of goods/services |

| Commercial | Amounts over credit limits | Insurers limit exposure to prevent foreseeable losses |

| Political | Currency claims without local deposit | Specific policy requirements for valid political risk claims |

| General | Pre-existing financial problems | Underwriting excludes known high-risk or insolvent buyers |

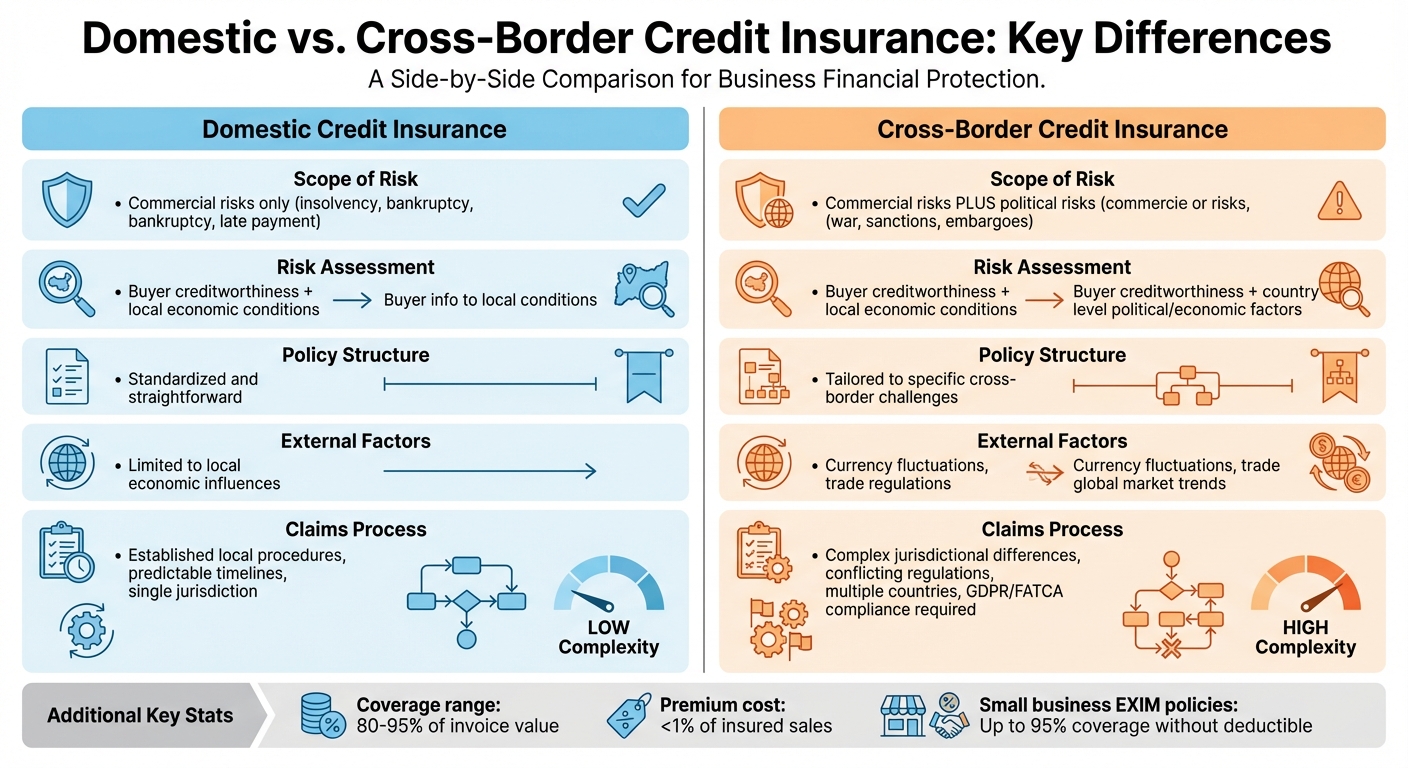

Domestic vs. Cross-Border Credit Insurance Policies

Domestic vs Cross-Border Credit Insurance: Key Differences Comparison

Choosing between domestic and cross-border credit insurance policies requires a clear understanding of their differences. These policies both protect against nonpayment risks, but they vary in terms of scope, complexity, and cost. These distinctions influence everything from coverage to claims processes, making it essential to evaluate which type aligns with your business needs.

Coverage Scope Differences

Domestic credit insurance focuses on commercial risks like buyer insolvency, bankruptcy, or prolonged nonpayment. These policies are typically simpler, with standardized terms and lower premiums. Risk assessments are based on the buyer’s creditworthiness within the context of local economic conditions.

Cross-border credit insurance, on the other hand, includes coverage for political risks such as war, sanctions, or embargoes. Insurers evaluate not only the buyer’s financial stability but also the broader economic and political environment of their country. Pricing for these policies is more variable – it depends on whether you’re insuring specific transactions or your entire sales portfolio. While the cost is generally a small fraction of your company’s sales profits, additional factors like currency devaluation, exchange rate volatility, and international trade regulations can influence premium rates. Unlike domestic policies, cross-border policies must navigate a more dynamic and unpredictable regulatory and currency landscape.

Claims Processes and Challenges

The claims process is another area where domestic and cross-border policies diverge significantly.

Domestic claims are relatively straightforward, operating within a single jurisdiction with clear legal and collection procedures. Timelines are predictable, and the process is governed by established protocols.

Cross-border claims, however, can be far more complex. Jurisdictional differences often lead to complications, especially if the policy lacks clear "choice of law" or "forum selection" clauses. This can result in simultaneous legal disputes in multiple countries. Each jurisdiction may impose unique time limits, documentation standards, and regulatory requirements, which can conflict with the insurer’s protocols. Noncompliance with local regulations – such as GDPR in the EU, FATCA in the U.S., or OSFI standards in Canada – can delay or invalidate claims. Sharing sensitive financial or customer data across borders adds another layer of risk, as improper consent documentation can lead to legal penalties. Even standard terms in contracts may be interpreted differently depending on the country, with local laws sometimes overriding the agreed terms.

| Feature | Domestic Credit Insurance | Cross-Border Credit Insurance |

|---|---|---|

| Scope of Risk | Covers commercial risks like insolvency and late payment | Includes commercial risks plus political risks such as sanctions or war |

| Risk Assessment | Focuses on buyer creditworthiness within local conditions | Considers buyer creditworthiness and country-level political and economic factors |

| Policy Structure | Standardized and straightforward | Tailored to address specific cross-border challenges |

| External Factors | Limited to local economic influences | Impacted by currency fluctuations, trade regulations, and global market trends |

| Claims Challenges | Follows established local procedures | Complicated by jurisdictional differences and conflicting regulations |

Understanding these differences is key to determining the right policy for your business, especially when navigating the complexities of international trade.

How to Secure Cross-Border Credit Insurance

To secure cross-border credit insurance, you’ll need to carefully evaluate your business risks, work with experienced professionals, and ensure proper management throughout the policy’s lifecycle.

Assessing Your Business Needs and Risks

Start by analyzing the financial stability of your international buyers. Insurers provide ratings and credit reports that can help you gauge the risks tied to your largest trade partners. These insights reveal how underwriters perceive your exposure, giving you a clearer picture of potential vulnerabilities.

It’s also essential to review your international sales contracts and payment terms. Non-compliance with insurance standards could result in claim denials down the line. Decide whether cancelable or non-cancelable credit limits suit your business better. Non-cancelable limits are particularly attractive because they guarantee coverage throughout the policy term, even if a buyer’s financial situation worsens. Additionally, consider whether the policy aligns with internal management standards or could enhance your access to bank financing and working capital. Keep in mind that most export credit insurance policies typically cover about 90% of the amount owed in cases of buyer insolvency or default.

This evaluation provides the foundation for selecting the right broker and structuring a policy that fits your needs.

Working with Specialized Providers

After assessing your risks, collaborate with specialized providers to customize your coverage. Partnering with an experienced broker gives you access to a wide range of underwriters through a single application.

"The insured is often surprised in the variation of terms and underwriting results from carrier to carrier"

- Kirk Elken, Co-founder, Securitas Global Risk Solutions

A skilled broker not only compares terms but also ensures your policy meets the regulatory requirements in each market.

For instance, providers like Accounts Receivable Insurance focus on tailoring policies to your specific needs. They assist with policy design, risk evaluations, and connecting you to a global network of credit insurance carriers. They also advocate for you during negotiations with underwriters. To streamline the process, prepare documentation such as purchase orders, invoices, bills of lading, and proof of delivery ahead of time. These documents are crucial for both underwriting and any future claims.

Managing Your Policy Over Time

Assign a dedicated policy owner to handle tasks like limit requests, overdue account reporting, and claims documentation. Regularly review the policy – ideally once a year – to ensure it still aligns with your business needs and covers the right debtors. Also, verify that your sales terms comply with the policy’s requirements.

Start the renewal process 60 to 90 days before the policy expires. This gives you enough time to reassess market trends and adjust coverage as needed. Stay on top of overdue accounts by following notice rules and enforcing "stop shipment" orders when delays exceed the allowed timeframe. Claims should be filed within 180 days from the invoice date to avoid complications.

Many insurers offer online tools to help you monitor the financial health and risk ratings of your international customers in real time. These platforms can be invaluable for proactive policy management.

"A well-structured policy, backed by active management and strong advocacy, helps ensure you get the coverage you need when it matters most"

- Kirk Elken, Co-founder, Securitas Global Risk Solutions

Conclusion

Cross-border credit insurance goes beyond simply protecting receivables – it serves as a cornerstone for building confidence in international trade. By adhering to regulatory requirements and maintaining accurate documentation, businesses can ensure their claims are eligible, with policies often covering 80–90% of qualifying receivables.

But the benefits don’t stop at claim payouts. Insured receivables can enhance borrowing power and provide access to valuable insights on over 250 million companies worldwide. And with premiums typically costing less than 1% of insured sales, it’s a cost-effective way to safeguard your global operations.

"In many cases, a single claim can offset years of premium costs."

- Kirk Elken, Co-founder, Securitas Global Risk Solutions

However, success with cross-border credit insurance requires more than just purchasing a policy. It demands active engagement – monitoring buyer creditworthiness, meeting reporting obligations, and managing coverage effectively. Partnering with experts like Accounts Receivable Insurance can simplify the process, offering customized policy solutions, in-depth risk evaluations, and access to a worldwide network of carriers with expertise in international trade.

Whether you’re entering new markets or securing existing ones, a well-managed credit insurance strategy equips you to trade with confidence while reducing financial risks.

FAQs

Do I need my insurer to be licensed in my state?

Yes, it’s typically a good idea to make sure your insurer is licensed in your state. This ensures they comply with local laws and regulations, which can make handling claims and receiving support much smoother. That said, the exact requirements can vary depending on your state’s rules and the insurer’s specific practices.

What documents do I need to avoid a denied claim?

To avoid having your claim denied, make sure all your documentation is accurate and complete. This includes items like invoices, bills of lading, export licenses, and proof of export. Additionally, claims need to be submitted within the timeframe outlined in your policy – usually within 180 days from the invoice date. Carefully review your policy requirements to ensure you’re meeting all the necessary conditions.

Can my insured receivables help me get a bank loan?

Insured receivables can play a key role in securing a bank loan. By serving as collateral, they reduce the lender’s risk, which often leads to better terms, such as higher advance rates. This can open up more financing opportunities, making it simpler to access the funds necessary for your business.