Managing credit risk has evolved. Traditional methods like financial statements and credit reports focus on historical data but often miss current and emerging risks. Credit insurance analytics, powered by AI and real-time data, predict risks months in advance, offering faster, more accurate insights.

Key Points:

- Traditional Tools: Use past data (financial statements, trade references) but are slow and limited in scope.

- Credit Insurance Analytics: Leverage AI, alternative data (B2B transactions, cybersecurity), and real-time monitoring for predictive risk assessment.

- Comparison: Analytics are faster (30 minutes vs. 3–5 days), more accurate, and better at detecting early warning signs, especially for private companies.

Quick Comparison:

| Feature | Traditional Tools | Credit Insurance Analytics |

|---|---|---|

| Data Sources | Historical financials, trade references | Real-time B2B data, AI, news sentiment |

| Speed | 3–5 business days | 90% approvals in 30 minutes |

| Risk Monitoring | Periodic (monthly/quarterly) | Continuous, real-time |

| Coverage | Public companies, limited SMEs | Private firms, SMEs, global data |

| Early Warning | Reactive | Predictive (6–8 months ahead) |

For the best results, combine both approaches: use traditional tools for baseline creditworthiness and analytics for early risk detection and dynamic insights.

Benefits of Credit Monitoring Tools I Moody’s Analytics Pulse I Explainer Video

sbb-itb-2d170b0

How Traditional Risk Tools Work

Traditional credit risk tools rely on a structured, methodical approach grounded in the 5 Cs framework. Instead of forecasting future trends, these tools focus on analyzing past performance using established financial metrics and manual processes.

Historical Financial Data Analysis

At the heart of traditional risk assessment is the review of historical financial statements, such as balance sheets, income statements, and cash flow statements. Analysts calculate key ratios, including debt-to-equity, current ratio, and debt service coverage ratio, all of which provide a snapshot of past financial performance.

"Traditional credit risk analysis primarily relies on historical financial statements and past performance. This backward-looking perspective is a major limitation." – Emagia Staff

To add another layer of verification, trade references from banks and suppliers are often included. However, these references are typically selective, highlighting only on-time payments while leaving out details of poor payment histories. This selective reporting creates gaps in the overall risk evaluation process.

Manual Processing and Rule-Based Systems

Traditional methods are heavily manual and time-intensive. Analysts spend hours collecting documents, verifying data, and calculating financial ratios, often using spreadsheets or basic rule-based systems. These systems assign scores based on a narrow set of financial data and fixed rules, which makes them inflexible to economic changes or shifts in borrower behavior.

Qualitative assessments, such as evaluating management quality or market position, add another layer of complexity. These evaluations can vary widely depending on the analyst, leading to inconsistencies. As the volume of loans or invoices grows, these manual processes often result in bottlenecks, slowing down the decision-making process and driving up costs. This lack of efficiency makes it difficult to respond swiftly to market fluctuations.

Challenges with Real-Time Updates

One of the biggest hurdles for traditional tools is their inability to provide timely insights. The process of gathering and analyzing certified financial statements can take so long that the data is often outdated by the time a credit decision is made. Portfolio monitoring is typically limited to periodic reviews or manual alerts, which means early warning signs of financial distress are often missed until it’s too late.

"Traditional credit analysis often falls short because it relies heavily on past financial performance and public information. This approach can miss critical indicators of a company’s future financial health." – Moody’s

Additionally, these tools struggle to quickly adapt to sudden market shocks, geopolitical events, or real-time developments that could immediately impact a borrower’s ability to repay. They also face significant limitations in processing alternative data sources, such as social media sentiment, real-time payment patterns, or detailed transaction histories. For private companies, these challenges result in major blind spots, underscoring the need for more agile, real-time risk assessment tools.

How Credit Insurance Analytics Work

Credit insurance analytics have redefined how businesses evaluate risk by incorporating AI-driven algorithms and real-time data streams into their processes. Unlike traditional tools that rely solely on past performance, these platforms predict future risks with greater precision. By merging vast global datasets with machine learning, they provide quicker and more accurate evaluations of buyer creditworthiness. This modern approach has paved the way for advanced predictive models and the integration of alternative data sources.

Predictive Models and Alternative Data Sources

Gone are the days of relying exclusively on annual financial statements. With predictive models, today’s analytics platforms can forecast a company’s solvency and risk of default over a 12-month period. These systems pull from alternative data sources that traditional tools overlook, such as B2B transaction records, digital spending behaviors, cybersecurity vulnerabilities, and even real-time news sentiment.

This capability is especially beneficial when assessing private companies, which often do not release financial statements. Algorithms can detect early warning signs that manual reviews might miss entirely. For instance, a company’s cybersecurity posture now serves as an indicator of corporate governance – weak digital security often correlates with financial instability.

"By combining our world-class expertise with the wealth of our global data assets and the power of cutting-edge technologies (artificial intelligence, data science), our clients benefit from more intelligent solutions that inform their decisions and enable them to manage commercial risks in a more predictive way." – Guillaume Huguet, Data Lab Director, Coface

These predictive tools seamlessly integrate with systems designed for continuous, real-time monitoring of financial health.

Real-Time Automated Risk Monitoring

Traditional periodic reviews have been replaced by automated monitoring systems that offer round-the-clock oversight of buyer financial health. By incorporating B2B transaction data and spending patterns, these platforms capture up-to-the-minute behavioral insights. For example, they can analyze financial ratios in real time across a database of over 5 million financial statements, identifying anomalies or potential opportunities.

Real-time news feeds and algorithmic scoring further enhance these systems, automatically flagging high-risk companies. This dynamic approach ensures that businesses are alerted to potential issues early, allowing them to adjust credit terms or reduce coverage before losses occur, rather than reacting after a missed payment.

Access to Global Credit Data Networks

Modern analytics platforms leverage global data networks that provide insights into more than 600 million pre-scored companies worldwide. These networks are particularly useful for understanding private companies and SMEs that traditional credit agencies often overlook. They cover a wide range of industries and geographic locations, offering a standardized view of risks.

This global perspective is invaluable for businesses engaged in international trade. These platforms account for factors like currency fluctuations, trade sanctions, and political instability – risks that local tools might miss. By combining traditional financial data with emerging risks such as cyber threats and geopolitical changes, these networks provide businesses with a comprehensive risk assessment. Accounts Receivable Insurance utilizes this global network to deliver tailored coverage for both domestic and international markets, ensuring businesses have the insights they need to navigate complex trade environments.

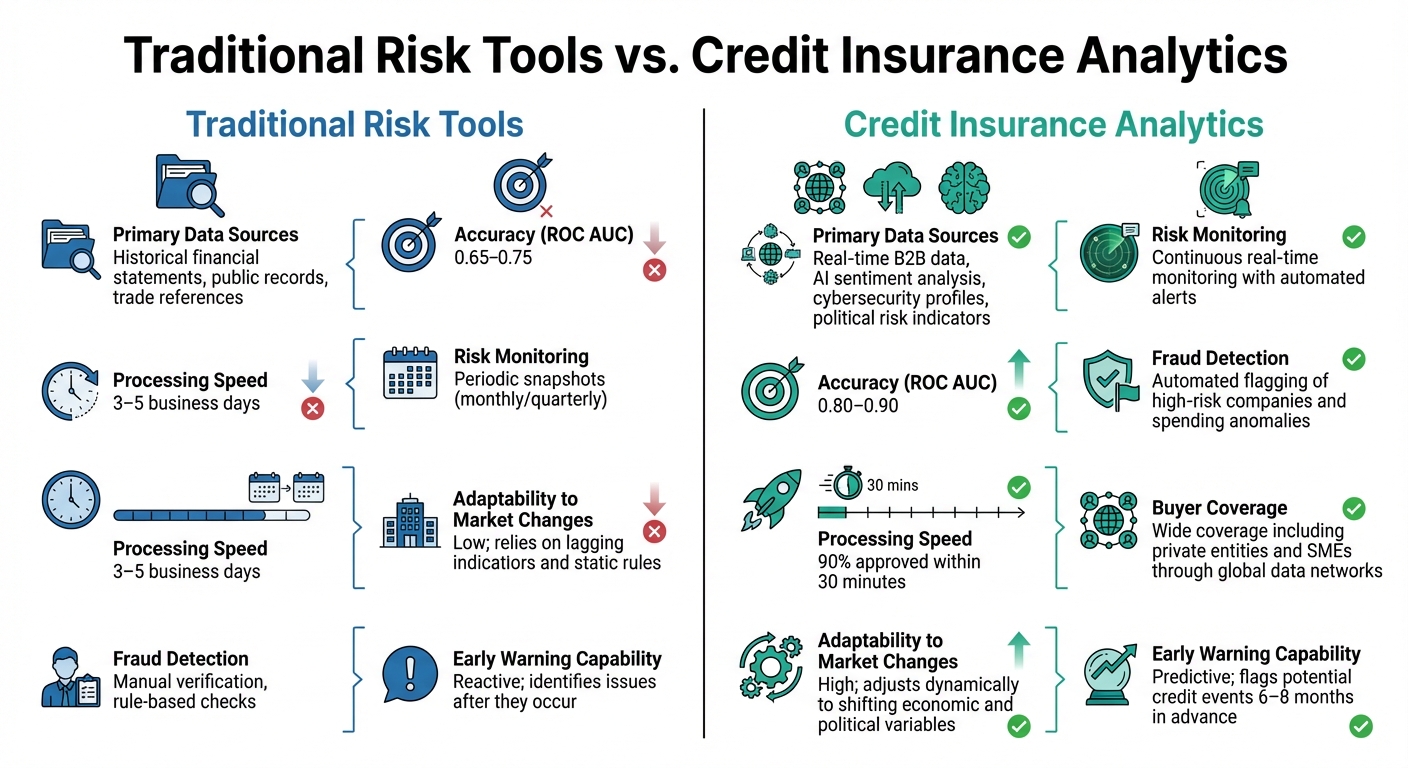

Direct Comparison: Traditional Risk Tools vs. Credit Insurance Analytics

Traditional Risk Tools vs Credit Insurance Analytics Comparison

When you place these two approaches side-by-side, the differences become clear. Traditional risk tools rely on historical snapshots – examining financial statements, trade references, and public records that might be months or even years old. On the other hand, credit insurance analytics leverage real-time data and AI to predict risks rather than simply recount past performance.

Take credit limit approvals as an example. Traditional methods often require 3–5 business days for manual underwriting. In contrast, analytics platforms can process 90% of approvals in just 30 minutes, significantly speeding up decision-making and cutting operational costs.

Another key distinction lies in buyer coverage. Traditional tools often fall short when assessing private companies or small and medium-sized enterprises (SMEs) that lack public financial data or credit histories. Credit insurance analytics overcome this limitation by incorporating alternative data sources like B2B transaction patterns, cybersecurity ratings, and even news sentiment. This broader perspective allows them to evaluate entities that traditional methods simply can’t.

Comparison Table

| Metric | Traditional Risk Tools | Credit Insurance Analytics |

|---|---|---|

| Primary Data Sources | Historical financial statements, public records, trade references | Real-time B2B data, AI sentiment analysis, cybersecurity profiles, political risk indicators |

| Accuracy (ROC AUC) | 0.65–0.75 | 0.80–0.90 |

| Processing Speed | 3–5 business days | 90% approved within 30 minutes |

| Risk Monitoring | Periodic snapshots (monthly/quarterly) | Continuous real-time monitoring with automated alerts |

| Fraud Detection | Manual verification, rule-based checks | Automated flagging of high-risk companies and spending anomalies |

| Buyer Coverage | Limited to firms with public data or references | Wide coverage including private entities and SMEs through global data networks |

| Adaptability to Market Changes | Low; relies on lagging indicators and static rules | High; adjusts dynamically to shifting economic and political variables |

| Early Warning Capability | Reactive; identifies issues after they occur | Predictive; flags potential credit events 6–8 months in advance |

These differences highlight how real-time analytics have reshaped risk assessment. Credit insurance analytics consistently outperform traditional tools, especially in areas like fraud detection. Automated systems can quickly spot irregularities in B2B transactions that manual reviews might overlook. Plus, by predicting potential credit events 6–8 months ahead, these tools allow businesses to take proactive steps – whether that means adjusting terms, reducing exposure, or finding alternative solutions.

Why Credit Insurance Analytics Outperform Traditional Tools

Better Accuracy and Earlier Fraud Detection

Credit insurance analytics can identify emerging risks as much as 6–8 months in advance, giving businesses the chance to act before these risks impact financial performance. Automated fraud detection tools analyze thousands of data points at once, flagging unusual patterns in B2B transactions and spending that manual reviews would miss. Interestingly, a company’s cybersecurity posture has become a key indicator of risk – companies with weak security measures often exhibit poor governance, which can increase the likelihood of financial instability.

Broader Buyer Coverage Through Alternative Data

Unlike traditional underwriting methods, credit insurance analytics rely on alternative data sources, such as B2B payment trends and real-time news sentiment, to evaluate risk. This approach is particularly useful for assessing private companies and small-to-medium enterprises (SMEs) that don’t disclose public financial information. Traditional methods often depend on trade references provided by buyers, which are typically handpicked to showcase on-time payments. In contrast, credit insurers analyze millions of buyer relationships and transactions within their global networks. This wealth of data paints a much clearer picture of payment behavior across industries and regions, enabling more informed and effective trade credit strategies.

Practical Applications in Trade Credit Management

These analytics-driven insights bring tangible benefits. For example, in April 2025, a multinational chemical supplier managed to cut default losses in emerging markets by 20% by integrating real-time market intelligence with tailored credit analytics.

For businesses looking to manage accounts receivable risk, services like Accounts Receivable Insurance apply these advanced analytics to create customized policies and risk assessments. By partnering with global credit insurance carriers, businesses can access the same predictive models and alternative data sources used by major insurers. This allows companies to tailor coverage to their specific buyer portfolios, whether they’re dealing with domestic clients or international markets. Analytics also make it easier to segment risk, enabling businesses to prioritize insurance coverage for higher-risk transactions while offering more flexible terms to lower-risk buyers.

Limitations and How to Combine Both Approaches

Data Privacy and Implementation Concerns

Using AI and machine learning in risk management comes with its own set of challenges. These technologies rely on large datasets and specialized expertise, which can be expensive and take time to implement. Adding real-time B2B data into the mix increases the risk of privacy breaches and requires strong cybersecurity measures. There’s also the risk of missteps when acting on predictive analytics. For example, Moody’s highlights that withdrawing insurance coverage based on analytics could backfire if suppliers insist on advance payments for deliveries, potentially triggering claims. This creates a tricky situation where being too aggressive with analytics might inadvertently lead to defaults. Even as we navigate these modern hurdles, traditional risk tools remain a cornerstone for financial benchmarks.

Where Traditional Tools Still Matter

Traditional risk tools continue to play a vital role, offering insights that analytics alone cannot fully replace. Tools like financial statement analysis and credit reports provide the baseline creditworthiness data that regulators and compliance teams depend on. These methods also offer a clear, documented trail that aligns with industry standards. Key metrics such as Loss Given Default (LGD), which evaluates collateral value, and Exposure at Default (EAD), which measures the actual dollar amount at risk, are critical for regulatory compliance. These assessments form the backbone of consistent risk management protocols across organizations.

Using Both Methods Together

The best results come from blending traditional methods with modern analytics. Traditional tools establish a reliable baseline for assessing risk, while AI-driven analytics add a proactive layer to identify early warning signs and emerging threats. Start with standard credit scores and financial ratios, then enhance these insights with real-time data on cash flow, cybersecurity risks, and B2B payment trends. When analytics highlight increased risk, Moody’s advises a cautious, collaborative approach: "Trade credit insurers often navigate risk reduction with caution, phasing out coverage in close collaboration with the key suppliers and buyers involved". This careful strategy avoids sudden disruptions while still acting on predictive insights.

Accounts Receivable Insurance exemplifies this integrated approach. It combines traditional underwriting standards with access to global credit data networks, enabling businesses to leverage the reliability of established methods alongside advanced risk detection capabilities.

Conclusion: Selecting the Right Method for Your Business

Choosing the right mix of methods is essential for managing credit risk effectively. It’s not about picking between analytics and traditional tools but rather understanding how they complement each other. Traditional tools, like financial statements and credit reports, offer the regulatory documentation needed to establish baseline creditworthiness. On the other hand, analytics-driven solutions bring predictive insights, helping businesses identify risks earlier. The challenge lies in tailoring the combination to your unique needs.

For businesses with annual revenues exceeding $5 million, credit insurance analytics can be a game-changer. These tools often cover up to 90% of unpaid invoice values, with premiums ranging between 0.1% and 0.4% of the invoice value – significantly lower than the up-to-2% cost associated with Letters of Credit. Companies engaged in international trade or those with limited public data benefit greatly from analytics that evaluate B2B transaction patterns and provide real-time monitoring.

While analytics emphasize speed and predictive accuracy, traditional tools remain critical for their ability to provide financial benchmarks. For example, firms with strong financial reserves capable of self-insuring, or those handling high-value single transactions, may lean on traditional methods like bank guarantees for focused protection. However, relying solely on historical data or trade references can introduce biases and fail to account for emerging risks.

A well-rounded strategy integrates both approaches. Start with traditional credit scores and financial ratios to establish a foundation of stability. Then, enhance this with real-time insights into payment behaviors, industry trends, and geopolitical risks. For instance, Accounts Receivable Insurance showcases this hybrid model by blending established underwriting practices with global credit data networks, ensuring compliance while proactively identifying risks.

Key Takeaways

Balancing these methods can lead to stronger risk management strategies:

- Credit insurance analytics: These tools excel at early risk detection and provide broad portfolio coverage by leveraging AI and alternative data sources.

- Traditional methods: They offer the regulatory framework and audit trails required for compliance.

- Hybrid strategies: Combining both approaches allows businesses to establish dependable baselines with traditional tools while using analytics to spot emerging risks and opportunities.

- Tailored solutions: Companies engaged in global trade or working with private firms should prioritize analytics-backed methods, while those with stable, local clients and strong reserves may find traditional tools sufficient.

Most businesses find that combining these approaches delivers the best results for managing credit risk effectively.

FAQs

What data does credit insurance analytics use that traditional tools miss?

Credit insurance analytics tap into real-time data and alternative data sources that traditional tools often miss. These include factors like buyer behavior, financial health, payment trends, and even emerging risks such as cybersecurity issues and ESG (Environmental, Social, and Governance) ratings. By focusing on these dynamic insights, credit insurance analytics can spot signs of financial trouble early. In contrast, traditional tools rely heavily on historical data and fixed credit scores, which might not accurately capture current or evolving risks.

How can I combine traditional credit checks with real-time analytics?

To merge conventional credit checks with real-time analytics, leverage advanced tools that provide continuous monitoring of customer financial health. Traditional credit checks focus on static data, such as credit scores, offering a snapshot of creditworthiness. On the other hand, real-time analytics track ongoing data, like payment behavior and transaction trends, giving a more current picture of financial activity. By integrating these methods, businesses can better manage risk, optimize cash flow, and make quicker, more informed credit decisions by balancing a stable credit baseline with dynamic, real-time insights.

What are the biggest privacy and implementation risks with AI-based monitoring?

AI-based monitoring comes with several challenges, including data quality, transparency, and security. For these systems to work well, they need access to high-quality data, but maintaining that standard can be tough. Privacy is another big concern since these tools often handle sensitive financial and personal information, which raises the risk of data breaches.

There are also hurdles when it comes to implementation. These include pushback against adopting new systems, potential biases in algorithms, and difficulties in meeting regulatory requirements. To tackle these issues, it’s essential to have strong security protocols in place and ensure AI processes remain clear and open.