Coverage limits in trade credit insurance are the maximum amounts your insurer will pay if a customer fails to pay their debt. These limits protect your business by capping financial risks tied to specific buyers or your overall policy. Key points to know:

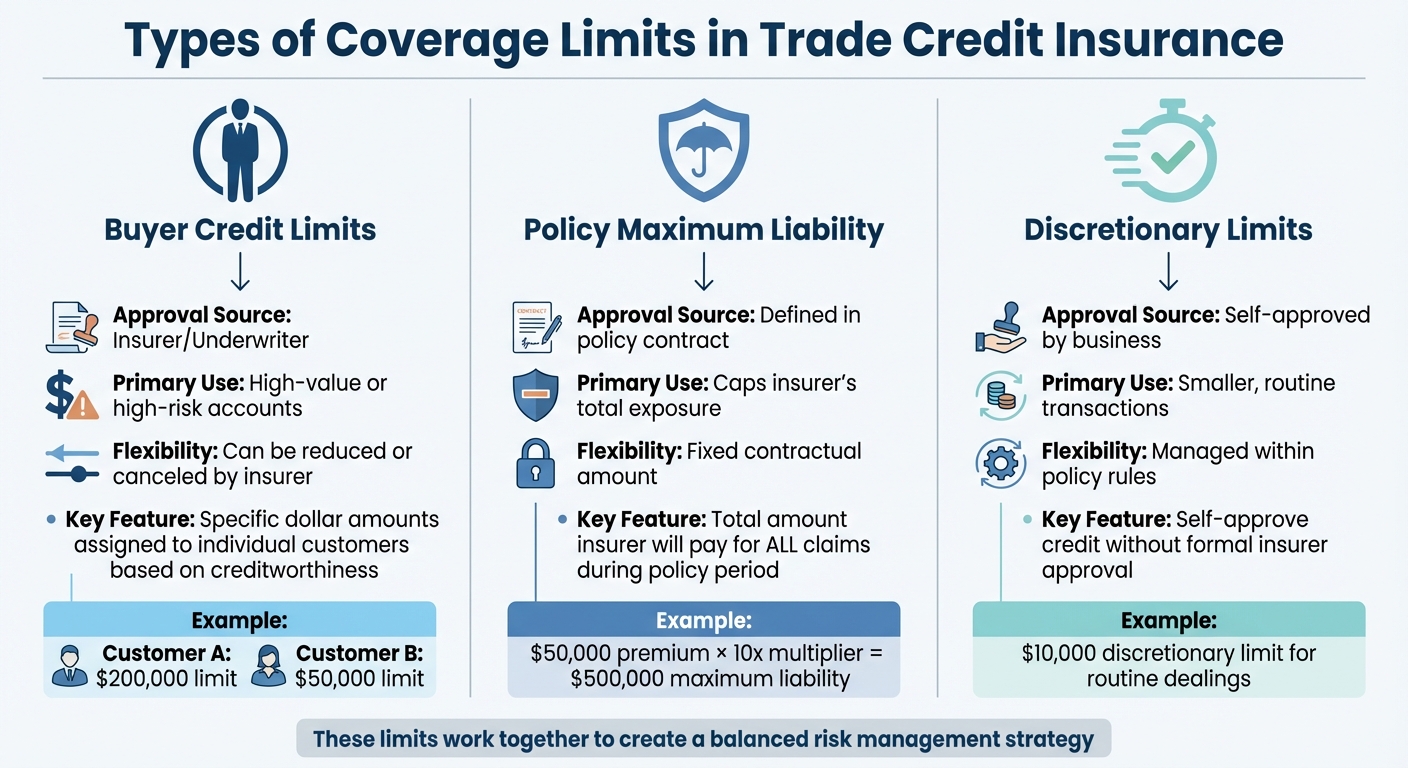

- Buyer Credit Limits: Specific limits for individual customers based on their creditworthiness.

- Policy Maximum Liability: The total amount your insurer will pay across all claims during the policy period.

- Discretionary Limits: Self-approved limits for smaller transactions, allowing quicker credit decisions.

Coverage typically reimburses 75%-95% of losses, leaving a small portion for you to manage. These limits are tailored to your business needs and adjusted over time based on customer risk, industry trends, and transaction details. Properly managing coverage limits not only reduces risk but also improves cash flow, financing options, and overall financial stability.

What is Trade Credit Insurance? | Credit Insurance explained in 5 minutes

sbb-itb-2d170b0

What Are Coverage Limits?

A coverage limit is the maximum amount your insurer will pay if a buyer fails to fulfill their payment obligations. Essentially, it sets a financial boundary on your protection. For instance, if a buyer owes you $500,000 but your coverage limit for that buyer is $300,000, the insurer will only cover up to $300,000 – not the entire debt owed.

These limits are specific to each buyer. Insurers assess the creditworthiness of individual customers and assign a unique limit to each one. This determines the maximum amount of coverage you’ll have for transactions with that buyer. For example, Customer A might have a $200,000 limit, while Customer B’s limit could be $50,000, depending on their financial stability. This tailored approach helps manage risk more effectively.

As ICISA explains:

"The granted credit limit… is the maximum insured cover for a specific buyer and the policyholders can trade on an insured basis within the approved credit limit throughout the policy period without further reference to the insurer".

This means you can conduct business confidently within those limits without needing to repeatedly consult your insurer.

Coverage limits help transfer risk by protecting you up to the specified amount if a buyer defaults, as long as a valid credit limit is in place at the time of the loss.

It’s important to note that insurers rarely cover the entire loss. Instead, they pay an indemnity percentage, which typically ranges from 75% to 95% of the outstanding debt. For example, if your coverage limit is $300,000 and your policy has an 85% indemnity rate, the maximum payout you’d receive is $255,000. This co-insurance model ensures that you share some responsibility when extending credit, encouraging prudent risk management.

Types of Coverage Limits

Types of Trade Credit Insurance Coverage Limits Comparison

Trade credit insurance policies typically include three main types of coverage limits. These limits work together to help manage your business’s exposure to customer non-payment, ensuring a balanced approach to risk.

Buyer Credit Limits

Buyer credit limits are specific dollar amounts assigned to individual customers based on their creditworthiness.

As Ari Global explains:

"A key service provided is that the insurance underwriter will assess each of the policyholder’s customers and set an approved credit limit on each. This represents the maximum amount of coverage for that buyer".

For example, if a customer typically has an outstanding balance of $150,000, the insurer might set a buyer credit limit at $120,000. If the customer defaults, the policy would cover up to that approved amount, subject to the agreed indemnity percentage. These limits can either be cancelable – allowing adjustments if the customer’s credit profile changes – or non-cancelable, staying fixed for the policy term.

In addition to individual buyer limits, policies also include an overall cap to manage total exposure.

Policy Maximum Liability

The policy maximum liability, also called the aggregate limit, is the total amount an insurer will pay for all claims during the policy period. Think of it as the insurer’s overall exposure ceiling.

ICISA explains:

"The maximum liability amount is used to limit the loss that can be sustained through one single policy, hence also called policy limit".

This limit is usually tied to your annual premium. For instance, if your premium is $50,000 and the policy applies a 10x multiplier, the maximum liability would be $500,000. Even if multiple customers default throughout the year, the insurer’s total payout will not exceed this cap.

While maximum liability sets a firm boundary, discretionary limits offer more flexibility for managing smaller accounts.

Discretionary Limits

Discretionary limits allow businesses to self-approve credit for smaller transactions without needing formal approval from the insurer. This simplifies routine dealings with lower-value customers.

For instance, a policy might include a $10,000 discretionary limit. This means you can extend credit up to that amount as long as you meet the policy’s documentation requirements, such as maintaining recent credit reports (valid for 12 months) or proof of timely payments on past invoices. Failing to meet these requirements could result in a denied claim under this limit.

ICISA highlights:

"If a discretionary limit has been agreed in the policy, exposures up to that amount do not have to be agreed by the trade credit insurer but are covered based on specific rules".

Here’s how the different limits compare:

| Limit Type | Approval Source | Primary Use | Flexibility |

|---|---|---|---|

| Buyer Credit Limit | Insurer/Underwriter | High-value or high-risk accounts | Can be reduced or canceled by insurer |

| Policy Maximum Liability | Defined in policy contract | Caps insurer’s total exposure | Fixed contractual amount |

| Discretionary Limit | Self-approved by business | Smaller, routine transactions | Managed within policy rules |

Each of these limits plays a role in creating a balanced risk management strategy, aligning with the principles of trade credit insurance to protect your business effectively.

How Coverage Limits Are Set and Managed

Setting coverage limits is not a one-size-fits-all approach. Insurers rely on specific evaluation methods to establish and manage these limits, often tailoring them to individual circumstances. By understanding how these limits are determined and adjusted, you can better collaborate with your insurer to secure the right level of protection for your business. Below, we’ll explore the key factors and processes that influence coverage limits.

Factors That Affect Coverage Limits

When you request a credit limit for a customer, the insurer begins by assessing the buyer’s financial health and overall risk profile. This evaluation includes several key considerations:

- Financial Strength: Insurers analyze the buyer’s annual accounts, management accounts, and other financial statements to gauge their stability and creditworthiness.

- Payment History: A buyer’s track record of paying on time is critical. The International Credit Insurance & Surety Association emphasizes the importance of credit assessments for every buyer in an insured’s portfolio. Insurers also check for any adverse judgments or legal actions that could signal risk.

- Macroeconomic and Industry Risks: Broader economic trends and industry-specific challenges can impact coverage limits. For instance, buyers in highly volatile sectors may face lower limits even if their financials appear strong.

- Transaction Details: The specifics of each transaction matter, including the requested limit amount, payment terms, and payment methods. If you’ve secured guarantees or other protections for a buyer, these can positively influence the insurer’s decision.

- Your Business Practices: Insurers also evaluate your internal credit controls, historical loss record, and exposure to single buyers or related groups. Providing detailed buyer data – such as the buyer’s full legal name, registration or VAT numbers, and requested credit amount – helps prevent errors in coverage decisions.

Adjusting Coverage Limits Over Time

Coverage limits are not static; they evolve with changing risks and business needs. Insurers continuously refine these limits based on updated information.

- Requesting Adjustments: As your business grows or market conditions shift, you can request changes to your limits. Many insurers offer online platforms like CofaNet or Allianz Trade Online, allowing you to submit requests and receive responses quickly, sometimes instantly.

- Seasonal or Temporary Adjustments: For fluctuations in demand, you can submit updated financial data – such as current management accounts – to justify temporary increases or adjustments. It’s a good idea to make these requests well in advance to ensure coverage is in place when needed.

- Monitoring Services: Some insurers provide proactive monitoring. If a buyer’s creditworthiness improves, they may notify you of opportunities to increase coverage. Conversely, insurers might suggest reducing limits if new risks emerge. In cases where a limit is canceled, a delayed effect period (typically 30 days) ensures existing shipments remain covered during the transition.

- Using Discretionary Limits: For smaller accounts, you can often adjust coverage using your policy’s discretionary limit. These self-approved limits may rely on a Credit Intelligence Opinion (CIO), reports from approved credit agencies, or documented payment histories showing the highest balance paid within terms. Keeping detailed records of payment performance is crucial for supporting these adjustments.

- Calculating Exposure: To ensure your requested limits align with your actual exposure, calculate your maximum outstanding balance using the formula: (monthly sales ÷ 30) × payment terms. Regularly updating records on your top buyers is also important, as insurers may request a buyer review form if negative information arises.

Managing coverage limits effectively is a cornerstone of a strong trade credit risk strategy. By staying proactive and providing accurate, up-to-date information, you can help ensure your business remains well-protected.

Other Factors That Affect Coverage Limits

Coverage limits aren’t solely determined by the amounts you choose – they’re also shaped by key policy features like indemnity percentages and deductibles. These factors play a critical role in determining the final payout of your claims.

Indemnity Percentage and Deductibles

When it comes to claim payouts, your buyer’s approved credit limit doesn’t mean you’ll receive the full amount. The indemnity percentage – sometimes called coinsurance – dictates what portion of your loss the insurer will cover. This percentage typically falls between 80% and 95%. The remaining 5% to 20% is referred to as your insured retention, which is the portion of the loss you’re responsible for covering.

For instance, if you have a $100,000 credit limit for a buyer and your policy includes a 90% indemnity level, the maximum claim payout you’d receive is $90,000. Allianz Trade explains it this way:

"The insurance indemnifies a proportion (up to 95%) of the debt owed to you. You must have traded within the limit we give you for that customer".

Deductibles are another factor that can reduce your claim payout. These are the out-of-pocket expenses you must exceed before the insurer begins to pay. Deductibles can be structured in two primary ways: as an aggregate deductible, which applies to the total losses over the policy year, or as individual buyer deductibles, which apply to each claim separately. Many policies also include a small claim threshold, meaning losses below a certain amount won’t qualify as insured events. If a significant number of your invoices fall below this threshold, those transactions won’t be covered.

As Maheswaran Sudagar, Senior Vice President and Lead Actuary at Crum & Forster, puts it:

"The actual recovery is an amalgamation of policy features"

where your final payout reflects the loss amount minus any recoveries, deductibles, and the coinsurance percentage. These features also influence the premiums you pay.

Premiums and Policy Fees

These policy features don’t just affect claim payouts – they also play a big role in shaping your premiums and fees. Coverage limits, in particular, directly impact the cost of your policy. Premiums are often calculated as a percentage of your total insurable sales volume, with rates typically ranging from 0.15% to 0.80% of insured turnover for portfolio policies. For example, a business with $20 million in annual sales might pay a premium of less than $50,000.

The connection between coverage limits and premiums is based on a risk-based pricing model. Higher limits increase your Exposure at Default (EAD), which insurers use to estimate potential loss costs. Similarly, opting for a higher indemnity percentage, like 95% instead of 90%, raises the insurer’s Loss Given Default (LGD), leading to higher premiums. However, if you’re using trade credit insurance to secure financing, many lenders won’t adjust their advance rates for that extra 5% of coverage.

You can lower premium costs by strategically adjusting policy features. For instance, increasing deductibles or choosing a lower indemnity percentage shifts more risk to your business, which can help reduce premiums. Beyond basic premiums, additional fees may apply for managing your coverage limits. These might include costs for requesting Credit Intelligence Opinions (CIOs) to justify discretionary limits or fees for credit limit applications and monitoring services.

How Coverage Limits Support Risk Management

Coverage limits go beyond being just numbers on a policy – they act as practical tools for managing risk, shielding your business from potential customer defaults. By setting a coverage limit for a buyer, you essentially cap the financial risk tied to that specific customer. If they fail to pay, the insurer reimburses up to the limit (after factoring in the policy terms), helping safeguard your cash flow from being severely impacted by one customer’s financial troubles. These measures also encourage ongoing oversight of your credit exposure.

In addition to financial protection, coverage limits serve as an early indicator of credit issues. Peter Aitken, Vice President of Special Products at Atradius Trade Credit Insurance, Inc., highlights this benefit:

"Some companies perceive value in having the insurer serve as an adjunct to their own internal credit management function and an early warning beacon about problems associated with their customers".

If a coverage limit is reduced or withdrawn, it signals a decline in your customer’s creditworthiness. This gives you the opportunity to reassess your sales strategy and reduce the risk of future losses.

Coverage limits also enhance your ability to secure financing. Banks are more likely to offer higher advance rates – typically 80% to 85% compared to 70% – on insured receivables because the credit risk is transferred to the insurer. This increased borrowing capacity can be crucial for maintaining working capital and supporting growth, particularly when dealing with international buyers.

Monitoring and Updating Coverage Limits

Your coverage needs are not static – they evolve alongside your business, customer payment habits, and market conditions. Regular reviews and adjustments ensure that your limits match your actual credit exposure and remain sufficient as circumstances change.

Customer payment behavior plays a key role. Late payments increase your outstanding balance, which may require higher coverage limits or even a reassessment of whether to continue extending credit. Temporary spikes in exposure, such as during seasonal demand surges, also need attention. For example, retailers often require higher limits during the holiday season when inventory orders peak. These changes highlight the importance of real-time monitoring systems.

To keep everything on track, integrate your policy limits into your ERP system. This allows your sales and credit teams to monitor available coverage in real time. Assign a dedicated policy owner to handle limit requests, track overdue accounts, and enforce terms like stop-shipment rules. These rules typically require halting deliveries for accounts that are 60 to 90 days overdue, helping you avoid accumulating further uncovered debt.

If a limit is withdrawn, insurers often provide a Delayed Effect Period – usually 30 days – during which shipments remain covered. Use this time to collect outstanding payments or work with your customer to provide updated financial information for the insurer. Submitting fresh financial statements could lead to higher approved limits.

Managing Uncovered Risks and Exclusions

While monitoring coverage limits is essential, understanding policy exclusions is equally important for managing your overall risk. Some risks fall outside the policy’s protection, and identifying these gaps helps you prepare for potential losses that won’t be reimbursed.

For instance, violating policy conditions can void your coverage. If you continue shipping to a customer who has exceeded the stop-shipment threshold or fail to report overdue accounts within the required timeframe, you risk losing protection for those transactions. This is why assigning a policy owner to oversee notice rules and ensure delivery proofs are collected is so critical.

For larger accounts where your primary insurer’s limit falls short, consider Top-Up insurance to extend coverage beyond the initial cap. This layered approach ensures you’re adequately protected for your most significant customers. For smaller accounts managed under discretionary limits, maintain proper documentation – such as credit reports or trading histories showing the highest balance cleared within terms. This helps avoid claim denials due to insufficient proof.

Getting the Right Coverage Limits with Accounts Receivable Insurance

When it comes to managing risk effectively, setting the right coverage limits is key. Accounts Receivable Insurance (ARI) offers a tailored approach, helping businesses secure the protection they need by aligning policies with their specific risk profiles. This ensures financial stability and reliable cash flow, even in uncertain conditions.

Tailored Policies for Your Business Needs

ARI provides flexibility by offering different policy structures to suit your business model and customer base. For companies with a diverse range of buyers, a Whole Turnover policy is a great option. It covers all customers and often comes with competitive pricing. On the other hand, if your business relies heavily on a few key accounts, a Key Accounts or Single Buyer policy focuses on protecting your largest exposures. This approach not only reduces administrative complexity but also directs protection to where it’s needed most.

Credit limit management is another area where ARI shines. For smaller, routine exposures, policies often include Discretionary Limits. These allow you to approve orders quickly based on your own credit checks or trading experience, bypassing the need for insurer approval. For larger exposures, you’ll apply for Approved Limits, which rely on the insurer’s in-depth risk analysis. The good news? About 85% of these requests are processed in under 48 hours [29,30]. This blend of flexibility and precision ensures your policy evolves alongside your business.

Expert Risk Assessments for Better Protection

Once your policy is customized, ARI’s professional risk assessments take things a step further. These assessments use extensive global databases covering over 85 million companies to guide credit limit decisions [29,30]. Underwriters evaluate buyer and country risks, assigning proprietary risk grades that reflect the likelihood of default. Their analysis is informed by various sources, including financial statements, public records, shared data from other policyholders, and even on-site visits to buyers [14,20].

Mike Libasci, President of International Fleet Sales, highlights the benefits:

"Accounts receivable insurance has allowed us to take on customers and transactions we wouldn’t have felt comfortable taking on by ourselves".

Additionally, insurers keep a close eye on your buyers, providing early alerts if their creditworthiness changes. They’ll also notify you when positive updates allow for increased coverage [9,29]. This ongoing monitoring ensures your coverage limits stay aligned with both your business needs and market shifts, keeping you one step ahead.

Conclusion

Understanding and managing coverage limits goes beyond just protecting your business from financial losses – it’s about creating opportunities for growth. Coverage limits outline the extent of protection available for each customer and across your entire portfolio. Any amounts exceeding those limits remain uninsured.

Effectively managing these limits does more than mitigate losses; it can act as an early warning system. If a customer’s creditworthiness begins to decline, you can reduce your exposure before a default happens. This proactive approach has saved many businesses from unexpected financial setbacks.

Coverage limits also play a practical role in strengthening your financial position. With the right insurance in place, you can confidently offer credit terms like Net 30 or Net 60 to new customers, enabling you to secure more sales and expand into new markets without taking on unnecessary risk. Since accounts receivable often represent a business’s largest asset, defined coverage limits can improve lender confidence, increase borrowing capacity, and even lead to better interest rates.

The numbers speak for themselves: trade credit insurance typically covers between 75% and 95% of outstanding debt in insured losses. In 2020, around 14.52% of global trade was protected by trade credit insurance. With corporate defaults and insolvencies accounting for 25% of all business bankruptcies, having the right coverage limits is essential for maintaining financial stability.

FAQs

How do I know if my buyer credit limit is high enough?

To determine whether your buyer credit limit meets your needs, start by examining the buyer’s financial stability, payment history, and any risks associated with their industry. Then, compare these insights with the credit limits provided by your insurer. Make sure these limits align with your sales volume and your comfort level with risk. If necessary, adjust the limits to strike a balance between seizing growth opportunities and maintaining financial security.

What happens if I ship after a buyer’s limit is reduced or canceled?

If you ship goods after a buyer’s credit limit has been reduced or canceled, the insurer usually won’t cover any nonpayment issues. This could leave you responsible for the financial loss. Since coverage limits are often either non-cancelable or come with specific restrictions, it’s crucial to thoroughly review your policy terms before proceeding with any shipment.

Can I increase my policy’s maximum liability during the policy year?

Yes, you can ask to increase your policy’s maximum liability limit at any time during the policy year through a mid-term adjustment (MTA). This process lets you modify your coverage to better align with any changes in your situation, though it will require approval.