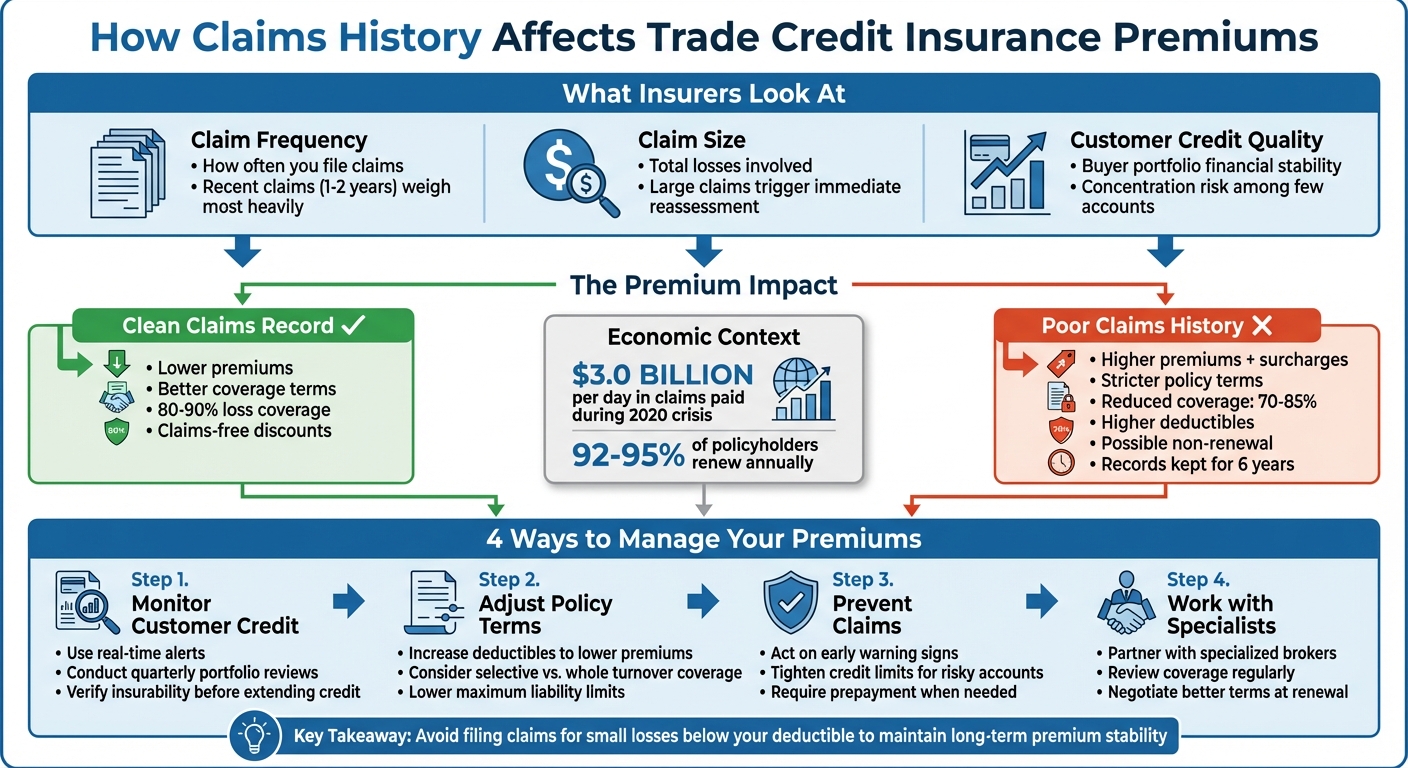

Your claims history directly impacts the cost of your trade credit insurance. Insurers assess how often you file claims, the size of those claims, and the financial health of your customers. Frequent or large claims signal higher risk, leading to increased premiums, stricter policy terms, or even non-renewal. On the other hand, a clean claims record can help you secure better rates and terms.

Key Takeaways:

- Frequent Claims: Suggest weak risk management, resulting in higher premiums and potential surcharges.

- Large Claims: Lead to immediate reassessment of risk and possible premium hikes.

- Customer Creditworthiness: Defaults by your customers can increase your premiums, even with a clean claims record.

- Economic Downturns: Claims spikes during recessions can worsen premium increases for businesses with poor claims histories.

How to Manage Premiums:

- Monitor customer credit and adjust terms for high-risk accounts.

- Avoid filing claims for smaller losses below your deductible.

- Work with specialized brokers to optimize your policy and risk management.

- Review and improve your claims record before policy renewal.

How Claims History Impacts Trade Credit Insurance Premiums

How Claims History Affects Premium Pricing

What Insurers Look at in Your Claims Record

When insurers evaluate your claims history, they focus on two key factors: how often claims are made and the total losses involved. Frequent, smaller claims can indicate weak risk management, which often leads to surcharges and even safety inspections.

As Sam Grieves from Brier Grieves Insurance explains:

"Frequent claims suggest a lack of effective risk management and may lead to surcharges, safety inspections, and increased scrutiny at renewal".

Another factor insurers consider is concentration risk. This means they look at whether your claims are spread across a broad customer base or concentrated among a few key accounts. If your business heavily depends on a small number of buyers – especially those with a history of defaults – it increases your risk profile.

Timing also matters. Recent claims, typically those made within the last one to two years, carry more weight in underwriting decisions than older claims from three or four years ago. By understanding these factors, you can take steps to improve your risk management practices and potentially avoid premium increases.

How Buyer Creditworthiness Affects Premiums

Your customers’ financial stability plays a major role in determining your premium rates. Even if your claims record is clean, a history of customer defaults can still lead to higher premiums.

Kirk Elken, Co-founder of Securitas Global, highlights this connection:

"Customer defaults drive premium increases".

Insurers don’t just look at your claims – they also assess the overall credit quality of your buyer portfolio. If your records show repeated defaults from financially unstable customers, you’re likely to face higher rates at renewal. On the flip side, businesses that primarily extend credit to financially reliable customers often enjoy lower premiums. This aspect of customer credit quality becomes particularly important during the annual renewal process.

Premium Changes at Renewal Time

Every year, during the renewal process, insurers take a deep dive into your claims history. This review determines whether your premiums will rise, your coverage will narrow, or if favorable terms will remain intact.

A poor claims record can lead to several challenges at renewal. You might lose claims-free discounts, face higher deductibles, or see new policy exclusions that limit your coverage. In more severe cases, frequent or significant losses could result in a non-renewal notice, leaving you to seek coverage in the pricier non-standard market.

To avoid these outcomes, it’s a good idea to review your claims history well before renewal. Identifying areas for improvement and addressing them proactively can help you maintain better terms and avoid unexpected premium hikes.

sbb-itb-2d170b0

Problems Caused by a Poor Claims Record

Increased Costs and Limited Coverage Options

When claims are frequent or particularly high in value, insurers see you as a bigger risk. This perception doesn’t just lead to higher premiums – it can also shrink your coverage options. Insurers may decide to avoid insuring certain high-risk businesses altogether or cap the total coverage they’re willing to provide for your receivables portfolio. As Niche Trade Credit puts it:

"If you work with a business with a history of bad debt, you will pay more insurance premiums. In some cases, you may be unable to insure risky debts".

A poor claims record can also result in stricter policy terms. For example, while standard policies might cover 80–90% of losses, a tarnished claims history could mean reduced compensation levels of 70–85% and higher deductibles.

The consequences of a poor claims record aren’t short-lived, either. Insurers typically keep these records for about six years, meaning a significant loss today could keep your premiums elevated for years to come. This challenge becomes even more pronounced during tough economic times.

Economic Downturns and Claim Spikes

Economic downturns tend to amplify these issues. During recessions, the likelihood of customer non-payment increases across industries, prompting insurers to raise premiums for everyone. But if your claims history is already poor, these general increases can hit you even harder, compounding the strain on your budget.

To put things into perspective, insurers were paying out an estimated $3.0 billion per day in claims during the global crisis of 2020. As FasterCapital explains:

"The pandemic led to a surge in claims, which in turn put upward pressure on premium rates as insurers sought to cover the unexpected spike in payouts".

When insurers face periods of high payouts, they become more cautious. They tighten their underwriting guidelines, reduce coverage limits, and scrutinize businesses with prior claims even more closely. If your claims spiked just before or during an economic downturn, the impact on your renewal terms could be both immediate and severe. Recent claims – those made within the last one to two years – carry the most weight in determining pricing, making timing a critical factor.

How to Control Premium Increases

Monitor Customer Credit More Closely

Keeping premiums steady starts with staying on top of your credit management practices. Trade credit insurance can play a key role here. Before extending credit terms to new customers, confirm whether they’re insurable. If coverage is limited or declined, it might be time to reconsider that relationship.

Using real-time alerts allows you to adjust credit terms immediately when risks arise. Conducting quarterly portfolio reviews can also help you spot accounts that are approaching their credit limits or no longer represent a sound risk. Letting customers know their accounts are insured and monitored by third-party risk assessors can encourage timely payments and highlight weaker buyers early on. These steps give you the tools to adjust your policy terms before risks turn into losses.

Modify Your Policy Terms and Deductibles

Tweaking your policy structure is another way to manage premium costs. For instance, increasing your deductible shifts more of the initial loss to you, which lowers the insurer’s risk and could result in a lower premium. If your financial reserves are strong enough to handle this, it’s worth considering.

You might also look into changing your coverage approach. Instead of a whole turnover policy, which covers all accounts, you could opt for targeted coverage focused on key accounts. While whole turnover policies spread risk across your entire portfolio, selective coverage can save money if you have solid internal credit management in place. Another option is to lower your policy’s maximum liability – the total annual payout from the insurer – which can also reduce your premium. These adjustments allow you to take a more active role in managing risks before claims arise.

Take Action Before Filing Claims

Proactive measures are your best defense against filing claims. The goal? Avoid claims altogether. If you notice warning signs like late payments or credit downgrades, act quickly. Tighten credit limits, shorten payment terms, or require prepayment or cash-on-delivery to reduce your exposure.

Specialized brokers, such as Accounts Receivable Insurance, can be invaluable in these situations. They can help you address potential risks early by negotiating temporary credit limit adjustments or policy endorsements with insurers. This approach not only protects your financial interests but also helps maintain good relationships with both your customers and your insurer.

Maintaining a Good Claims Record for Stable Premiums

Work With Specialized Insurance Brokers

Teaming up with a knowledgeable insurance broker can make a big difference in keeping your premiums steady. Brokers who specialize in accounts receivable insurance understand the finer details of policies and can provide valuable advice on how insurers view your specific risk profile. They’ll help you choose a policy structure that truly fits your business needs – whether that’s comprehensive coverage for all accounts or focusing on key ones.

David Patten, CEO and CFO of Everchem LLC, highlights this benefit:

"Securitas and credit insurance have allowed us to focus on expanding our business with confidence. They helped Everchem realize that credit insurance isn’t really a cost, but a way to expand business revenues while reducing risk."

Regularly reviewing your coverage with your broker ensures your risk management strategy stays effective.

Use Regular Risk Reviews and Renewal Planning

The policy renewal period is a prime opportunity to reassess your coverage. Between 92% and 95% of trade credit insurance policyholders renew annually. During this time, gather multiple quotes and examine how insurers evaluate your portfolio. If your buyer base has improved or your sales have grown, these positive changes could lead to better premium rates.

Frequent reviews also allow you to adjust your policy structure. For instance, insuring a diverse group of reliable customers spreads out risk and can help lower costs, while focusing only on higher-risk accounts might do the opposite. Additionally, aligning your projected sales accurately during renewal is critical since premiums often depend on these forecasts. This approach not only optimizes your coverage but also enhances claims management in the long run.

Develop Better Claims Management Processes

The best way to manage claims? Prevent them in the first place. By setting up internal systems to catch potential issues early, you can avoid unnecessary claims. Take advantage of your insurer’s tools for monitoring buyer creditworthiness. If you get alerts about a buyer’s deteriorating financial health, act immediately – adjust credit limits, revise payment terms, or even require upfront payments to minimize losses.

When selecting coverage, prioritize the insurer’s ability to provide credit limits over simply hunting for the lowest price. If an insurer hesitates to approve limits for certain buyers due to risk concerns, it might be a sign to reevaluate your portfolio. Addressing these red flags before your policy renewal – whether by improving your customer base or tweaking credit policies – can lead to more stability and potentially lower premiums over time.

Conclusion

Main Points to Remember

Your claims history plays a big role in determining what you’ll pay for trade credit insurance. Insurers often see frequent or large past claims as indicators of higher future risk, which can lead to higher premiums when it’s time to renew. On the flip side, a clean claims record can work in your favor. Businesses that maintain strong internal credit controls and keep claims to a minimum often secure better rates and terms.

How often you file claims also impacts your premiums. That’s why it’s smart to weigh the costs and benefits before submitting a claim. For smaller losses – especially those below your deductible – it might make more sense to handle them out-of-pocket. This approach can help you avoid long-term premium increases and preserve any claims-free discounts.

Interestingly, between 92% and 95% of businesses renew their trade credit insurance policies each year. This makes the renewal period a prime opportunity to renegotiate terms. Use this time to showcase any improvements you’ve made, like enhanced credit controls, a broader customer base, or better debt collection processes. These proactive steps demonstrate to insurers that you’re actively managing risk, not just reacting to problems, which could lead to better premiums down the road.

What to Do Next

Take a close look at your internal claims log to spot any patterns. Are certain customers or industries responsible for repeated losses? Could earlier credit monitoring have prevented some of these claims? Pinpointing these trends can help you address issues before your next renewal.

Consider reaching out to specialists for personalized advice. Accounts Receivable Insurance offers tailored trade credit insurance solutions, risk assessments, and expert claims management services. Their team can help you design policies that balance comprehensive coverage with cost efficiency.

How much does Trade Credit Insurance (TCI) cost?

FAQs

How far back do insurers look at my claims history?

Insurers typically look at your claims history from the last 3 to 5 years. This review helps them assess your risk level and determine the cost of your trade credit insurance. If you have a clean claims record, it could work in your favor by lowering your premiums. On the other hand, frequent or large claims might result in higher insurance costs.

Will my premium increase if my customers’ credit worsens but I don’t file claims?

Yes, your premium can go up if your customers’ credit scores drop, even if no claims are filed. Insurers often use creditworthiness as a key factor when calculating premiums. Keeping an eye on and managing your customers’ credit risk can help reduce the chances of premium increases.

Should I avoid filing small claims to keep my premium lower?

Filing small claims might seem like a quick solution, but it can add to your claims history. Over time, this could lead to higher trade credit premiums. To help keep your premiums in check, it’s often a good idea to avoid filing claims for minor issues when possible.