Trade credit insurance helps businesses protect themselves from financial losses due to customer non-payment. This coverage is vital for managing risks like buyer insolvency, payment delays, and geopolitical disruptions. However, changes in U.S. policies – such as tariffs, sanctions, and export controls – can increase trade credit risks and lead to stricter insurance terms, reduced coverage, and higher premiums.

Key takeaways:

- Tariffs: Raise costs for buyers, squeezing margins and increasing default risks.

- Sanctions: Can make previously insurable transactions illegal, requiring policy adjustments.

- Currency controls: Delay payments and often fall outside standard coverage, needing specialized endorsements.

Businesses can manage these risks by monitoring policy changes, diversifying markets, and restructuring their insurance policies to align with evolving challenges. Accounts Receivable Insurance (ARI) offers tailored solutions to safeguard receivables and maintain financial stability amidst policy-driven uncertainties.

How Policy Changes Impact Trade Credit Insurance: A Visual Guide

Credit Insurance as a Risk Mitigation Tool for International Trade

Government Policy Changes That Affect Trade Credit Insurance

Building on the discussion of rising trade credit risks, let’s explore how specific government policies are reshaping the conditions for trade credit insurance.

Tariffs and Trade Barriers

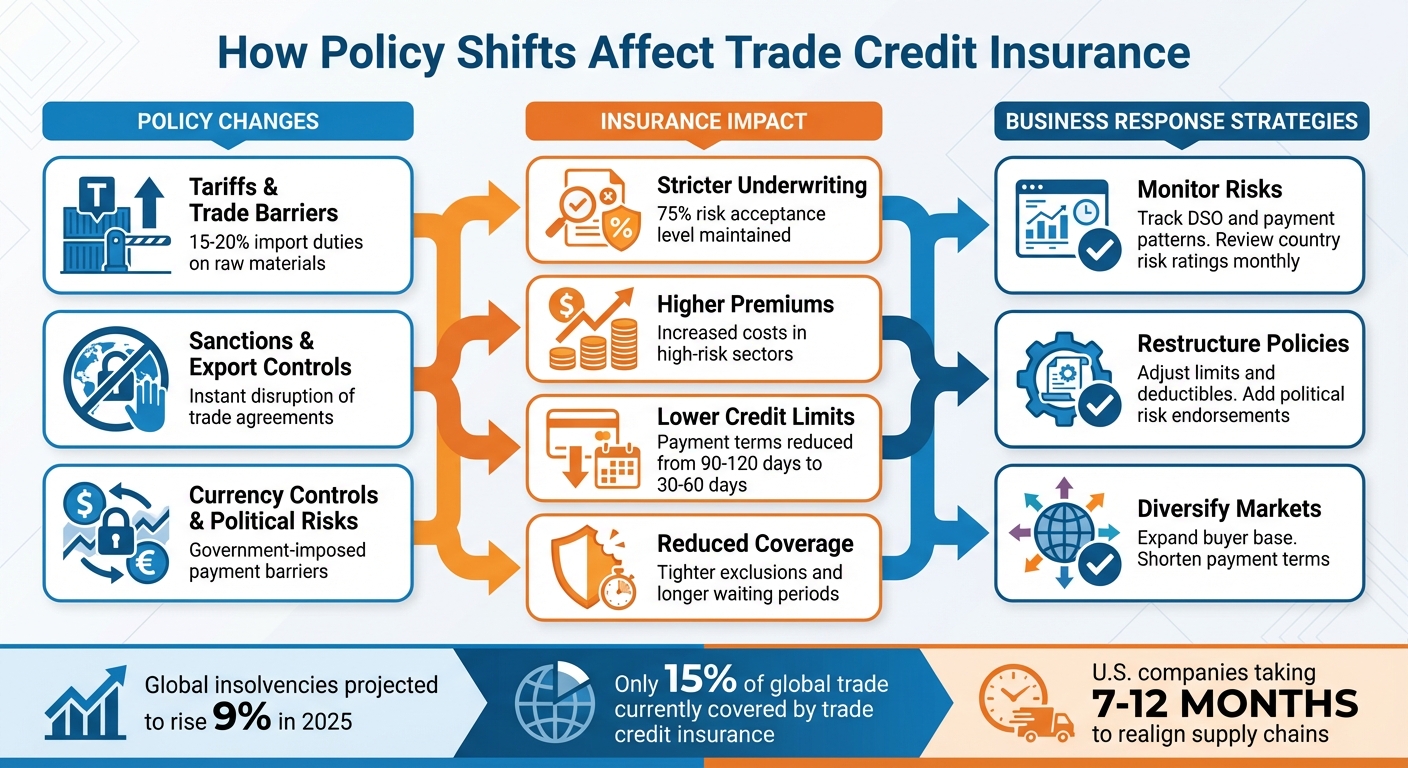

The introduction of higher U.S. tariffs and new trade barriers has sent shockwaves through supply chains. For example, import duties – ranging from 15% to 20% on raw materials – have driven up costs for manufacturers and distributors. These increased expenses often squeeze profit margins and strain working capital, especially when companies can’t immediately pass these costs on to their customers.

For trade credit insurers, this creates a ripple effect. Narrower profit margins heighten the risk of insolvency, prompting insurers to tighten their underwriting practices. This often means reducing per-buyer credit limits, raising premiums, and focusing on sectors most vulnerable to tariffs, such as manufacturing and consumer goods that depend on imported components. U.S. sellers may find their insured credit lines reduced, while payment terms shrink from the usual 90–120 days to as little as 30–60 days, limiting open-account exposure. These adjustments significantly alter the trade credit landscape.

Sanctions and Export Controls

Sanctions and export controls imposed by the U.S. government can disrupt trade agreements almost instantly. When a foreign entity, sector, or country is sanctioned, transactions that were legal one day can become unpayable the next. Payments may be frozen if sanctioned banks or intermediaries are involved, and shipments canceled or rerouted, increasing the chances of disputes and non-payment. A buyer who was once deemed creditworthy can quickly become uninsurable.

While standard trade credit insurance covers risks like insolvency and prolonged default, many policies include sanctions clauses. These clauses exclude claims if paying them would violate U.S. or international sanctions. Losses from contracts that become illegal or from buyers unable to make payments due to sanctions often fall outside standard coverage. Specialized extensions, such as political risk or contract frustration coverage, are often required to address these gaps. Insurers respond by reevaluating exposure to certain countries, sectors, and buyers, tightening policy terms, increasing compliance requirements, and adjusting premiums or deductibles for higher-risk areas.

Currency Controls and Political Risks

Government-imposed currency controls and capital restrictions can prevent buyers from converting local currency into U.S. dollars or transferring funds abroad. Even when a buyer remains financially stable, these restrictions can cause significant payment delays, creating liquidity challenges for U.S. exporters.

Standard trade credit insurance typically doesn’t cover risks tied to government-imposed payment barriers. To address this, insurers offer political risk extensions. These extensions cover risks like currency inconvertibility and transfer restrictions, providing payouts after a waiting period if regulations block currency conversion or fund transfers. They may also include contract frustration coverage, which protects against losses from government actions such as embargoes, import bans, or license cancellations. However, these extensions come with higher premiums, stricter sublimits for specific countries, longer waiting periods, and more rigorous underwriting to ensure non-payment stems solely from government intervention.

How Policy Changes Affect Insurance Coverage and Pricing

When government policies shift – whether through tariffs, sanctions, or currency controls – trade credit insurers adapt by revising their pricing models, tightening underwriting standards, and restructuring coverage terms. These adjustments directly impact what businesses can insure, how much they pay, and the credit limits available for their buyers.

Stricter Underwriting and Lower Coverage Limits

Uncertainty in government policies often prompts insurers to reevaluate their risk exposure across different sectors and markets. For instance, when tariffs drive up costs or sanctions disrupt payment flows, insurers face higher probabilities of defaults. These risks are integrated into their underwriting models, which can result in reduced market capacity, lower credit limits, or even withdrawal from high-risk sectors.

Take the case of the significant U.S. tariffs introduced in 2025. Insurers quickly adjusted their models, with underwriting teams tightening terms even before claims began to surface. Analysts note that external economic factors are automatically reflected in these risk models, leading to reduced coverage and increased premiums. Recent trends show that while premiums are climbing in high-risk sectors and regions, businesses in more stable markets may still have some leverage to negotiate terms. However, in areas affected by tariffs or sanctions, the increased frequency and value of claims have driven premiums higher [3, 13]. These market dynamics set the stage for further changes in political risk coverage and buyer terms, as discussed in the following sections.

Changes to Political Risk Coverage

In addition to stricter underwriting, shifts in policy often lead to adjustments in political risk endorsements. New policies that introduce additional risks – like expanded sanctions or sudden export controls – prompt insurers to limit their exposure. These changes typically involve stricter exclusions for sanctioned countries, longer waiting periods for claims, and narrower definitions of covered events.

Following the U.S. trade policy changes in January 2025 under the Trump administration, insurers implemented tighter exclusions and revised terms for political risks. Particular focus was placed on tariff-related losses and trade disputes. Coverage that previously offered broader protection now often comes with higher deductibles and more specific exclusions to manage the spike in claims caused by prolonged disruptions.

For businesses trading in politically volatile markets, it’s critical to carefully review exclusions, waiting periods, and country-specific limits within their political risk endorsements. Some insurers may offer buy-back options for certain exclusions or provide tailored endorsements at an additional cost. However, these options typically require more stringent underwriting to ensure that losses are clearly tied to government actions [7, 9].

Effects on Buyer Credit Limits and Payment Terms

As policy uncertainty grows, both insurers and businesses are forced to reassess buyer terms, emphasizing the need for flexible financial strategies. Policy-driven changes also influence the credit limits insurers are willing to extend to individual buyers and the payment terms they support. For example, when currency controls or tariffs increase buyer vulnerability, insurers may reduce limits, shorten payment periods, or decline coverage for specific buyers or countries. This can force sellers to adjust by tightening payment terms.

These changes often have a ripple effect on working capital management. Reduced insured receivables can create liquidity pressures, pushing businesses to explore alternative financing options or revise their pricing strategies. A March 2025 survey by WTW highlighted the growing demand for trade credit insurance amid tariff risks, with Aon‘s H1 2025 report showing insurers maintaining a 75% risk acceptance level. Meanwhile, global insolvencies are projected to rise by 9% in 2025, further straining businesses as insurers impose stricter terms and lower credit limits.

KPMG reports that many U.S. companies are taking 7–12 months to realign their supply chains in response to these shifts. Jerry Paulson from HUB International advises risk managers to secure coverage while capacity remains relatively available, emphasizing that tariffs of 15%–20% on raw materials are increasing the risks of unpaid invoices. As policy uncertainty persists and loss ratios climb, the window for securing favorable terms may continue to narrow [3, 14].

sbb-itb-2d170b0

How Businesses Can Adapt to Policy Changes

As shifts in trade credit insurance policies continue to impact the business landscape, companies need to take proactive steps to protect their cash flow and maintain favorable terms. By closely managing risks, adjusting policies, and diversifying exposure, businesses can navigate tighter underwriting standards and rising premiums with greater confidence. Below are practical strategies to help mitigate risks tied to these policy changes.

Keep a Close Eye on Country and Policy Risks

Building a strong monitoring system is key to staying ahead of potential challenges. Finance and credit teams should track warning signs like rising Days Sales Outstanding (DSO), late payments, or increased use of credit limits across specific countries and sectors. These patterns often signal deeper policy or economic issues on the horizon. Externally, staying updated on U.S. and international trade policies through resources like the U.S. International Trade Administration or the Department of Commerce can provide valuable insights. Additionally, monitoring country risk ratings from insurers and brokers and reviewing insolvency forecasts – currently predicting elevated corporate failures through 2026 – can help businesses anticipate risks.

Many trade credit insurers offer online tools and alerts to notify users of changes in a buyer’s or country’s risk category. Incorporating these alerts into weekly credit meetings ensures credit and finance teams can swiftly align open-account terms and insured credit limits with emerging risks. To stay organized, consider a structured approach: monthly reviews of country risks, quarterly portfolio analyses, and detailed documentation of these activities. Such efforts demonstrate active risk management to underwriters, which can improve pricing and capacity.

Predefined risk triggers, such as a country downgrade or inclusion on a sanctions list, can prompt immediate adjustments to credit terms and insured limits. For instance, if tariffs or sanctions raise costs in a specific sector, companies might shorten payment terms (e.g., from net 60 to net 30), tighten credit limits, or require partial advance payments for new orders. These measures ensure your trade practices and insurance coverage remain aligned with the latest policy developments.

Reassess and Restructure Insurance Policies

Regularly reviewing and updating insurance policies – whether annually or following significant policy changes – can help businesses stay protected. Key adjustments might include revisiting maximum policy limits, per-buyer limits, deductibles, coinsurance percentages, and endorsements tailored to specific risks.

In higher-risk environments, businesses might negotiate higher aggregate limits or seek additional capacity for strategic markets, even if it means accepting higher premiums or deductibles. Instead of applying uniform caps, consider setting per-buyer limits based on internal credit evaluations. While increasing deductibles and coinsurance can reduce premiums by absorbing more initial risk, higher limits and broader political risk endorsements may provide stronger protection during major policy disruptions.

For companies heavily reliant on specific buyers or volatile markets, named-buyer or key-account policies offer more precise control. Larger firms with robust credit management systems might explore excess-of-loss (XoL) structures, allowing them to absorb smaller, expected losses while safeguarding against significant defaults triggered by policy changes. To ensure coverage aligns with real-world risks, businesses should confirm that policy terms account for their trading practices – whether through open accounts, letters of credit, or consignment – and that events like insolvency, political upheaval, or extended defaults are clearly defined.

Broaden Buyer Base, Markets, and Payment Options

Relying too heavily on a single buyer, group, or industry tied to tariffs, sanctions, or regulatory changes can heighten a company’s vulnerability. Diversification is a powerful way to spread risk, and starting early – especially when policy changes are anticipated – can make all the difference.

Expanding into markets less affected by trade disputes is one approach. Leveraging data from insurers and brokers can help identify sectors and buyers showing signs of credit deterioration due to policy changes, allowing businesses to limit their exposure. On the payment front, shortening payment terms, requiring partial or full upfront payments, or using milestone-based billing for buyers in higher-risk countries can help balance sales growth with financial security.

Trade credit insurance plays a crucial role here, offering the confidence needed to explore new markets or buyers that might otherwise seem too risky. By supporting diversification efforts, businesses can better manage the challenges posed by policy-driven uncertainties while maintaining steady growth.

How Accounts Receivable Insurance Helps Manage Policy Risks

When trade policies shift and create uncertainty around buyer creditworthiness or country-specific risks, having the right support can mean the difference between maintaining stability or facing serious cash flow challenges. Accounts Receivable Insurance (ARI) provides businesses with a structured way to protect receivables, even in the face of tariffs, sanctions, and regulatory changes. Let’s explore how ARI’s customized solutions and proactive risk management strategies help safeguard businesses as they navigate evolving policy risks.

Customized Coverage for Policy-Driven Challenges

Standard insurance policies often fall short when government policies change unexpectedly. ARI steps in with tailored coverage to address specific risks, whether it’s shielding domestic receivables from tariff-related buyer defaults or securing international sales against political risks like currency controls or export restrictions. By working with a strong network of credit carriers, ARI ensures businesses get the specific protection they need.

For example, U.S. exporters dealing with tariff hikes – where raw material costs might increase by 15–20% and gross margins shrink – can rely on ARI to adjust buyer limits and add political risk extensions. This ensures that coverage remains intact for key buyers, even as market conditions tighten. By transferring default risks to insurers, businesses can continue selling confidently, knowing their receivables are protected. Insurers typically maintain risk acceptance levels at around 75% to provide this crucial support.

Ongoing Risk Monitoring and Claims Assistance

Beyond offering tailored policies, ARI provides continuous risk monitoring and streamlined claims support. Their team tracks buyer financial health and monitors political developments in key regions, offering businesses early warnings when risks escalate. For instance, if new sanctions or tariffs stress specific sectors or buyers, ARI adjusts credit limits and issues alerts to help businesses adapt before losses occur.

If a buyer defaults due to policy changes, ARI’s claims process becomes a lifeline. They offer efficient claims handling and direct broker support to ensure businesses recover funds quickly. This is especially critical as global insolvencies are projected to rise 9% in 2025 and another 5% in 2026. With ARI’s backing, businesses can maintain cash flow stability even during challenging periods marked by tariff-related or sanction-driven payment failures.

Strengthening Financial Planning with Insured Receivables

Insuring receivables doesn’t just mitigate risks – it also enhances financial planning. Banks and asset-based lenders often view insured receivables as lower-risk collateral, which can improve borrowing terms. This means businesses can secure better advance rates, increase borrowing base availability, and extend more favorable payment terms to their customers. These benefits directly support treasury management and provide greater flexibility with credit facilities.

In today’s market, described as a soft market with competitive pricing and high carrier interest, businesses have an excellent opportunity to integrate trade credit insurance into their broader financial strategies. By consolidating global coverage programs and leveraging insurer-provided monitoring tools, companies can achieve cost efficiencies while building resilience against ongoing trade disruptions. This approach transforms trade credit insurance from a simple safety net into a strategic asset that supports growth, even as policy risks remain unpredictable.

Conclusion

Government policy changes – like tariffs, sanctions, export controls, and currency restrictions – are now a constant in global trade. For U.S. businesses operating on open account terms, these shifts bring heightened risks of buyer non-payment and corporate bankruptcies, leading to increased claims. While stricter underwriting and reduced credit limits are becoming the norm, trade credit insurance remains a vital tool for stabilizing cash flow, supporting sales, and securing financing – especially when policy-driven costs put pressure on profit margins.

Businesses navigating this landscape successfully are those that actively monitor country-specific and policy risks, adjust their insurance strategies as needed, and diversify both their buyer base and markets. This proactive approach not only protects cash flow but also prepares businesses to handle evolving risks. Trade credit insurance plays a crucial role in maintaining liquidity and improving borrowing terms, particularly when policy changes disrupt supply chains or tighten margins. With only about 15% of global trade currently covered by trade credit insurance, many companies still carry the burden of receivables risk on their balance sheets during times of uncertainty.

As policy-driven risks rise, specialized options like Accounts Receivable Insurance (ARI) address gaps left by standard trade credit coverage. ARI offers tailored protection for policy-related exposures, continuous risk monitoring, and efficient claims support – helping businesses safeguard their receivables from non-payment. Now is the time to secure or expand coverage before increasing insolvencies make conditions even more challenging.

To navigate this volatility effectively, businesses should stay informed about policy developments, adjust their coverage as needed, and integrate insured receivables into their financial plans. By partnering with ARI, companies can turn policy uncertainty into manageable risks – protecting cash flow and fostering growth even in the face of shifting trade policies. In a world marked by ongoing disruption, proactive risk management through trade credit insurance is essential for staying resilient and maintaining a competitive edge.

FAQs

How do tariffs affect the terms of trade credit insurance?

Tariffs can add a hefty layer of financial uncertainty to international trade. When governments impose tariffs, they often drive up costs for businesses, which can ripple through the supply chain, sometimes resulting in late payments or even buyer defaults.

In response to these risks, trade credit insurers may adjust their approach by tightening policy terms, raising premiums, or lowering coverage limits. To navigate these challenges, businesses should keep a close eye on their policies, ensuring they align with the shifting trade landscape. Partnering with providers like Accounts Receivable Insurance can also help businesses find tailored solutions to safeguard against these risks.

What can businesses do if their trade credit insurance doesn’t cover risks caused by government policy changes?

If your standard trade credit insurance falls short in covering risks tied to government policy changes, there are ways to bridge the gap. One option is to explore tailored insurance policies designed to address your specific challenges. These policies can offer protection against unique risks, such as those arising from political or regulatory changes.

Partnering with specialists like Accounts Receivable Insurance (ARI) can also be a game-changer. They provide access to risk evaluations, claims management support, and a global network of credit insurance providers. This combination of expertise and resources helps safeguard your business from financial uncertainties, whether at home or abroad. With proactive monitoring and expert advice, you’ll be better equipped to navigate shifting policy landscapes.

How do changes in government policies impact trade credit insurance, and how can businesses stay prepared?

Government policy changes can have a big impact on trade credit insurance, influencing factors like risk levels, payment terms, and overall market stability. To keep up with these shifts, businesses should make it a habit to evaluate potential risks, stay informed through government and industry updates, and collaborate with knowledgeable trade credit insurance providers.

Teaming up with a provider such as Accounts Receivable Insurance can be a smart move. They offer tailored coverage, proactive risk management strategies, and expert advice to help businesses adapt their policies as needed. This partnership ensures companies stay protected from financial risks like non-payment or political instability, even when regulations are in flux.