Political risk insurance protects businesses from losses caused by political events like government actions, civil unrest, and regulatory changes. This specialized coverage is essential for companies operating in volatile markets or expanding internationally, where standard insurance often falls short. Key risks include expropriation, currency restrictions, political violence, and trade disruptions.

To create effective political risk policies, businesses should:

- Identify risks: Categorize threats like political violence, government interference, and currency issues.

- Tailor coverage: Customize policies to match your specific operations and regions.

- Combine layers: Pair political risk insurance with other coverage like trade credit or supply chain insurance.

- Monitor and update regularly: Stay informed on geopolitical developments and adjust policies as risks evolve.

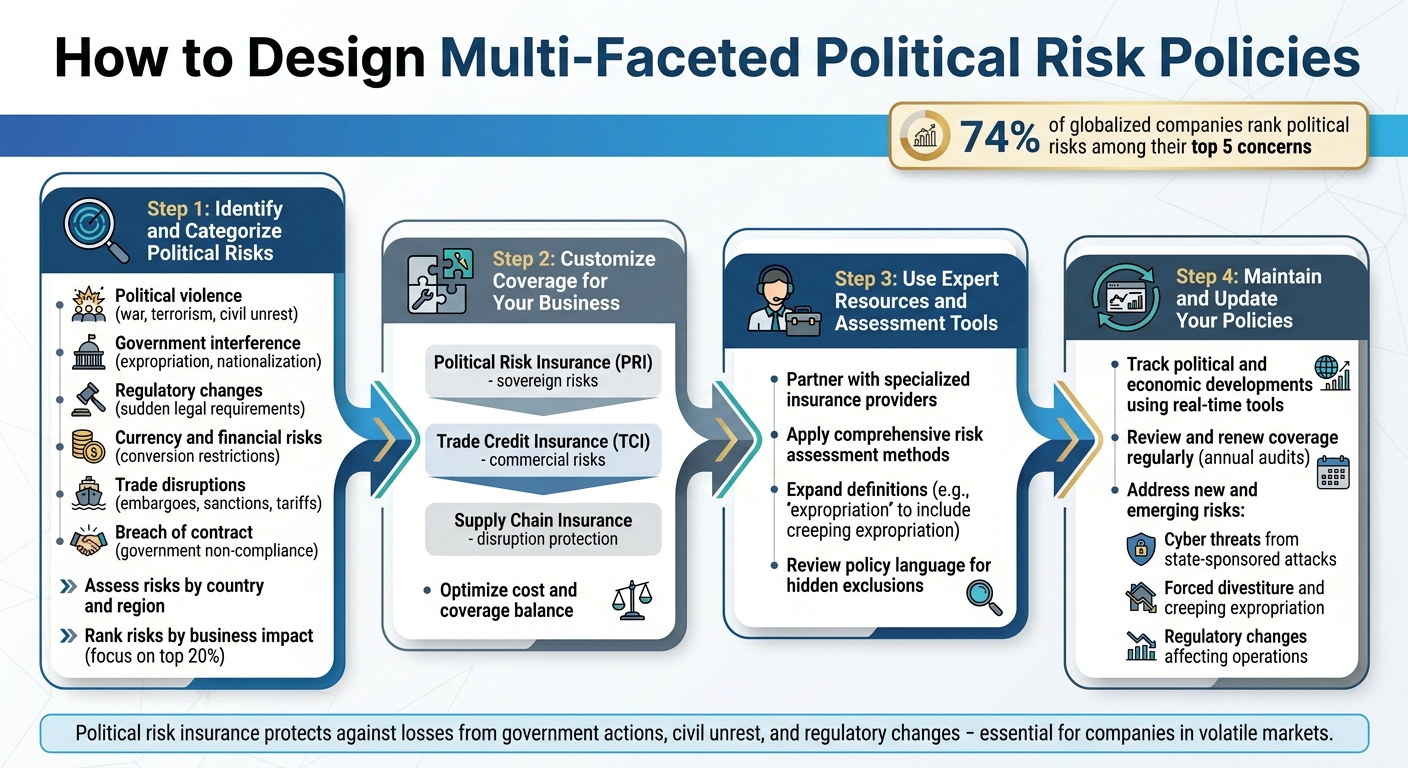

4-Step Framework for Designing Political Risk Insurance Policies

Super-cycle election year and political risk insurance

sbb-itb-2d170b0

Step 1: Identify and Categorize Political Risks

Start by pinpointing the political risks your business faces and grouping them into clear categories. Since political conditions can change rapidly, this step is crucial for understanding how these risks might affect specific locations and your overall operations.

Types of Political Risks to Consider

Political risks generally fall into several key categories:

- Political violence: This includes threats like war, terrorism, civil unrest, strikes, and riots. Such events can lead to property damage or force operations to pause. For example, in 2025, Burkina Faso transferred five gold mining assets to a state-owned company, while Niger nationalized both a gold mine and a uranium mine previously run by foreign companies.

- Government interference: This involves actions such as expropriation, nationalization, or outright confiscation of assets, as well as policies favoring domestic businesses over foreign ones.

- Regulatory and legislative changes: Sudden legal requirements can disrupt business models. A case in point: Apple had to switch its iPhone 15 to a USB-C port in 2024 to comply with new European Union regulations.

- Currency and financial risks: These include restrictions on converting local earnings to U.S. dollars or transferring profits abroad.

- Trade disruptions: Embargoes, sanctions, tariffs, and import/export restrictions fall under this category. For instance, U.S. tariffs on Mexico and Canada in January 2025 affected over $1 trillion in global trade.

- Breach of contract: This occurs when government entities fail to honor agreements or arbitration rulings. In July 2024, the Russian Supreme Court barred enforcement of arbitration awards from countries deemed "unfriendly".

Understanding the distinction between macro risks (affecting an entire economy, like civil war) and micro risks (specific to industries, such as targeted tax changes) is critical for evaluating your exposure.

Properly categorizing these risks is the first step toward crafting a comprehensive strategy.

Assess Risks by Country and Region

A business’s geographic footprint plays a major role in its risk profile. Since 2005, the number of global conflicts has doubled, making regional assessments more important than ever. Tools like Marsh‘s World Risk Review can help by tracking economic, political, and security trends across 197 countries, providing comparative risk ratings.

Create a watchlist of high-risk locations where your business operates or plans to expand. For example, a border dispute between Thailand and Cambodia in 2025 caused Thai businesses to lose over $3 billion, disrupting supply chains for months. Additionally, nearly 40% of companies surveyed reported financial losses from Middle Eastern conflicts in 2024, largely due to supply chain issues.

To get a complete picture, map your entire supply chain – not just your direct operations, but also vendors, shareholders, and customers. Overlooking these connections can leave vulnerabilities exposed.

Consistent monitoring of geopolitical developments is key.

"Risk analysis is ongoing, not a one-time transaction. If you want to be ahead of the curve, a company’s considerations of the global political climate must be constantly evolving." – Erica Stieper, Manager, Professional Services, FiscalNote

Once regional risks are identified, the next step is to rank them based on their potential impact on your business.

Rank Risks by Business Impact

Not every risk requires the same level of attention. Focus on the top 20% of risks that could have the greatest impact on your business continuity. Assess each risk by its likelihood and potential severity. For example, rare but catastrophic events may demand more attention than frequent, low-impact issues.

Look at both short-term financial effects and long-term strategic challenges. A sudden tax change might hit your quarterly revenue, while evolving trade policies could force a complete restructuring over several years. Surveys show that 74% of globalized companies rank political risks among their top five concerns, with 11% naming it their number one issue. Additionally, 58% of businesses expected trade wars to negatively affect their operations in 2025.

Pay close attention to risks in regions with limited legal protections or where arbitration awards may not be enforced. Prioritizing risks in this way helps determine which require immediate insurance coverage and which can be managed through other strategies.

Step 2: Customize Coverage for Your Business

Once you’ve pinpointed and ranked your political risks, it’s time to shape your insurance to reflect the realities of your operations. Political risk insurance can be tailored to fit anything from short-term trade agreements to multi-decade projects.

Align Policies with Your Operations

Use your supply chain mapping from Step 1 to identify specific vulnerabilities in your industry. For instance, manufacturers relying on imports from key suppliers may face tariff risks.

To ensure your coverage aligns with financial goals, use objective standards to value potential losses. For currency inconvertibility claims, define the "date of loss" as the first instance where conversion fails.

If you’re working with foreign governments, include stabilization clauses and arbitration agreements in your host-country contracts. These measures can complement your insurance by providing additional recovery options. However, enforcement might be tricky in some regions. For example, a Russian Supreme Court ruling in July 2024 blocked arbitration awards from "unfriendly" countries.

Finally, consider layering your coverage to address both sovereign and commercial risks effectively.

Add Multiple Coverage Layers

A comprehensive approach often involves combining different types of insurance. Pairing Political Risk Insurance (PRI) with Trade Credit Insurance (TCI) is a good example. PRI covers sovereign risks like expropriation and war, while TCI safeguards against commercial risks, such as buyer insolvency or non-payment.

For goods traveling through politically unstable areas, add Strikes, Riots, and Civil Commotions (SRCC) endorsements to your cargo policies. These endorsements cover physical damage caused by political unrest during transit. You might also want to look into Supply Chain Insurance, which protects against financial losses from disruptions like port closures or tariff-related shortages – even when there’s no physical damage . This layered approach strengthens your overall protection.

"Political risk insurance generally safeguards companies against losses caused by political events or government actions… Trade credit insurance generally protects businesses… against losses arising from the failure of a buyer or debtor to fulfil its payment obligations." – Marsh

When bundling coverage, focus on the risks most relevant to your operations, such as expropriation, currency inconvertibility, contract frustration, or political violence. This way, you can balance costs while maintaining strong protection.

Optimize Cost and Coverage

Striking the right balance between cost and coverage is key. The global political risk insurance market generates around $2 billion in annual premiums. You can manage costs by adjusting deductibles (retention levels) and choosing a policy term that fits your risk profile. For instance, longer terms (10+ years) provide rate stability for infrastructure projects, while shorter terms (under 12 months) may be more affordable for trade finance deals.

Collaborating with specialists can also help refine your coverage. Accounts Receivable Insurance, for example, offers tailored policy designs and risk assessments, leveraging a global network of credit insurance carriers to identify gaps and optimize your strategy.

Ensure your policy language is clear and comprehensive. Expand the definition of "expropriation" to include creeping expropriation or discriminatory regulatory changes, not just outright nationalization . Additionally, remove "direct physical loss" requirements and broaden the definition of "dependent property" to include critical third-party suppliers.

"Potential policyholders must evaluate their needs carefully and be strategic during policy placement to ensure they are maximizing potential coverage." – Emily P. Grim, Attorney at Gilbert LLP

Step 3: Use Expert Resources and Assessment Tools

Once you’ve designed coverage tailored to your needs, the next step is refining your policy using expert resources and assessment tools. Political risk policies often involve intricate details, and since no universal policy form exists, working with experienced professionals is crucial. These experts can help you navigate complex terms and uncover hidden exclusions that could leave you vulnerable. Their guidance ensures your policy addresses your specific risk profile effectively.

Partner with Specialized Insurance Providers

Selecting the right insurance provider is key. Look for one with extensive experience in international trade insurance and a deep understanding of the markets you operate in. Providers like Accounts Receivable Insurance connect businesses with a global network of credit insurance carriers, including Ex-Im Bank, Allianz Trade, Coface, and Atradius. This network helps ensure you receive solutions tailored to your unique needs.

An experienced provider will also help you interpret ambiguous policy terms and identify potential pitfalls. For instance, they can clarify how "date of loss" is defined for currency inconvertibility claims. Rather than relying on a waiting period that could expose you to declining exchange rates, they may recommend defining it as the first moment conversion fails.

"Policyholders should make an aggressive assessment of policy language that reveals possible limitations while developing the most solid and likely arguments in favor of coverage." – Mark Garbowski, Anderson Kill

This collaboration lays the groundwork for thorough risk assessment and effective policy design.

Apply Risk Assessment Methods

A comprehensive risk assessment categorizes potential threats into clear groups: currency inconvertibility, transfer restrictions, government expropriation, political violence, and breach of contract. Your insurance provider should rely on objective standards or independent evaluations to estimate potential losses, rather than solely depending on insurer-led valuations.

Pay close attention to exclusions, such as "pre-existing condition" clauses. For example, in late 2021 and early 2022, the U.S. publicly announced potential sanctions months before implementing them. Broad interpretations of pre-existing condition clauses could exclude coverage for these well-known risks.

Political risk insurance can also enhance financial stability. By covering up to 90% of losses from political and commercial risks, as offered by Accounts Receivable Insurance, businesses can demonstrate reduced risk to lenders, potentially lowering borrowing costs .

Examples of Effective Policy Design

Real-world examples highlight the importance of precise policy design. When Russia invaded Ukraine, many companies found their coverage lacking. However, businesses that worked with specialized providers to expand expropriation definitions beyond outright nationalization were better protected. Their policies included coverage for "creeping expropriation", which accounts for subtle, discriminatory actions by governments. This proved invaluable as restrictions on foreign businesses gradually increased.

For companies operating in areas with shifting political boundaries, expert policy drafting is essential. Policies must account for losses caused by both host and foreign governments imposing sanctions. The complexity of U.S. sanctions on Russia, for example, underscores the need for a nuanced approach to how sanctions interact with political risk coverage.

"U.S. businesses can maximize the benefits of such coverage through careful policy drafting and strategic evaluation of their individual risk profile." – Emily P. Grim, Gilbert LLP

Step 4: Maintain and Update Your Policies

Managing political risk insurance isn’t a one-and-done process. The geopolitical landscape is always shifting, and your coverage needs to keep up. With regulatory changes in trade, finance, and digital infrastructure accelerating, neglecting regular updates could leave you exposed at the worst possible time.

By staying proactive with policy maintenance and updates, you can ensure your coverage remains aligned with the risks you face.

Track Political and Economic Developments

To stay ahead of potential threats, use real-time intelligence tools and set up a dedicated team to monitor geopolitical and legislative changes. Platforms like the World Risk Review provide insights into political, economic, and security trends across nearly 200 countries, helping businesses identify risks early on.

It’s also wise to create an internal political risk task force. This team can establish clear protocols for responding to emerging threats, ensuring key stakeholders are informed quickly. Building relationships with local officials, industry groups, and regional partners can provide invaluable firsthand information that complements data from risk platforms.

"An accelerating geopolitical transition is underway, ushering in an era of heightened and persistent complexity. While such a period may seem daunting, it should not lead to decision paralysis." – Angela Duca, Global Head Credit Specialties, Marsh

AI-driven tools can now process vast amounts of information – like bills, hearing transcripts, and news articles – in seconds. These tools are increasingly being used to track how industry narratives influence policy decisions, offering a layer of insight that manual monitoring often misses.

Review and Renew Coverage Regularly

Regular reviews are critical to ensure your policy remains comprehensive. Annual audits are a must. During these reviews, check how terms like "government" or "government authority" are defined and verify that the geographic scope aligns with current political realities, especially in conflict zones where control can shift quickly.

Pay close attention to exclusions for "pre-existing conditions." For example, in 2021 and 2022, companies without policies in place before the U.S. announced potential sanctions against Russia found themselves unable to file claims due to exclusions for restrictions that were "publicly known to be under consideration".

"Be wary of broader language that excludes restrictions that the policyholder ‘should have known about,’ or that targets proposed restrictions, or those ‘publicly known to be under consideration.’" – Mark Garbowski, Anderson Kill

Consider opting for multi-year, non-cancelable policies (ranging from 3 to 15 years) to maintain consistent coverage as political conditions evolve. During renewals, negotiate stabilization clauses to lock in regulatory or tax conditions as of the signing date, protecting your business against abrupt legal changes in host countries.

Also, map your supply chain – including Tier 1 and Tier 2 suppliers – against your policy. Make sure your coverage is aligned with potential disruptions at foreign locations. In 2023, 18% of surveyed global businesses reported political risk losses significant enough to require corporate earnings restatements.

Address New and Emerging Risks

New risks are always on the horizon, and your policy should adapt accordingly. For instance, in 2025, Burkina Faso and Niger nationalized major mining assets, underscoring the importance of monitoring government interference risks. Policies should include coverage for "creeping expropriation" and "forced divestiture" to address these types of situations.

Cyber threats have also become a major political risk. By 2026, 75% of small business owners identified cyber-related issues as a top concern, yet many still rely on general property or political risk policies to cover cyber events. This approach falls short when dealing with state-sponsored cyberattacks. Instead, look into standalone cyber policies to address these gaps.

"If you’re a small company thinking, ‘Well, I don’t really need a cyber policy, that’s for the big, global, intricate organizations,’ that is completely wrong." – Thaddeus Woosley, Executive Vice President, World Insurance Associates

It’s also crucial to monitor where citizen data is stored and governed. For example, in 2024, Apple changed the iPhone 15 to a USB-C port to comply with European Union regulations, showing how legislative changes can force significant product adjustments. Ensure your policy accounts for similar regulatory risks through specific endorsements or broader definitions.

Work closely with your insurance provider to model different geopolitical scenarios, such as military coups, regional unrest, or embargoes. Testing how your policy would respond to these situations can help identify potential gaps before they become costly issues, ensuring your coverage evolves as your risks do.

Conclusion: Build Complete Protection with Tailored Policies

Main Points for Policy Design

Creating effective political risk policies involves a focused approach built on four key steps:

- Identify your risks: Pinpoint the range of threats your business could face, from expropriation and political violence to currency issues and regulatory changes.

- Tailor your coverage: Align your policy with the specific needs of your operations and regions, as standard property insurance often doesn’t address political disruptions.

- Use expert tools and insights: Tap into resources like AI-driven tracking systems to simplify complex data and transform it into actionable strategies.

- Stay proactive: Establish early warning systems and regularly review your policies to account for new and emerging risks.

"Political risk policies likely cannot insulate U.S. companies from the full impact of a global trade war or other politically-inspired disruptions. However, U.S. businesses can maximize the benefits of such coverage through careful policy drafting and strategic evaluation of their individual risk profile." – Emily P. Grim, Attorney, Gilbert LLP

From geopolitical conflicts to nationalizations, recent events highlight the importance of having comprehensive coverage. These strategies lay the groundwork for managing risks effectively.

Action Steps for Your Business

To fortify your political risk policies, take these actionable steps:

- Audit your existing coverage: Check for gaps in definitions, exclusions, and geographic scope. Use broad, clear language for terms like "expropriation" and "government authority" to avoid restrictive interpretations.

- Map your supply chain: Include both Tier 1 and Tier 2 suppliers to ensure your policy accounts for disruptions across your entire network.

- Collaborate with specialists: Work with providers who understand political risk intricacies. For example, Accounts Receivable Insurance offers tailored solutions to protect against financial risks like non-payment, bankruptcy, and political instability. Their expertise in claims management and their global network of credit insurance carriers can help you craft policies suited to your specific vulnerabilities.

"Political risk insurance provides broad cover for losses from government action, political unrest, and economic turmoil." – Chubb

Take action now to strengthen your coverage. Assign accountability within your teams, develop clear protocols, and rely on real-time intelligence to anticipate geopolitical changes. By following these steps and maintaining flexibility, you can ensure your protection evolves with the risks you face.

FAQs

What losses does political risk insurance actually pay for?

Political risk insurance safeguards businesses and investors against losses stemming from political events that interfere with operations or investments in foreign countries. This coverage includes protection against government expropriation, political violence (such as war, terrorism, or riots), restrictions on currency transfers, sovereign payment defaults, and breaches of contract by government entities. Additionally, it extends to other government actions that could harm assets or disrupt trade activities.

How do I avoid policy exclusions like “pre-existing conditions” and narrow definitions?

When drafting a policy, it’s crucial to steer clear of pitfalls like "pre-existing conditions" or overly restrictive definitions. To do this, take the time to review and negotiate the terms carefully. Use clear and specific language to avoid misunderstandings. Collaborating with an experienced broker or legal advisor can help you customize the policy to suit your unique needs.

Make sure the coverage definitions are broad enough to address the risks you face. Additionally, don’t treat your policy as a one-and-done deal. Regularly revisit and update it, particularly before significant transactions, to reduce the risk of exclusions or unclear terms.

When should I layer political risk with trade credit, cargo SRCC, or supply chain coverage?

Layering political risk insurance with trade credit, cargo SRCC (Strikes, Riots, and Civil Commotion), or supply chain coverage can be an effective way to address the intertwined risks of international trade. For instance, combining these coverages can help safeguard against challenges like political unrest, payment defaults, or disruptions in the supply chain. This strategy allows for customized protection in complex situations, especially when one issue – like political instability – has the potential to escalate and impact trade credit or the smooth operation of supply chains.