Small and medium-sized businesses (SMEs) often face the risk of customers not paying invoices on time – or at all. Local credit insurance can help protect your business from these financial risks, especially when offering Net 30 or Net 60 payment terms. Here’s what you need to know:

- What It Covers: Credit insurance shields you from losses caused by customer insolvency, bankruptcy, or prolonged nonpayment (typically covering 75%-95% of unpaid invoices).

- Why It’s Useful: It helps stabilize cash flow, supports growth by enabling competitive payment terms, and can improve financing options by making receivables stronger collateral.

- Key Considerations:

- Assess Risks: Use the "5 Cs of Credit" (Character, Capacity, Capital, Collateral, Conditions) to evaluate your buyers and choose a policy that fits your business needs.

- Provider Reputation: Look for insurers with strong financial ratings, reliable claims handling, and dedicated account agents.

- Coverage Details: Understand what risks are covered (e.g., commercial vs. political risks) and ensure the policy aligns with your operations.

- Costs: Premiums typically range from 0.1%-0.4% of annual sales. Be mindful of co-insurance, deductibles, and potential hidden fees.

- Claims Process: Confirm timelines for acknowledgment, investigation, and payment. Keep thorough documentation to avoid delays.

- Additional Tools: Many insurers offer risk assessment tools, real-time monitoring, and debt collection services to help manage credit risks effectively.

- Customization Options: Policies can be tailored for specific industries or needs, such as Whole Turnover coverage or Single Buyer policies.

Choosing the right credit insurance provider can protect your business from financial disruptions, improve cash flow, and support growth. Use these guidelines to evaluate policies that work best for your SME.

SME Credit Insurance Selection Checklist: Key Factors and Red Flags

Key Factors to Consider When Choosing Local Credit Insurance

Assessing Business Risks and Coverage Needs

Before diving into policy comparisons, it’s essential to pinpoint the specific risks your small or medium-sized enterprise (SME) faces. One of the biggest concerns? Credit risk – the chance that your buyers might not pay what they owe.

To get a clearer picture of your buyers’ reliability, use the 5 Cs of Credit:

- Character: Look at their payment history and reputation.

- Capacity: Check their cash flow strength using metrics like the debt-to-income ratio (ideally 36% or less).

- Capital: Assess their financial reserves and overall net worth.

- Collateral: Identify any assets they can use to secure their debts.

- Conditions: Consider external influences, like economic downturns or industry-specific challenges.

When choosing a provider, look for one that actively monitors these factors and provides real-time insights into industry trends and broader economic shifts that might affect your buyers’ ability to pay. This kind of data can be a game-changer when evaluating policies and ensuring you’re working with a trustworthy insurer.

Evaluating Provider Reputation and Licensing

Once you’ve assessed your risks, the next step is finding a provider you can rely on. Instead of skimming through generic online reviews, focus on detailed client testimonials that specifically address claims handling and support for SMEs. These testimonials often provide a more accurate and reliable picture.

It’s also a good idea to gauge how responsive the provider is. Ask about their dedicated account agents – reputable companies will be more than happy to introduce you to your point of contact.

Don’t stop there. Look into the provider’s financial strength ratings and their track record for paying claims. Insist on transparency about the claims process, including clear timelines for when you can expect payment. Considering that nearly 20% of small businesses in the U.S. don’t make it past their first year, aligning with a financially stable insurer is critical.

Comparing Policy Coverage and Terms

When reviewing policies, pay close attention to the type of risks covered. Commercial risk typically protects against insolvency or prolonged non-payment, while political risk shields you from losses caused by government actions. Keep in mind that most policies won’t cover disputes over product quality or delivery – insurers usually only pay on amounts that aren’t in dispute.

"The policy coverage also needs to match how your business operates" – Jason Benson, Global Head of Structured Working Capital in Trade & Working Capital at J.P. Morgan

You’ll also want to ensure that the insurer’s credit management requirements align with your internal processes. If your team doesn’t have the capacity for heavy administrative work, this is something to factor into your decision. Additionally, confirm how the insurer evaluates your customers. Customizing the policy to fit your business operations can help protect you from unexpected financial disruptions.

sbb-itb-2d170b0

Understanding Costs and Premium Structures

Analyzing Premiums, Co-Insurance, and Deductibles

Credit insurance premiums typically fall between 0.1% and 0.4% of annual sales. For instance, a small business with $2 million in sales might pay around $5,000 (approximately 0.25%), while a larger company with $20 million in sales would likely pay under $50,000.

The final cost of your policy depends on factors like the stability of your industry, the creditworthiness of your customers, and how well you manage credit risk. If your business operates in a high-risk sector or works with customers who are financially unstable, you can expect higher premiums.

"If a company isn’t doing its due diligence, it may be purchasing more insurance than is otherwise needed, or its insurance may be more expensive than it should be."

- Jason Benson, Global Head of Structured Working Capital in Trade & Working Capital, J.P. Morgan

Most policies cover about 90% of the insured debt. This co-insurance structure ensures you retain some responsibility for managing credit risk. Opting for higher deductibles or lower co-insurance can reduce your premium, as it shifts more of the risk onto your shoulders.

It’s also important to examine additional fees and the renewal process, as these can impact your overall costs in the long run.

Factoring in Policy Renewal and Hidden Costs

While the base premium is the primary expense, additional fees can significantly influence your total costs. For example, if your standard policy limits don’t sufficiently cover your highest-risk customers, insurers may offer "CAP" or "top-up" products. These provide extra, limited coverage for those customers but come at an added cost. Some policies may also charge endorsement fees for faster decisions on smaller accounts.

Credit insurance is not a one-and-done purchase – it requires ongoing management. Insurers regularly adjust limits and terms based on the financial health of your customers. This means you’ll need staff to handle reporting requirements and maintain communication with your insurer.

When seeking quotes, provide detailed financial and receivables data to get a precise estimate. Initial quotes based on general information are not binding and can change significantly. Additionally, inquire about renewal terms upfront. Some policies include non-cancellable limits, which prevent the insurer from reducing coverage on specific customers during the policy term. While this feature offers stability, it may come with a different pricing structure.

Reviewing Claims Process and Support Services

Claims Handling Efficiency and Broker Assistance

The claims process generally unfolds in three stages: acknowledgment (within 15–30 days), investigation (30–60 days), and payment (within 30 days after settlement). However, specific timelines can vary depending on state regulations. Claims are typically triggered by "protracted default", which occurs when a payment remains overdue for a set period. Policies usually cover between 75% and 95% of the outstanding debt.

Working with a dedicated agent or broker can simplify this process significantly. As ARI Global emphasizes:

"Ideally, you’ll have access to a professional who can help you with the claim. This will streamline the process and reduce the stress you deal with".

To ensure smooth handling, confirm that your insurance provider assigns a dedicated agent to assist with claims. Additionally, maintaining thorough documentation – such as invoices, delivery confirmations, and written communications – is crucial. Referencing state prompt payment laws in your follow-ups can also help. Missing or incomplete records are a common reason for delays in claim settlements.

Beyond claims processing, insurers are enhancing their services with advanced tools designed to help businesses manage risks more effectively.

Access to Risk Assessment Tools and Local Credit Data

Top-tier insurers now provide risk assessment tools that help businesses avoid bad debts. These tools tap into extensive databases, offering insights like financial data, payment histories, and creditworthiness ratings for potential clients. Christian Bürger, Senior Editor at Atradius, highlights the value of these resources:

"With insurer-backed credit ratings, businesses avoid ad hoc decisions based on guesswork".

Many insurers integrate these tools into ERP or invoicing systems through APIs, delivering real-time alerts about changes in a customer’s financial health. This kind of continuous monitoring can be a game-changer, especially for smaller businesses that might lack the resources for an in-house credit risk team. Additionally, insurers often include debt collection services to help recover overdue payments and protect cash flow.

When choosing a provider, look for one that offers proactive digital monitoring, which goes beyond simply reacting to issues as they arise. Such tools can provide businesses with early warnings and actionable insights, helping them stay ahead of potential risks.

Customizing Coverage for SME Needs

Flexible Policies for Regional and Industry-Specific Needs

Small and medium-sized enterprises (SMEs) require insurance policies that align closely with their operations, whether they focus on local sales or manage international shipments. Some of the most common coverage options include Whole Turnover coverage (protecting all receivables), Single Buyer policies (designed for one high-risk account), and Excess-of-Loss coverage (safeguarding against catastrophic losses beyond a self-insured threshold). In 2023, Whole Turnover coverage made up 62.23% of the U.S. market share, highlighting its popularity among businesses with diverse customer bases.

Industry-specific add-ons also play a crucial role. For instance, manufacturing SMEs often need policies that bundle machinery breakdown and cargo insurance, while IT consultancies typically benefit from professional indemnity and electronic equipment coverage.

To support businesses with high customer concentration, some providers offer non-cancellable limits, ensuring stable financing streams. Gary Lorimer, Head of Business Development for Aon Credit Solutions, explains:

"It’s known as credit insurance, but it’s more opportunity protection."

With these flexible policy structures, SMEs can tailor their insurance to meet both regional needs and industry-specific demands.

Features of Accounts Receivable Insurance

Accounts Receivable Insurance (ARI) offers SMEs a way to simplify credit management and minimize risks, all while catering to local market conditions. For U.S. businesses, ARI (https://accountsreceivableinsurance.net) provides customizable options that address specific credit challenges. One standout feature is discretionary limits, which allow companies to trade up to a pre-set limit without needing individual approvals – as long as they follow established credit management practices or obtain a credit report. This feature empowers quicker decision-making for smaller accounts while maintaining adequate protection.

ARI covers both commercial and political risks, such as insolvency, protracted default, and export-specific issues like currency inconvertibility. Beyond the coverage itself, ARI offers additional tools such as built-in debt collection services and real-time buyer ratings, functioning like an external credit department for SMEs that lack in-house resources.

Another key advantage? Insured receivables can be used as collateral to secure loans, improving access to working capital and potentially lowering borrowing costs. For SMEs expanding into international markets, ARI’s export credit insurance safeguards against risks stemming from both commercial failures and political instability abroad.

What is Trade Credit Insurance? | Credit Insurance explained in 5 minutes

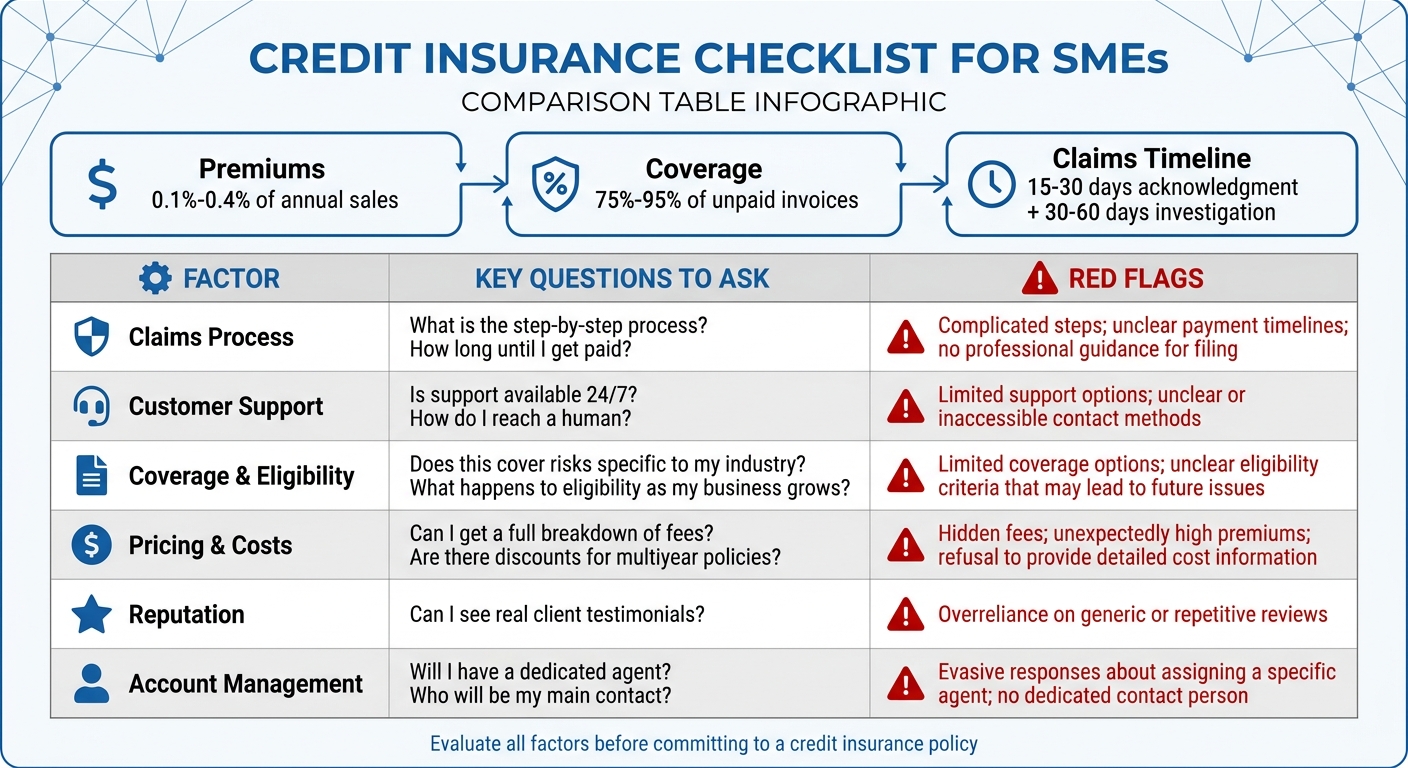

Checklist Summary Table

Use this table to double-check essential credit insurance considerations for your SME.

| Factor | Key Questions to Ask | Red Flags |

|---|---|---|

| Claims Process | What is the step-by-step process? How long until I get paid? | Complicated steps; unclear payment timelines; no professional guidance for filing. |

| Customer Support | Is support available 24/7? How do I reach a human? | Limited support options; unclear or inaccessible contact methods. |

| Coverage & Eligibility | Does this cover risks specific to my industry? What happens to eligibility as my business grows? | Limited coverage options; unclear eligibility criteria that may lead to future issues. |

| Pricing & Costs | Can I get a full breakdown of fees? Are there discounts for multiyear policies? | Hidden fees; unexpectedly high premiums; refusal to provide detailed cost information. |

| Reputation | Can I see real client testimonials? | Overreliance on generic or repetitive reviews. |

| Account Management | Will I have a dedicated agent? Who will be my main contact? | Evasive responses about assigning a specific agent; no dedicated contact person. |

This table highlights the critical factors to evaluate before committing to a policy. Each element listed above plays a vital role in ensuring the policy aligns with your business needs and risk profile.

Make sure to confirm pricing transparency and eligibility rules upfront to avoid surprises later. A clear fee breakdown is essential to ensure administrative costs don’t eat into your coverage. Pay close attention to providers that dodge questions about claims timelines or fail to offer a dedicated agent – these could signal potential delays or communication issues when you need assistance the most.

FAQs

Do I need whole-turnover coverage or a single-buyer policy?

When deciding between whole-turnover coverage and a single-buyer policy, it’s all about what works best for your business.

Whole-turnover coverage is designed to protect all your receivables, making it a great choice if you have a wide range of customers and want broad protection against risks. On the other hand, single-buyer policies are tailored for businesses that rely heavily on specific clients, offering focused protection for those key relationships.

To choose the right option, think about factors like the size of your receivables, how concentrated your customer base is, and how much a major customer default could affect your business. These considerations can help you find the coverage that aligns with your needs.

What invoices won’t a credit insurance claim pay for?

Credit insurance generally does not cover invoices linked to risks or events specifically excluded in the policy. This might include certain types of non-payment, instances of buyer insolvency that aren’t covered, or explicitly listed exclusions like particular hazards. It’s crucial to carefully review your policy details to fully understand what is included and what falls outside the scope of coverage.

How do I know if the premium is worth it for my business?

When deciding if the premium is worth it, think about how well the coverage matches your specific risks and potential financial vulnerabilities. Weigh the cost of the premium against the potential losses it could help you avoid. Important considerations include the extent of the coverage, the insurer’s reputation, and the unique risks your business faces.