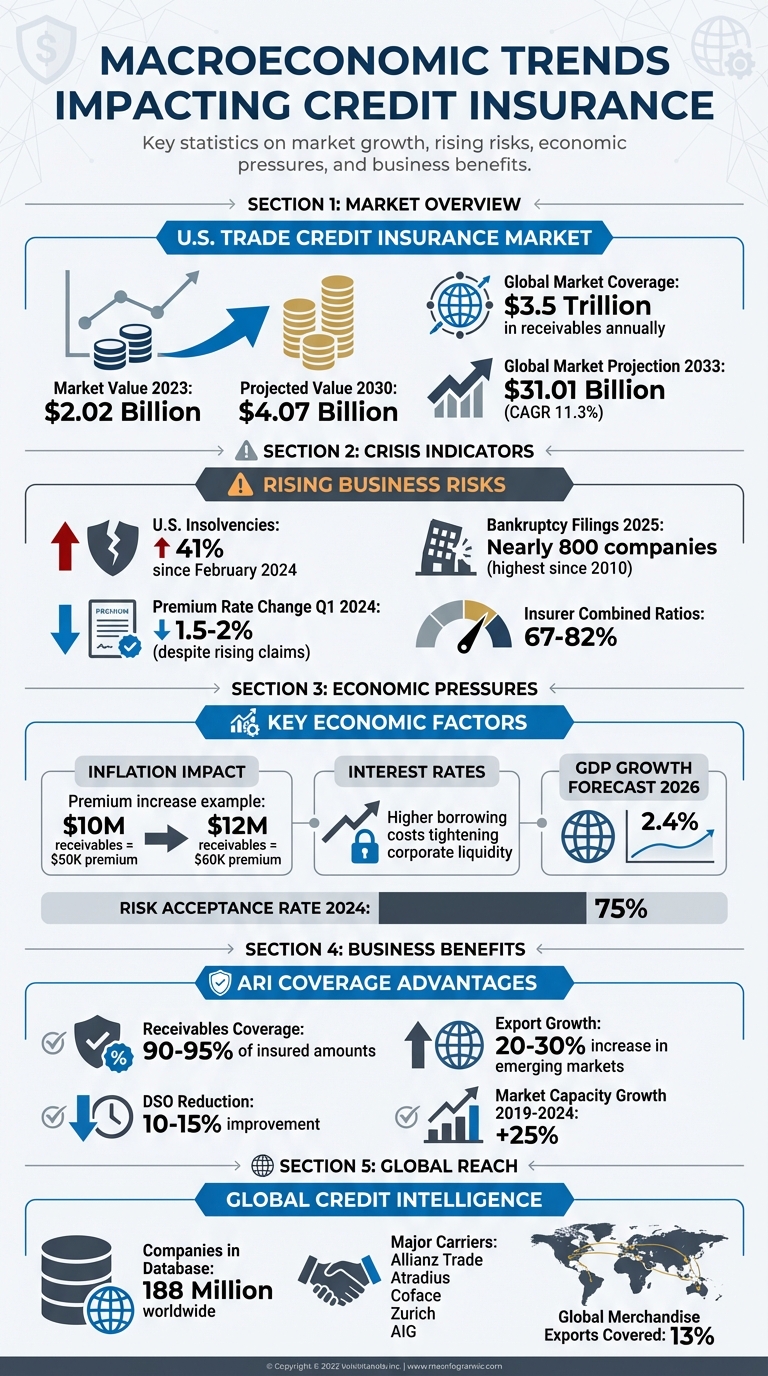

Credit insurance is becoming a critical tool for businesses in today’s volatile economy. With U.S. insolvencies up 41% since February 2024 and inflation pushing costs higher, companies are turning to trade credit insurance to protect against unpaid invoices and financial risks. The U.S. trade credit insurance market, valued at $2.02 billion in 2023, is projected to grow significantly as businesses face mounting challenges like rising interest rates, geopolitical tensions, and supply chain disruptions.

Here’s what’s driving the demand for credit insurance:

- Inflation: Higher trade receivables and operational costs are raising premiums, especially in vulnerable sectors like construction and retail.

- Interest Rates: Increased borrowing costs are tightening liquidity, making it harder for businesses to manage debt and cash flow.

- Bankruptcy Risks: Nearly 800 U.S. companies filed for bankruptcy in 2025, the highest since 2010, putting pressure on insurers and businesses alike.

- Geopolitical Uncertainty: Trade disruptions, tariffs, and political conflicts are reshaping global credit strategies, especially for international markets.

- Economic Cycles: During downturns, businesses seek credit insurance to shield against rising insolvencies. In growth periods, they use it to manage risks in new markets.

Credit insurance not only protects businesses from financial losses but also helps secure better lending terms, improve cash flow, and expand into new markets. With tailored policies and real-time risk insights, it’s an essential tool for navigating today’s economic uncertainties.

Key Macroeconomic Trends Impacting Credit Insurance in 2024-2026

How Inflation Affects Credit Insurance Costs

Inflation puts pressure on credit insurance pricing in multiple ways. As the value of trade receivables climbs due to inflation, businesses often face higher insurance costs – even when premium rates stay the same. This happens because premiums are calculated as a percentage of insured turnover. For example, a company with $10 million in receivables might pay $50,000 annually for coverage. If inflation pushes that volume to $12 million, the premium would increase to $60,000.

Higher Premiums Caused by Inflation

Inflation doesn’t just affect businesses – it also impacts insurers. Rising operational expenses, including costs for data analytics, risk assessments, and general operations, often lead insurers to adjust their pricing. Industries like construction and retail are hit harder, as they face increased vulnerabilities from higher energy and raw material costs. Despite this, competitive market conditions in Q1 2024 forced premium rates down by 1.5% to 2%, even as claims rose.

Construction and retail sectors are under particular scrutiny, as insurers have become more selective in these areas. Construction businesses are grappling with tighter margins due to rising material and energy costs, while retail suffers from reduced consumer spending. Nicolas Garcia, Group Commercial Director at Coface, highlighted the challenges:

"The level of uncertainty and the complexity has been at the highest level for at least the last decade. The tensions on the macro-economic and the political sides are huge".

Adding to the financial strain, higher premiums often coincide with an uptick in claims, as inflation increases the likelihood of business failures.

More Claims from Business Failures

Inflation also drives higher claim activity, further stressing the credit insurance system. In 2025, nearly 800 U.S. companies filed for bankruptcy – the highest number since 2010. Manufacturing and construction businesses, in particular, are struggling with rising input costs and tighter credit conditions. For manufacturers, energy price spikes can shrink margins, disrupt supplier payments, and create a ripple effect throughout supply chains.

Major trade credit insurers have reported combined ratios stabilizing between 67% and 82%, as claims activity has returned to pre-pandemic levels. The construction sector illustrates this trend clearly. Rising material costs, coupled with stricter credit conditions, have led to more business failures and insolvency-related claims. These challenges explain why insurers are becoming more cautious about the risks they underwrite, even as the overall market remains well-capitalized.

sbb-itb-2d170b0

Interest Rate Changes and Credit Insurance

Recent inflation-driven adjustments have led to fluctuating interest rates, which are now playing a key role in shaping the dynamics of credit insurance. These shifts significantly affect the U.S. business environment, altering how companies manage their cash flow and evaluate credit risks. When the Federal Reserve raises interest rates, borrowing costs climb, putting a strain on corporate cash flow and making it harder for businesses to manage their existing debt. This isn’t just an isolated issue – these financial pressures ripple across supply chains and customer networks, creating broader vulnerabilities.

Rising Interest Rates and Limited Liquidity

Higher interest rates have tightened corporate liquidity across the U.S., making the financial landscape even more challenging. As borrowing becomes more expensive, businesses face a dual challenge: they struggle to manage their own debt while also contending with customers who are under similar financial strain. James Dezell, SVP of Financial Risk Management at Lockton, highlighted this cascading effect:

"Higher interest rates have increased the cost of capital and tightened corporate liquidity".

This issue is particularly pronounced in industries like automotive parts, technology, and vehicle financing, where private credit pressures are creating a chain reaction of financial stress. These liquidity constraints are a contributing factor to the rising bankruptcy rates seen in U.S. markets. In response, credit insurance has emerged as a strategic tool for businesses. By using trade credit insurance, companies can secure better lending terms from banks, such as larger credit lines or lower interest rates, as the insurance coverage reduces the risk of default.

Changes in Underwriting and Claims

With liquidity challenges mounting, insurers have adjusted their underwriting standards and claims management practices to align with the current economic environment. Insurers are now more selective about the risks they take on, particularly in high-risk sectors like retail, construction, and transportation. Despite the heightened bankruptcy risks, the trade credit insurance market remains competitive, with over a dozen major carriers actively seeking new business. This competition has spurred the development of flexible program structures and innovative underwriting methods that were less common in past economic cycles.

To navigate these complexities, insurers are leveraging technology such as AI, machine learning, and real-time analytics to identify early warning signs – like a customer facing secondary pressures from tariffs or private credit issues. Claims activity, meanwhile, has returned to historic norms. Businesses are also finding ways to optimize their trade credit insurance policies, such as negotiating better terms through multi-line insurer relationships or excluding low-risk customers from coverage to reduce premium costs in this high-interest-rate environment.

GDP Growth and Credit Insurance Demand

The relationship between GDP growth and credit insurance demand is closely tied to economic conditions. When GDP contracts, companies often seek credit insurance to shield themselves from rising insolvencies. Conversely, during periods of economic growth, businesses face new risks as they expand into unfamiliar markets, creating a need for tailored credit protection.

Credit Insurance Demand During Economic Cycles

Credit insurance plays a critical role during economic downturns. When GDP shrinks and insolvencies rise, businesses turn to credit insurance to safeguard their finances against customer defaults. Historical data illustrates this countercyclical trend, as bankruptcy rates tend to spike during such periods. For context, the U.S. GDP growth forecast for 2026 stands at 2.4%, yet bankruptcy filings are expected to remain high, according to S&P Global Market Intelligence.

In times of economic expansion, the demand for credit insurance shifts rather than diminishes. As businesses venture into new markets, they encounter unfamiliar credit risks, which heightens the need for protection. Offering competitive terms in these scenarios often increases exposure to payment defaults. This is reflected in the projected growth of the global trade credit insurance market, expected to reach $31.01 billion by 2033, with a CAGR of 11.3% from 2026 to 2033. Currently, insurers collectively cover over $3.5 trillion in receivables annually, representing about 13% of global merchandise exports. These trends highlight the evolving role of credit insurance in supporting businesses through both challenges and opportunities.

U.S. Infrastructure Spending and Insurance Opportunities

Beyond cyclical demand, infrastructure investments are creating new opportunities for credit insurance providers. Significant spending on technology and artificial intelligence is expected to contribute to U.S. GDP growth in 2026, opening up fresh avenues for insurers. These advancements not only boost economic output but also generate industries that require specialized credit protection.

"Trade credit insurers are actively pursuing new business in this competitive environment, with more than a dozen carriers offering meaningful capacity".

- James Dezell, SVP of Financial Risk Management at Lockton

In response to these shifts, insurers are adopting more flexible approaches. For instance, businesses can now exclude low-risk, financially stable customers from their policies, reducing premium costs while focusing on higher-risk accounts. This strategy is particularly beneficial in fast-growing sectors like life sciences, where companies face significant concentration risks as they scale. For small and medium-sized enterprises (SMEs), credit insurance offers additional benefits, such as reducing Days-Sales-Outstanding (DSO) by 10–15%, which enhances cash flow during periods of growth.

Geopolitical Risks and Trade Credit Insurance

Geopolitical risks add a layer of unpredictability to trade credit insurance, going beyond factors like inflation, interest rates, and GDP growth. Global trade disruptions have introduced new challenges for businesses operating internationally. Political tensions, supply chain issues, and evolving trade policies are reshaping how companies evaluate and manage credit risks.

Tariffs and Trade Barriers

Trade restrictions and tariffs are increasing the likelihood of non-payment from foreign buyers, pushing companies to rethink their international credit strategies. Events like the Ukraine war, the Gaza crisis, and ongoing Iran-US-Israel tensions have put the trade credit insurance market to the test. These disruptions ripple through global supply chains, leaving businesses exposed to sudden payment defaults.

The effects of these challenges vary across industries. For instance, sectors like construction and retail have seen higher insolvency rates in recent years, leading insurers to tighten their underwriting standards. Despite this, major carriers maintained risk acceptance rates near 75% in 2024, while also adjusting capacity requirements to handle the uncertainty.

Protectionism has become a key factor driving demand for trade credit insurance. As businesses face greater risks of non-payment from international buyers, they are increasingly turning to insurance to safeguard their receivables. Between 2019 and 2024, the market capacity for trade credit insurance expanded by 25%, even as economic activity remained stagnant in 2023. Insurers now need to adapt quickly to shifting trade policies and broader geopolitical uncertainties.

Managing Political and Economic Uncertainty

Trade credit insurance provides businesses with a safety net, ensuring payment even in the face of political instability or currency fluctuations. Insurers rely on economic intelligence and industry-specific risk analysis to help companies anticipate market volatility driven by geopolitical changes. Andreas Tesch, Chief Market Officer at Atradius, highlights the industry’s ability to adapt:

"I think the last couple of years have proven that the trade credit industry is resilient and is providing stable coverage despite crises like COVID, the Ukraine war and Gaza".

To keep pace with these uncertainties, insurers are integrating real-time data tools. For example, API portals now grant instant access to credit data on over 188 million companies, empowering credit managers to make well-informed decisions about their international partners. This digital transformation enables businesses to react swiftly to shifts like currency fluctuations, regulatory changes, or sudden political events that could lead to payment defaults.

Using Accounts Receivable Insurance for Risk Management

Accounts Receivable Insurance (ARI) plays a crucial role in navigating the challenges posed by inflation, fluctuating interest rates, and GDP shifts. When economic instability threatens cash flow, ARI steps in to protect businesses by covering 90–95% of insured receivables against risks like buyer insolvency, delayed payments, or political disruptions. This coverage acts as a financial buffer, helping businesses maintain liquidity and sustain operations, especially during downturns when bank lending tightens.

But ARI isn’t just about safeguarding payments – it also provides businesses with actionable risk intelligence. Insurers offer real-time insights into buyer reliability and sector-specific risks, empowering companies to make smarter decisions about extending credit. This becomes especially critical during periods of rising interest rates and slower GDP growth, conditions that often increase the likelihood of business failures in vulnerable sectors like construction and retail.

From a financial perspective, ARI enhances cash flow management by transforming receivables into assets that banks recognize, potentially reducing Days Sales Outstanding (DSO) by 10–15%. This improved cash flow can strengthen relationships with lenders, lower bank capital requirements under Basel III regulations, and lead to better borrowing terms. Additionally, businesses with ARI coverage often expand exports by 20–30%, particularly in emerging markets where securing collateral can be a challenge.

Tailored Policies for Specific Business Risks

ARI policies are designed to address the unique risks businesses face during economic turbulence. Companies can opt for Whole Turnover Coverage, which insures their entire debtor portfolio, or Single Buyer Coverage, which focuses on high-value transactions with specific customers. Whole turnover policies are generally more cost-effective per unit of coverage and support broader credit management strategies. Meanwhile, single buyer policies offer targeted protection, particularly useful for safeguarding against a specific customer’s payment default.

This flexibility is especially valuable when businesses venture into new or uncertain markets. For example, a company entering an international market might use single buyer coverage to protect against a major customer’s default while leveraging the insurer’s data to assess potential partners before extending credit. These policies also adapt to changing market conditions, such as supply chain disruptions or sudden shifts in buyer behavior, ensuring businesses remain protected. Moreover, they integrate seamlessly with a global network of carriers, providing a robust shield against macroeconomic volatility.

Access to Global Credit Insurance Carriers

One of the standout benefits of ARI is its connection to a global network of leading carriers, including Allianz Trade, Atradius, Coface, Zurich, and AIG. This international reach ensures coverage across multiple jurisdictions and access to extensive risk assessment tools. For instance, in September 2023, Coface introduced an API portal offering real-time data on 188 million companies worldwide, allowing credit managers to incorporate this intelligence directly into their systems.

In addition to risk assessment, this network offers specialized services like debt collection and dispute resolution, which help businesses recover outstanding payments without damaging commercial relationships. A noteworthy example is the August 2025 partnership between India’s M1xchange and Tata AIG, which integrated trade credit insurance into the TReDS platform. This collaboration improved risk protection for financiers and provided micro, small, and medium enterprises (MSMEs) with secure access to working capital despite global economic challenges. These partnerships highlight how insurers continuously evolve their offerings to address market-specific needs while maintaining high risk acceptance rates – currently at about 75%, even amid economic uncertainty.

Conclusion

The economic outlook for 2026 brings a mix of challenges and opportunities for U.S. businesses. Rising inflation, higher interest rates, and a 41% increase in insolvencies are creating significant pressure on cash flow. On the flip side, a moderate 2.4% GDP growth and reduced trade uncertainty offer some room for businesses to navigate these hurdles. In this environment, having strong credit risk management tools is more important than ever.

Accounts Receivable Insurance (ARI) has emerged as a key tool for businesses looking to safeguard their financial health. Covering 90–95% of insured receivables against defaults, ARI acts as a buffer against financial shocks, especially during times when bank lending tightens. It also helps businesses secure better credit terms by transforming receivables into bankable assets, which is particularly valuable in a climate of higher borrowing costs.

The growing importance of ARI is reflected in the U.S. trade credit insurance market, which was valued at $2.02 billion in 2023 and is expected to reach $4.07 billion by 2030. This market growth highlights the increasing reliance on proactive risk management. As industry experts point out, today’s business environment is more complex and uncertain than ever before. Businesses that use ARI’s customized policies, global carrier networks, and real-time risk insights can turn these uncertainties into opportunities – reducing Days-Sales-Outstanding by 10–15% and increasing export participation by 20–30%.

From sector-specific challenges in construction and retail to geopolitical disruptions and high-value customer risks, businesses can no longer afford to overlook proactive risk management. In these turbulent times, credit insurance – backed by tailored solutions and up-to-the-minute risk intelligence – remains a critical foundation for long-term resilience.

FAQs

How do inflation and higher receivables raise my premium?

Inflation and higher receivables lead to premium increases because they amplify the risk of non-payment and credit losses. To manage this added risk, insurers adjust premiums, ensuring they have the resources to handle potential claims efficiently.

Can credit insurance help me secure better bank financing?

Yes, credit insurance can make it easier to secure better financing from banks. By safeguarding your accounts receivable and mitigating risks like nonpayment or customer insolvency, it strengthens your business’s financial position and credit profile. Banks often view businesses with credit insurance as less risky, which can lead to more favorable loan terms or increased access to credit lines. This advantage becomes especially important during uncertain economic times when minimizing financial risks is crucial.

What geopolitical risks can credit insurance cover abroad?

Credit insurance provides businesses with a safeguard against geopolitical risks that can interfere with international trade. These risks include war, revolutions, asset expropriation, currency inconvertibility, and government actions like imposing import/export restrictions or canceling licenses. For example, export credit insurance protects companies from losses caused by non-payment due to political turmoil, helping maintain financial stability and keeping global trade moving, even in uncertain times.