Interest rates are reshaping credit insurance worldwide, with businesses and insurers facing unique challenges in different regions. Here’s what you need to know:

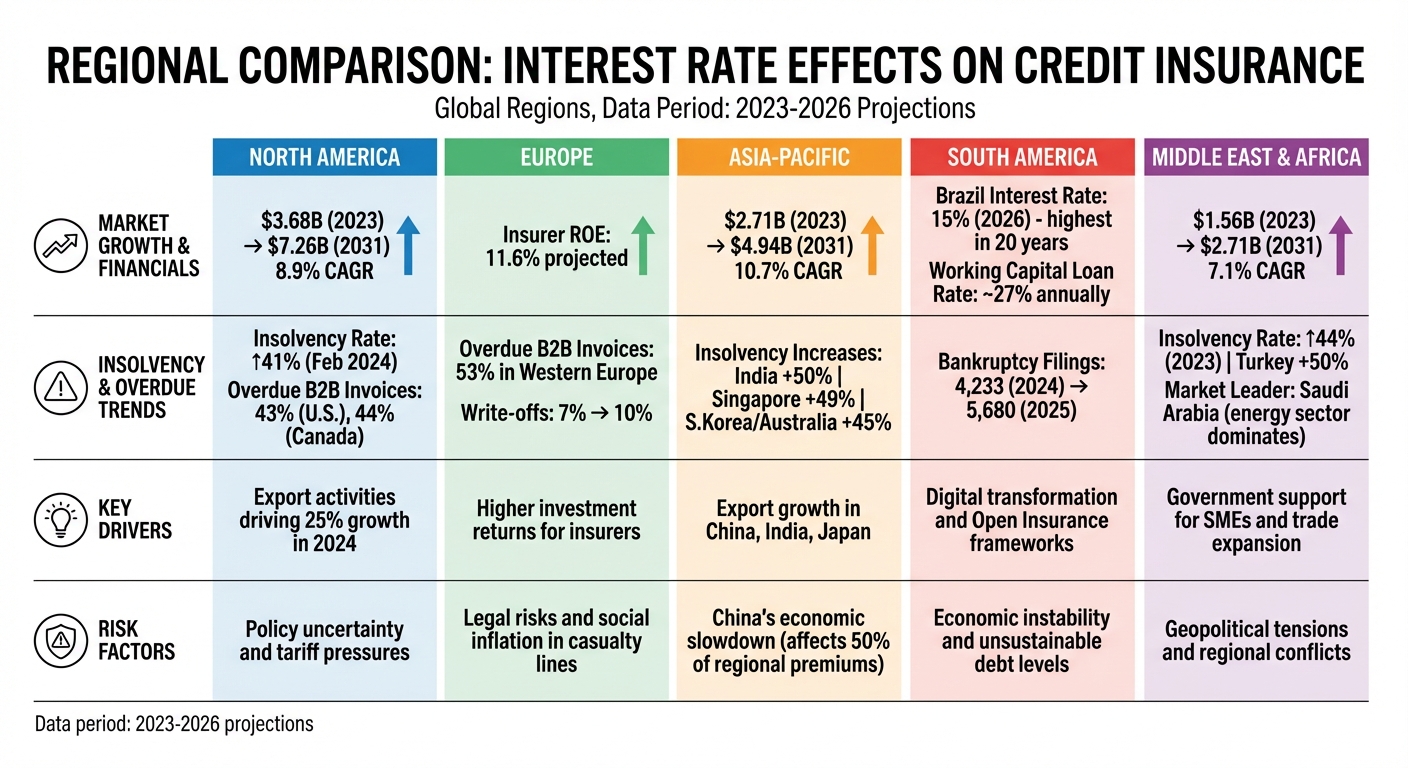

- North America: High rates are driving demand for credit insurance. Insolvency rates jumped 41% in early 2024, and overdue B2B credit sales reached 43% in the U.S. by 2025. The market is projected to grow from $3.68 billion in 2023 to $7.26 billion by 2031.

- Europe: Rising rates have boosted insurer returns but increased non-payment risks. Over 53% of B2B invoices were overdue in some areas, and write-offs climbed to 10%.

- Asia-Pacific: Credit insurance is expanding, especially in export-heavy economies like India and China. Insolvency rates rose sharply in 2024, with growth driven by SMEs and export markets.

- South America: Brazil’s 15% interest rate in 2026 led to unsustainable debt levels and a spike in bankruptcies, increasing reliance on foreign credit insurers.

- Middle East & Africa: Credit insurance markets are growing, driven by a 44% rise in insolvencies in 2023 and government support for SMEs.

Key takeaway: Rising interest rates are increasing financial risks globally, pushing businesses to use credit insurance to protect cash flow and receivables. Tools like Accounts Receivable Insurance can help businesses navigate these challenges effectively.

Federal Reserve and Interest Rates – Atradius Trade Credit Insurance

sbb-itb-2d170b0

North America: Rising Interest Rates and Credit Insurance Demand

In the U.S. and Canada, credit insurance is seeing a surge in demand as businesses contend with the challenges posed by persistently high interest rates. When borrowing becomes more expensive, companies often experience tighter cash flows and an increased risk of defaults, even when sales remain steady. This financial strain has significantly influenced the North American trade credit insurance market, which grew from $3.68 billion in 2023 to a projected $7.26 billion by 2031, marking an annual growth rate of 8.9%. Insolvency rates have also jumped by 41% as of February 2024, further amplifying non-payment risks for smaller suppliers struggling to collect from debt-laden customers. Additionally, overdue B2B credit sales reached 43% in the U.S. and 44% in Canada by 2025, with bad debts making up around 5% and 6% of long-outstanding invoices, respectively. These financial pressures highlight the inflation-driven changes in credit management, discussed further below.

How Inflation Drives Credit Insurance Adoption

Inflation has reshaped how businesses handle receivables. Rising operational costs and higher borrowing rates have squeezed profit margins, making unpaid invoices a significant threat to liquidity. As financing becomes more expensive, businesses are increasingly turning to credit insurance as a way to shield their balance sheets.

Credit insurance provides more than just protection – it also includes access to real-time payment data on potential partners, enabling businesses to make smarter credit decisions before extending terms. This is especially critical given that 50% of Canadian companies expect insolvency risks to worsen through 2026. Moreover, insured receivables can improve a company’s standing with lenders, often leading to better borrowing terms, a crucial advantage in today’s high-interest environment.

In 2023, COFACE SA introduced URBA360, an online risk management platform tailored specifically for North American businesses. This tool combines business reports, financial data, and economic briefings to deliver a clear, visual understanding of financial risks. By identifying vulnerabilities linked to high interest rates, URBA360 helps businesses choose appropriate coverage levels. Tools like these underline the growing demand for advanced credit risk management solutions in a challenging economic climate.

25% Growth Forecast for Trade Credit Insurance

Trade credit insurance growth isn’t just about managing internal risks – it’s also fueled by increasing export activities. As the President of Coface North America noted:

"Trade credit insurance is expected to grow by 25% in 2024 due to growing export activities in the region".

The energy sector currently dominates the North American trade credit insurance market. In Canada’s transport sector, for example, 64% of B2B sales are now conducted on credit. Similarly, the U.S. agri-food sector is facing growing financial strain, with 53% of firms anticipating higher insolvency risks by 2026. These concerns mirror the impact of elevated borrowing costs on business solvency.

For companies navigating these economic challenges, solutions like Accounts Receivable Insurance offer tailored protection against risks such as non-payment, bankruptcy, and political instability – both domestically and internationally. With interest rates expected to remain high through 2026, securing receivables has become a necessity for maintaining stable working capital.

Europe: Interest Rate Changes and Regional Differences

Europe’s credit insurance landscape reacts differently to interest rate changes, with notable variations across countries. These shifts impact both insurers and businesses seeking coverage, with effects ranging widely depending on the region.

Higher Investment Returns for Insurers

Rising interest rates have led to better investment returns for European insurers. As rates climbed during 2022 and 2023, insurers enjoyed higher yields on new investments. However, older long-term assets have faced unrealized losses, averaging around 30% of book equity by late 2023.

Germany’s non-life insurance sector stands out, benefiting from strong pricing momentum. This allows insurers to adjust premium rates to counterbalance claims inflation and increased reinsurance costs. According to S&P Global Ratings:

"European life insurers maintain solid margins but must offer attractive products while managing rising reinvestment rates, unrealized losses on long-term bonds, and falling short-term interest rates, which strain profitability".

Despite challenges, 82% of insurance ratings across Europe maintained a stable outlook as of early 2026.

While higher rates improve investment returns, they also elevate credit risks for businesses.

Increased Non-Payment Risks Across Markets

Rising interest rates have heightened non-payment risks for businesses across Europe, though the extent varies by region. In Western Europe, 53% of B2B invoices were reported overdue during times of economic strain. Additionally, write-offs for uncollectible receivables rose from 7% to 10%.

Italy has proven to be particularly vulnerable, experiencing the sharpest drop in coverage rates following the 2022-2023 interest rate hikes – more pronounced than in Germany or France. Meanwhile, Central and Eastern Europe are preparing for a wave of insolvencies. In these regions, 60% of companies anticipate increased insolvencies over the next year, especially among financially weaker firms in sectors like manufacturing and construction.

Businesses have responded decisively to these challenges. In Western Europe, 90% of businesses have adopted measures to mitigate liquidity risks caused by late payments. Notably, 56% expressed a preference for outsourcing credit risks through trade credit insurance rather than managing these risks internally. For U.S. companies operating in Europe, adapting credit risk strategies to reflect these regional differences is crucial. Solutions such as Accounts Receivable Insurance can help address these challenges and align risk management with the unique dynamics of each market.

Asia-Pacific: Credit Insurance Growth in Export Markets

The trade credit insurance market in the Asia-Pacific region is experiencing rapid growth, climbing from $2.71 billion in 2023 to a projected $4.94 billion by 2031. This surge is being driven by export-heavy economies such as China, India, and Japan, even as rising interest rates reshape the landscape of business financing.

Trade Expansion in Emerging Markets

As international trade grows, businesses increasingly turn to credit insurance for protection. The Asia-Pacific trade credit insurance market is expected to expand at a compound annual growth rate (CAGR) of 10.7% through 2033, with China leading the market share. India, however, is projected to see the fastest growth, thanks in part to government initiatives encouraging small and medium enterprises (SMEs) to safeguard against payment defaults.

The risk of business insolvencies is a key factor driving this trend. In 2024, insolvency rates were expected to rise significantly – by 50% in India, 49% in Singapore, and 45% in South Korea and Australia. Reflecting this, 42% of businesses in the region have increased their reliance on credit insurance. Amanda Best, Client Manager at Lockton, highlights the evolving focus of the market:

"The trade credit insurance market is less about guarding against sudden collapse and more about credit quality, cash discipline and selective risk differentiation".

Regulatory changes are also playing a role. For example, updated guidelines from the Insurance Regulatory and Development Authority of India (IRDAI) in November 2021 have made it easier for financial institutions to manage non-payment risks, further encouraging SMEs to adopt credit insurance. However, rising financing costs add complexity to this export-driven growth, affecting both risks and profit margins.

Rising Financing Costs and Market Effects

Higher interest rates are creating a mixed impact across the region. On one hand, businesses face increased debt servicing costs and tighter profit margins. On the other hand, insurers benefit from these higher rates, as they can invest in fixed-income assets with better yields. This dynamic is fueling demand for credit protection.

The automotive sector currently holds the largest share of trade credit insurance in the Asia-Pacific region. At the same time, technology sectors – particularly those focused on semiconductors and AI-related products – are seeing strong export demand. In India, real estate transactions accounted for a notable portion of private credit deals in the first half of 2025.

Payment behaviors across the region differ significantly. For example, 39.0% of B2B invoices in India were reported as overdue, compared to just 13.2% in Japan. For U.S. businesses looking to expand into Asia-Pacific markets, understanding these shifts is crucial. Tools like Accounts Receivable Insurance can help navigate the risks involved in cross-border trade.

South America and Middle East & Africa: Regional Challenges

South America and the Middle East & Africa face distinct hurdles tied to economic instability. In both regions, businesses are increasingly turning to credit insurance as a safeguard against financial uncertainty.

Economic Instability in South America

Skyrocketing interest rates are creating tough conditions for businesses in South America. Take Brazil, for instance – its central bank raised rates to 15% in early 2026, the highest in two decades. This has led to what Salvatore Milanese, Founding Partner at Pantalica Partners, calls unsustainable debt levels:

"With Brazil’s typical interest rate level, which is still very high, a company cannot have debt greater than twice its cash generation. If the debt exceeds that threshold, the company will inevitably have to renegotiate with its creditors."

The numbers tell the story. Bankruptcy filings in Brazil jumped from 4,233 in 2024 to 5,680 in 2025. Major companies are scrambling to adapt. In March 2026, Raízen – a joint venture between Cosan and Shell – sought out-of-court restructuring to manage its 65 billion reais (US$12.5 billion) in debt. Around the same time, Grupo Pão de Açúcar (GPA), one of Brazil’s largest supermarket chains, began restructuring to tackle 4.5 billion reais in non-operational debt. Meanwhile, industrial conglomerate CSN announced plans in January 2026 to sell assets worth 18 billion reais – half its total debt – to cope with the financial strain.

The cost of borrowing locally is steep, with working capital loans carrying annual rates of about 27%. As a result, Brazilian importers are increasingly relying on foreign credit insurers like Sinosure to secure deferred payment terms. This trend highlights the growing demand for credit insurance, particularly in industries like agricultural commodities and consumer goods, where the risk of non-payment has become more pronounced.

The Middle East & Africa, while facing its own economic challenges, is also seeing a surge in credit insurance adoption.

Growing Credit Insurance Markets in Middle East & Africa

Despite economic headwinds, the trade credit insurance market in the Middle East & Africa is on a growth trajectory. Valued at US$1.56 billion in 2023, the market is expected to hit US$2.71 billion by 2031, with a compound annual growth rate of 7.1%. Saudi Arabia leads the region in market share, with the energy sector being the largest consumer of credit insurance.

Rising business insolvencies are a key driver of this growth. The region’s insolvency rate surged by 44% in 2023, with Turkey alone seeing a jump of over 50%. High inflation and elevated interest rates are compounding financial risks. In response, governments are encouraging Micro, Small, and Medium Enterprises to adopt trade credit insurance as a way to improve financing options. Additionally, advancements like AI-powered underwriting and cloud-based technologies are making credit insurance more accessible and efficient.

Highlighting the industry’s adaptability, Andreas Tesch, Chief Market Officer at Atradius, stated:

"I think the last couple of years have proven that the trade credit industry is resilient and is providing stable coverage despite crises like COVID, the Ukraine war and Gaza."

For U.S. businesses eyeing opportunities in these markets, tools like Accounts Receivable Insurance offer essential protection against the heightened risks of non-payment in economically volatile regions.

Regional Comparison of Interest Rate Effects

Global Credit Insurance Trends by Region: Interest Rate Impact 2024-2026

Interest rate changes don’t hit every region the same way. Local economies, market maturity, and structural differences all play a role in shaping how these shifts play out. Understanding these nuances is key to optimizing receivables protection strategies.

Here’s a breakdown of how interest rate fluctuations impact major regions:

Regional Impacts Table

| Region | Key Study Insight | Demand Growth Driver | Risk Factor |

|---|---|---|---|

| North America | Combined ratios are expected to reach 99% by 2026. | Yield changes tied to underwriting margins, with a 4.2% forecast. | Policy uncertainty and potential tariff-related cost pressures. |

| Europe | ROE projected to climb to 11.6%, driven by lower cost pressures. | Favorable financial markets boosting demand for unit-linked products. | Increasing legal risks and social inflation in casualty lines. |

| Asia-Pacific | 69% of insurers are raising private credit allocations. | Emerging market trade growth and mobile tech adoption for micro-insurance. | China’s economic slowdown impacting 50% of regional premiums. |

| South America | "Open Insurance" frameworks are driving competition. | Digital transformation and API-based integrations. | Economic instability and tighter risk appetites from global insurers. |

| Middle East & Africa | Markets are shifting toward stricter risk management by 2025. | Expansion of trade credit in emerging hubs and growing middle markets. | Rising geopolitical tensions and regional conflicts. |

In more developed markets like North America and Europe, rising interest rates are increasing investment yields. For example, U.S. insurers are expected to see yields grow from 3.9% in 2024 to 4.2% by 2026. This boost helps offset tightening underwriting margins, offering some financial stability.

On the other hand, emerging markets face heightened risks from rising borrowing costs. This makes region-specific risk management critical.

The Asia-Pacific region tells a mixed story. While 69% of insurers are focusing on private credit to capture higher returns, the economic slowdown in China looms large, impacting half of the region’s insurance premiums. This underscores the region’s sensitivity to China’s broader economic health.

Tailoring credit protection to these regional dynamics is essential. For U.S. businesses, leveraging Accounts Receivable Insurance can provide targeted solutions to navigate these varied risks effectively.

Key Findings and Future Outlook

Research Findings Summary (2024–2026)

Recent studies reveal a noticeable shift in how businesses approach risk management, moving from broad defensive strategies to more selective, targeted measures. Global economic growth is projected at 2.9%, while the U.S. GDP is anticipated to grow by 2.4%. Rising interest rates are reshaping risk profiles across various industries, creating both opportunities and challenges.

"The trade credit insurance market is less about guarding against sudden collapse and more about credit quality, cash discipline and selective risk differentiation."

– Lockton

The data highlights clear sectoral differences. High-growth areas like technology, AI, and healthcare are seeing significant benefits from a $37 billion-plus data center pipeline. On the flip side, industries sensitive to interest rates – such as construction, building materials, and consumer durables – are under pressure due to higher debt servicing costs. The automotive sector is also struggling, weighed down by the costs of transitioning to electric vehicles and exposure to tariffs.

Although insolvencies are expected to increase by 2026, the pace will likely be moderate, indicating a late-cycle adjustment rather than a widespread economic crisis. In Australia, inflation is projected to stay above central bank targets for much of the year, delaying potential rate cuts. This will continue to strain mid-market businesses, particularly those already dealing with tight margins. These findings underline the need for strategic adjustments, especially for U.S. businesses navigating these challenges.

Recommendations for U.S. Businesses

Given these trends, U.S. companies need to rethink their credit strategies. Instead of relying on general market trends, businesses should focus on buyer-specific credit profiles, as 2026 will bring selective credit stress that varies by sector. For companies tied to construction or consumer durables, specialized coverage will be essential to manage the challenges posed by ongoing high borrowing costs.

Trade credit insurance can play a crucial role in managing working capital. With 52% of U.S. B2B sales conducted on credit, and 25% of businesses planning to adopt trade credit insurance for protecting receivables, this strategy can reduce risks and administrative burdens. In fact, 55% of companies report higher costs when managing credit risk internally.

Maintaining a close watch on cash flow and working capital will remain critical. The combination of strong stock market performance and continued investment in AI is expected to support U.S. credit markets. Tools like Accounts Receivable Insurance offer tailored solutions to help businesses address these challenges effectively, ensuring they remain resilient in a shifting economic landscape.

FAQs

How do higher interest rates increase non-payment risk?

Higher interest rates can increase the risk of non-payment by creating market instability, reducing asset values, and causing liquidity problems. These challenges can make financial products less attractive and raise the chances of defaults. On top of that, businesses often encounter stricter credit conditions, adding to financial pressure and making defaults more likely.

Which regions are seeing the fastest credit insurance growth?

Europe is experiencing the quickest expansion in credit insurance, with the European Union leading the charge. In 2022, the EU made up a substantial 73% of total insured exposure, showcasing its dominant role in this growth. Additionally, businesses outside the EU in Europe also played a notable part in driving this upward trend.

How can credit insurance improve borrowing terms with banks?

Credit insurance can play a key role in securing better borrowing terms with banks. By mitigating the risk of non-payment, it provides lenders with added confidence. This reduced risk can lead to benefits like lower interest rates or access to higher credit limits, making financing more favorable for businesses.