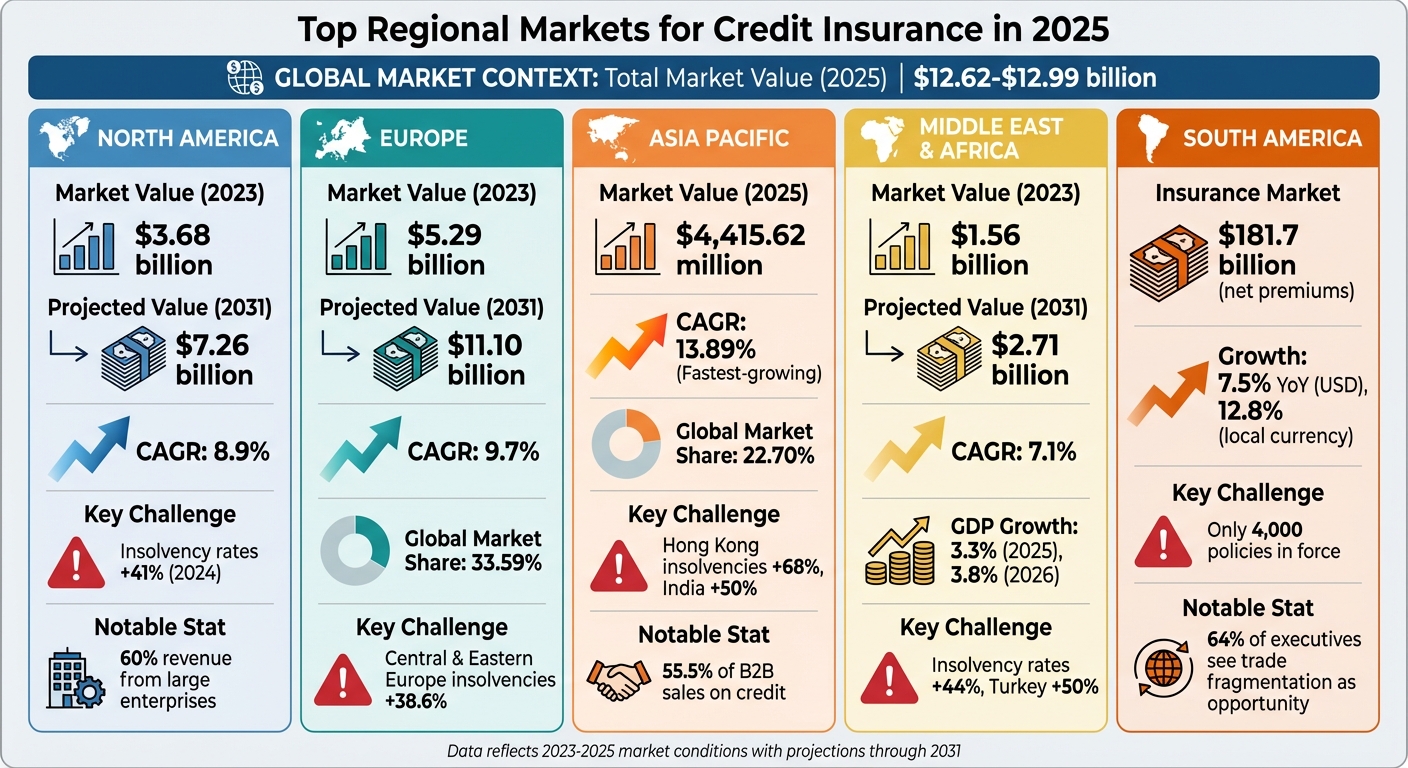

In 2025, the global credit insurance market was valued between $12.62 billion and $12.99 billion, driven by rising insolvencies and economic uncertainty. Key regional insights include:

- North America: Credit insurance grew significantly, with the U.S. leading due to increased insolvencies (+41% in 2024) and inflation pressures. SMEs gained traction, supported by government-backed programs.

- Europe: Accounted for 33.59% of the global market. Insolvencies surged, especially in Central & Eastern Europe (+38.6% in 2023), while geopolitical tensions and energy costs strained businesses.

- Asia Pacific: Fastest-growing region with a projected 13.89% CAGR. China’s market led, while insolvency rates spiked in Hong Kong (+68%) and India (+50%).

- Middle East & Africa: Economic recovery boosted credit insurance demand, but insolvency rates rose (+44%), with Turkey experiencing a 50% surge in failures.

- South America: Geopolitical tensions shaped the market, with limited policy adoption but growing demand in agribusiness and mining sectors.

The market reflects regional differences in trade risks, economic challenges, and demand for credit protection. Businesses are increasingly leveraging digital tools and tailored solutions to navigate these complexities.

Credit Insurance Market by Region 2025: Market Size, Growth Rates, and Key Challenges

Credit insurance helps financial institutions reduce risk in emerging market investments

sbb-itb-2d170b0

1. North America

North America’s trade credit insurance market was valued at $3.68 billion in 2023, with projections suggesting it could grow to $7.26 billion by 2031, reflecting a CAGR of 8.9%. The United States led the region’s market, largely due to economic pressures that made credit protection a necessity for businesses navigating uncertain conditions. This strong market foundation has coincided with increasing insolvency risks across the region.

In February 2024, Allianz Trade reported a 41% rise in insolvency rates, which hit small suppliers particularly hard. In Canada, overdue B2B invoices accounted for 44% of credit sales, with 50% of companies anticipating further financial difficulties after September 2025. These insolvency trends highlight the region’s financial vulnerabilities.

Inflation and high interest rates have further strained businesses, driving up costs and increasing the risks of counterparty defaults. As companies work to protect their margins and cash flow, credit insurance has become an essential tool. Adding to these challenges, trade tensions and geopolitical uncertainty in 2025 complicated cross-border operations, pushing firms to seek credit insurance as a way to manage unpredictable risks.

Among end users, the energy sector claimed the largest market share in 2023. Large enterprises generated 60% of global trade credit insurance revenue in 2025, but small and medium-sized enterprises (SMEs) are expanding quickly. This growth is supported by government-backed credit risk programs aimed at small exporters. International coverage continued to outpace domestic policies, reflecting the growing complexities of cross-border payment risks.

Insurers have also turned to digital innovation to stay ahead. COFACE launched URBA360, a risk management platform that uses AI and data analytics for real-time assessments. Additionally, the acquisition of Rel8ed, a North American analytics firm, has strengthened risk evaluation capabilities. Emma Crookes from Aon highlighted the need for insurers to adapt quickly to maintain their competitiveness and profitability in this evolving market.

2. Europe

Europe represents 33.59% of the global credit insurance market, with a valuation of $5.29 billion in 2023. By 2031, this figure is expected to climb to $11.10 billion, growing at a 9.7% compound annual growth rate (CAGR). Germany stands out as a leader in the region, contributing 6.92% of the global market share and generating $1.35 billion in revenue by 2025.

The market’s growth has been heavily influenced by rising insolvencies. Bankruptcies increased by 7% in 2023 and are anticipated to rise another 9% by late 2024. Western Europe saw insolvencies jump by 20% in 2023, while Central and Eastern Europe faced an even steeper rise, with insolvency rates surging 38.6% between 2022 and 2023.

"The insolvencies rate in Central & Eastern Europe (CEE) countries was highly significant in 2023… owing to the consequences of Russia’s invasion of Ukraine across the region." – Coface

These trends highlight the economic challenges European businesses are navigating. Inflation, rising interest rates, and fluctuating energy costs have put pressure on industries such as construction, real estate, hospitality, transport, and retail. Additionally, the ripple effects of Russia’s invasion of Ukraine have further disrupted supply chains and exacerbated labor shortages across the region.

Major insurance players like Allianz Trade, Atradius, and Coface are incorporating advanced technologies such as AI and big data, alongside ESG risk factors, to enhance real-time risk analysis. In 2023, the energy sector led the market, while government programs increasingly encouraged small and medium-sized enterprises (SMEs) to adopt credit insurance.

3. Asia Pacific

The Asia Pacific region is on track to generate $4,415.62 million in credit insurance revenue by 2025, accounting for 22.70% of the global market. With a projected 13.89% CAGR through 2033, it is set to outpace all other regions in growth. China leads the way with $1,603 million in revenue, while India and Japan are emerging as strong players with revenues of $812.61 million and $812.34 million, respectively. This economic momentum is reshaping credit insurance practices across the region.

Asia Pacific’s rapid expansion is closely tied to its role as a manufacturing powerhouse. Businesses in the region increasingly depend on credit insurance to protect against payment defaults. Insolvency rates have spiked in key markets such as Hong Kong (68%), India (50%), Singapore (49%), South Korea (45%), and Australia (45%), driven by the end of pandemic-era financial support, rising interest rates, and supply chain challenges.

"The level of risk, instability and volatility in the current economic climate is increasing daily. Payment defaults across the globe are rising and with them, we anticipate a steady rise in insolvencies in the coming years." – Eric den Boogert, Managing Director, Atradius Asia

B2B transactions conducted on credit made up 55.5% of total sales across the region, with Australia leading at 71.5%. Additionally, 42% of surveyed businesses revealed plans to increase their credit insurance usage, with this figure climbing to 51% in China and Hong Kong. Among industries, the automotive sector held the largest share of the market in 2023, while export-related policies outperformed domestic ones.

Government policies have also played a key role in supporting this growth. For instance, India’s Insurance Regulatory and Development Authority (IRDAI) issued 2021 guidelines allowing general insurers to offer tailored trade credit policies to MSMEs and financial institutions. These measures have helped reduce financial risks for smaller businesses venturing into international markets. This dynamic growth in Asia Pacific highlights the increasing importance of customized credit solutions in navigating global trade risks.

For businesses looking to manage the complexities of international trade in the Asia Pacific region, specialized services from providers like Accounts Receivable Insurance offer valuable support tailored to their needs.

4. Middle East & Africa

The Middle East & Africa region is navigating a period of dynamic growth and significant fiscal shifts, which are reshaping the credit insurance market. Economic recovery is accelerating, with real GDP growth forecasted at 3.3% in 2025, climbing to 3.8% by 2026 – a pace that surpasses all other global markets.

"MENA is poised for a remarkable economic resurgence – outpacing every other region in the world." – Niels de Hoog, Senior Economist, Atradius

This economic momentum is mirrored in the credit insurance market, valued at $1.56 billion in 2023 and expected to grow to $2.71 billion by 2031, driven by a 7.1% compound annual growth rate (CAGR). Saudi Arabia has emerged as the regional leader in 2023, with the energy sector being the largest end-user segment. However, the region is not without its challenges. Insolvency rates have risen by 44%, with Turkey seeing an alarming 50% increase in business failures in 2023 alone. These escalating defaults highlight the vital role of credit insurance in mitigating payment risks. This situation contrasts sharply with Europe’s credit insurance landscape, showcasing the varied nature of global credit risks.

The region’s economic diversity demands customized credit solutions. Oil-exporting countries are benefiting from higher production levels and diversification efforts, while oil-importing nations face hurdles like high debt burdens and limited room for fiscal reforms. Notably, international trade coverage dominates over domestic policies, reflecting the elevated risks tied to cross-border transactions. On a positive note, geopolitical stabilization – such as ceasefire agreements and fewer Houthi attacks on Red Sea shipping routes – has contributed to steadier trade flows.

5. South America

South America’s credit insurance market in 2025 is navigating a landscape shaped by geopolitical tensions between the United States and China. These dynamics bring both volatility and opportunities. The regional insurance market recorded $181.7 billion in net written premiums, reflecting a 7.5% year-over-year growth in U.S. dollars and a 12.8% increase in local currencies. Beneath this growth, however, lie significant challenges. U.S. tariffs – set at 50% for Brazil and 10% for most other South American nations – aim to address trade imbalances. At the same time, China’s export share surged from 3% in 2005 to 13% in 2024. This evolving trade landscape creates a complex environment for credit insurers operating in the region.

Economic experts underscore how South America’s trade relationships directly influence its credit risks. Daniel Zaga, Chief Economist at Deloitte Spanish LATAM, explains:

"The economic landscape of Latin America is significantly influenced by the relationship between its two major trading partners: the United States and China. In this context, analyzing the region’s position within the geopolitical tensions between these partners is crucial to understanding its future economic activity and dynamics."

The region’s credit insurance market remains underdeveloped, with only 4,000 policies in force across Latin America – 1,500 of which are in Brazil. This limited coverage exists alongside significant challenges, including financial opacity and currency volatility. In Brazil, receivables make up about 40% of a company’s assets on average, reflecting a considerable gap in protection. Argentina’s dual-currency economy adds another layer of complexity, as exchange-rate instability increases the need for safeguards against local currency devaluation.

Beyond geopolitical factors, market fundamentals like commodity prices also drive volatility. In 2025, oil prices averaged $63 per barrel, falling short of the five-year average of $74. This decline impacted export revenues for countries like Colombia, Brazil, and Argentina. Meanwhile, China’s role as the leading export destination for Brazil, Chile, and Peru has boosted demand for credit insurance products tailored to transpacific trade risks and Chinese counterparty exposure. Additionally, the conclusion of EU-Mercosur trade negotiations in December 2024 spurred demand for coverage on emerging cross-border trade flows.

Despite these hurdles, industry leaders see potential for growth. A survey found that 64% of regional executives view trade fragmentation as an opportunity, believing South American exports could fill gaps left by competing markets. Strong demand for credit insurance is particularly evident in the agribusiness, energy, and mining sectors, which collectively account for over 65% of Chinese investments in the region. However, the market recently faced a major test – a retail claim in Brazil resulted in a $600 million loss, prompting insurers to reassess their risk coverage strategies across critical sectors.

Pros and Cons

This section highlights the strengths and challenges influencing credit insurance across key regions in 2025.

Each region presents a unique mix of opportunities and obstacles for credit insurance providers.

North America continues to dominate as the largest insurance market globally, with over $1.7 trillion in annual net premiums. Property pricing benefits from high demand and sufficient capacity, but the casualty sector faces rising costs due to social inflation and litigation trends, which pushed rates up by 9% in Q4 2025. These pressures reflect broader issues tied to social and legal dynamics.

Europe boasts ample insurance capacity, with a noticeable shift from "follow" to "lead" underwriting positions. This competitive environment led to a 6% drop in composite rates in Q4 2025. Additionally, the region recorded €140.9 billion in high-yield bond issuance during the year. However, ongoing regional conflicts and trade tariffs create uncertainty for supply chains and trade credit lines.

Asia Pacific offers strong growth potential, flexible underwriting practices, and a composite rate decrease of 5%. Despite these advantages, the region remains vulnerable to natural disasters and geopolitical instability, which can significantly impact replacement costs.

South America benefits from increased economic stability, lower inflation, and advancements in digital transformation, all of which are driving demand for new insurance policies. However, exposure to natural catastrophes remains a major challenge, reflected in a 2% composite rate decrease.

Middle East & Africa is seeing increased interest from insurers, but escalating regional conflicts, such as those involving Israel and Iran, pose serious risks to political and trade stability.

Here’s a snapshot of each region’s key strengths and challenges:

| Region | Key Strength | Primary Weakness | Rate Trend (Q4 2025) |

|---|---|---|---|

| North America | Largest market size ($1.7T+ premiums) | Social inflation; casualty litigation | Casualty +9% |

| Europe | Abundant capacity; pricing discipline | Regional conflicts; supply chain uncertainty | Composite -6% |

| Asia Pacific | Growth-focused insurers; flexible terms | Natural disaster risks; geopolitical issues | Composite -5% |

| South America | Economic stability; digital transformation | Natural catastrophe exposure | Composite -2% |

| Middle East & Africa | Growing insurer interest | Regional conflicts affecting trade credit | Not specified |

These regional dynamics showcase how economic shifts, trade policies, and environmental risks shape credit insurance trends in 2025.

Conclusion

In 2025, North America and Europe led global credit markets, with the U.S. achieving $828.9 billion in leveraged loan issuance and Europe recording €306 billion. The U.S. market thrived on quick deal execution and a surge in refinancing driven by lower interest rates. Meanwhile, Europe drew investor attention with disciplined pricing and limited asset availability, even amidst geopolitical uncertainties. These figures highlight the distinct regional dynamics that also influence emerging markets in Asia Pacific and South America.

Asia Pacific and South America hold promising opportunities for international expansion. Softer market conditions in these regions, reflected by gradual price decreases, allow businesses to secure favorable credit insurance terms while addressing risks like natural disasters and market volatility.

"Now is the time for clients to take advantage of market conditions. In today’s competitive market, clients will find that insurers are more flexible on terms, and more willing to engage with insureds on enhancements to coverages, limits and attachment points." – Joe Peiser, CEO, Commercial Risk Solutions, Aon

Businesses should align their credit insurance strategies with their regional exposure and trading patterns. Companies with European operations can benefit from competitive pricing and leverage the high-yield bond market, which reached approximately €140.9 billion in 2025. For those focusing on emerging markets, it’s crucial to prioritize protection against geopolitical risks, trade tensions, and supply chain disruptions, which have become more pronounced over the year. These trends emphasize the importance of strategic credit insurance in navigating diverse market conditions.

Accounts Receivable Insurance offers tailored trade credit insurance solutions designed to address specific regional risks and opportunities. Through a global network of credit insurance carriers, ARI helps businesses manage geoeconomic challenges, control the total cost of risk, and secure comprehensive domestic and international coverage. Whether mitigating non-payment risks in volatile regions or taking advantage of favorable market conditions, strategic credit insurance remains a key tool for managing trade dynamics in 2025.

FAQs

Which region is best for credit insurance growth in 2025?

The Asia-Pacific region is expected to drive growth in credit insurance by 2025, fueled by increasing market activity and changing approaches to managing risks. Meanwhile, the United States will continue to play a major role, thanks to its strong and established risk management systems.

How do insolvency trends affect credit insurance pricing and limits?

Rising rates of insolvency are leading to tighter credit insurance limits and higher premiums. This is largely driven by the growing risks of non-payment and defaults. In response, insurers are adopting stricter risk management strategies to navigate these financial uncertainties effectively.

Should I buy domestic or international credit insurance coverage?

Choosing the right type of credit insurance – domestic or international – largely hinges on where your business operates and the risks you face. For businesses dealing primarily within the U.S., domestic credit insurance offers protection against issues like non-payment or insolvency in local markets. On the other hand, if your company engages in global trade, international credit insurance shields you from risks such as political unrest or currency fluctuations that can disrupt cross-border transactions. The key is to match your coverage to your trading activities and the specific risks you want to manage.