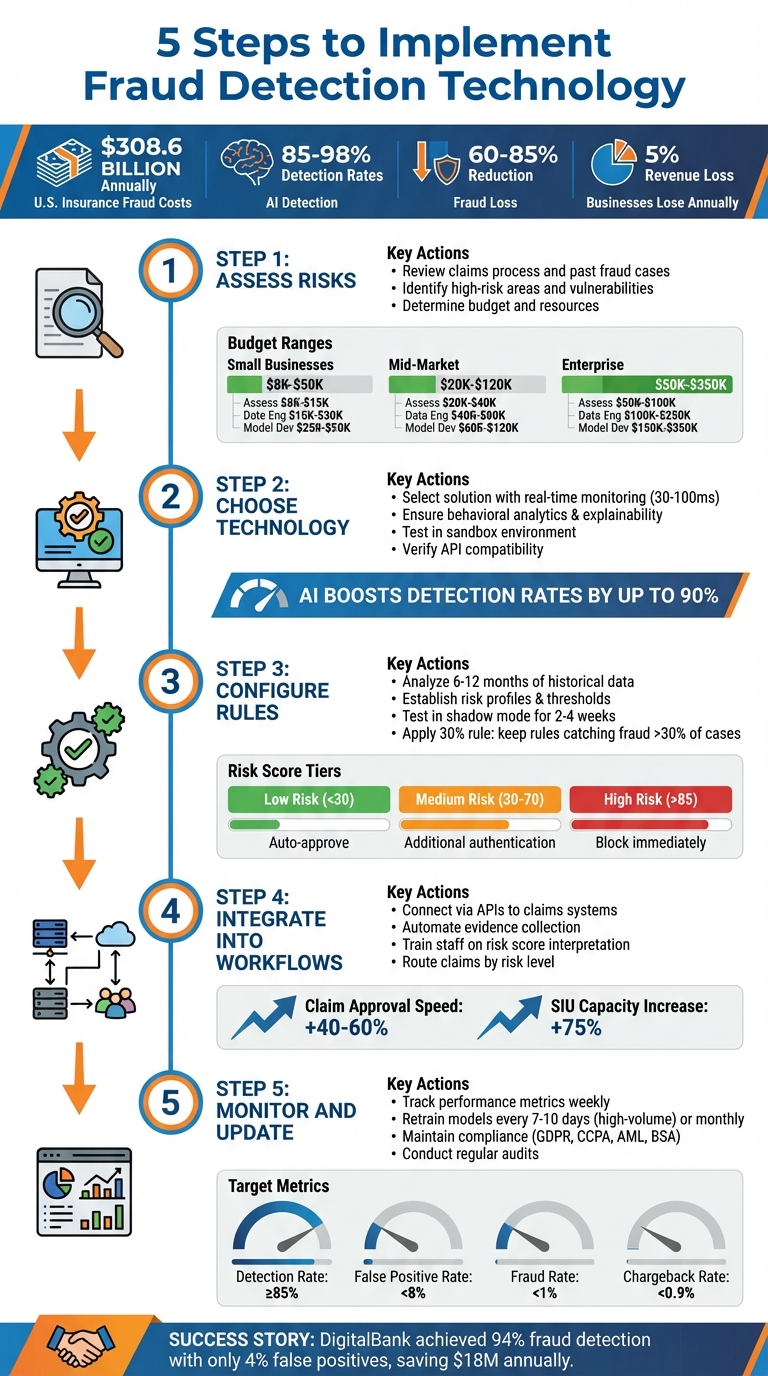

Fraud is a growing challenge for businesses, with U.S. insurance fraud alone costing $308.6 billion annually. Traditional methods often fall short, identifying fraud too late. AI-powered fraud detection systems offer a more efficient solution, delivering detection rates of 85–98% with fewer false positives. These tools analyze claims in real time, cutting fraud losses by 60–85% and speeding up investigations.

Here’s how you can implement fraud detection technology effectively:

- Step 1: Assess Risks – Review your claims process, past fraud cases, and high-risk areas. Identify vulnerabilities and budget for implementation costs, which can range from $8K for small businesses to $350K for large enterprises.

- Step 2: Choose Technology – Select a solution with real-time monitoring, behavioral analytics, and explainability. Ensure compatibility with your systems and test vendor solutions in a sandbox environment.

- Step 3: Configure Rules – Use historical data to fine-tune detection thresholds and establish risk profiles. Test detection settings in shadow mode to minimize false positives before full deployment.

- Step 4: Integrate Into Workflows – Connect tools to existing claims systems via APIs, automate evidence collection, and train staff to interpret risk scores and handle flagged cases.

- Step 5: Monitor and Update – Regularly review performance metrics, retrain models to counter evolving fraud tactics, and maintain compliance with regulations like GDPR and CCPA.

5-Step Process to Implement AI-Powered Fraud Detection Technology

Build Realtime Fraud Detection AI from Scratch – End to End Machine Learning Project – Part 1

sbb-itb-2d170b0

Step 1: Review Your Claims Process and Fraud Exposure

Before diving into technology, take a step back and assess where your organization might be vulnerable to fraud. Start by closely reviewing your current claims process and learning from past incidents. Did you know that businesses lose about 5% of their annual revenue to fraud? The problem is, many companies don’t realize the full extent of their risks until they take the time to map them out.

Review Current Procedures and Past Fraud Cases

If your process relies heavily on manual reviews, you’re likely only catching fraud after payouts have already been made. To get ahead of the issue, document recent fraud cases and look for recurring patterns. This step is critical – it provides the groundwork for identifying weak points in your system. Skipping this analysis leaves you guessing about which risks to address first, which could lead to wasted resources and missed opportunities to tighten controls.

Identify High-Risk Claims and Business Partners

Once you’ve reviewed your history, focus on identifying claims and partners that pose the highest risk. For example, in accounts payable, watch out for red flags like duplicate vendor details, inconsistent claimant information, or unusual transaction patterns, such as round-dollar amounts or split invoices. When it comes to claims, behavioral cues can also signal fraud – things like mismatched narratives and timestamps, reused image metadata, or similar language across unrelated claims. Internally, risks increase when one employee handles everything from setup to payment approval, or when staff members avoid taking time off or sharing responsibilities.

Determine Available Resources and Budget

The cost of implementing fraud prevention measures varies depending on the size of your business. Here’s a breakdown based on Stratagem Systems’ 2026 Guide:

- Small businesses: Plan for $8K–$15K for fraud assessment, $15K–$30K for data engineering, and $25K–$50K for model development.

- Mid-market companies: Expect $20K–$40K for fraud assessment, $40K–$80K for data engineering, and $60K–$120K for model development.

- Enterprise organizations: Budget $50K–$100K for fraud assessment, $100K–$250K for data engineering, and $150K–$350K for model development.

Don’t forget to account for staffing needs. Hiring fraud analysts, data engineers, and IT professionals is often necessary to ensure a smooth implementation. For example, a regional auto and property insurer that processes 95,000 claims annually spent $425K on their initial implementation and $125K per year on operations. However, their efforts paid off – they prevented $18.5 million in losses annually.

Step 2: Choose the Right Fraud Detection Technology

With your risk assessment in hand, the next step is to select a fraud detection solution that fits your needs. This decision is crucial – fraud-related losses are expected to surpass $41 billion by 2027, a sharp 25% increase since 2020. Picking the wrong technology could leave your organization vulnerable.

Review Available Technologies

To effectively combat fraud, you’ll need tools that provide real-time monitoring, behavioral analytics, and clear explainability. Real-time systems can process decisions in as little as 30–100 milliseconds, stopping fraudulent activity during authorization without delaying legitimate transactions. Behavioral analytics, on the other hand, can detect anomalies – like a claimant suddenly submitting multiple claims across different states or using unfamiliar device fingerprints.

Explainability is equally important. The system should not only flag suspicious activity but also clearly explain why it was flagged. This transparency is essential for meeting regulatory requirements and maintaining trust within your team.

AI-powered models stand out for their ability to boost fraud detection rates by up to 90%, all while minimizing false positives. Considering that 62% of financial professionals reported a rise in fraud alerts over the past year, this capability can make a significant difference. When evaluating these technologies, you’ll need to decide between rules-based systems (which are straightforward and fast but less flexible), machine learning models (which are adaptable but more complex), or hybrid systems that combine both approaches. Finally, ensure the chosen solution integrates smoothly with your current systems.

Assess Vendors and System Compatibility

Integration is a major hurdle for many companies – 48% of firms cite compatibility with existing compliance tools as a key challenge. Before committing to a vendor, ask for a technical demo that demonstrates how their solution will work with your claims platforms. Prioritize systems with API-first architecture, as these allow for real-time data enrichment and seamless integration.

Look for vendors that offer a sandbox environment where you can test fraud detection rules using real-world data without affecting live operations. Additionally, confirm that the solution includes a library of pre-configured rules for quick setup, regular software updates, and accessible customer support. Compliance is another critical factor – make sure the tool adheres to regulations like GDPR and CCPA to avoid fines and reputational damage.

Set Implementation Timelines

Once you’ve chosen a vendor, map out a deployment timeline that matches your operational needs. While basic fraud detection systems can be implemented quickly, more advanced setups designed to tackle organized fraud may require extended timelines for data collection and collaboration. Keep in mind that U.S. financial institutions are required to investigate fraud reports within 10 to 20 business days, so your implementation plan must account for these regulatory deadlines.

Consider a phased rollout. Start with automated screening for high-volume transactions, then gradually introduce manual validation processes. Early in the deployment, prioritize web tagging to collect behavioral data – this will help create dynamic risk profiles. Finally, schedule ongoing maintenance to adapt to new fraud tactics as they emerge.

Step 3: Configure Detection Rules and Models

This step is all about turning your fraud assessment and technology choices into actionable detection measures, helping you strengthen your claims management strategy. Once you’ve chosen your technology, it’s time to fine-tune it to detect fraud patterns specific to your business. Adjusting default settings is key to minimizing false positives and ensuring accuracy.

Establish Normal Behaviors and Risk Profiles

Start by analyzing 6–12 months of transaction data to identify typical patterns like average authorization rates, claim amounts, and velocity metrics. For example, a claim that far exceeds the usual amount should raise a red flag.

Create behavioral profiles by observing how legitimate users interact with your system. Look at login times, devices used, and navigation habits during claims submissions. Define risk indicators such as velocity metrics, behavioral ratios, and geographic consistency. It’s also important to segment these profiles by business type – patterns differ for e-commerce, subscription services, and digital goods. Relying on generic defaults can sometimes block legitimate customers unnecessarily.

PayPal‘s fraud detection engine in 2024 is a great example. It analyzed over 1,000 data points per transaction – like IP address and transaction velocity – to evaluate risk, helping them keep fraud losses below industry averages. Your system should assign a numerical risk score (typically ranging from 0 to 100) to every transaction based on signals like device fingerprinting, IP geolocation, and payment metadata.

Once you have well-defined risk profiles, you can fine-tune your system’s alerts to align with your business’s unique fraud patterns.

Configure Alert Thresholds and Detection Settings

Before going live with new rules, test them in shadow mode for 2–4 weeks to gather performance data. Apply the 30% rule: keep rules that catch fraud in over 30% of cases, and adjust or discard those that fall below 10%.

To determine the net benefit of each threshold, use this formula:

(Fraud Blocked × Average Fraud Loss) – (False Positives × Average Customer Lifetime Value Lost).

For instance, a rule that prevents $50,000 in fraud but results in $75,000 in lost customer value would be a poor choice. DigitalBank demonstrated the importance of this approach in February 2025. Under the leadership of Chief Risk Officer Jennifer Kim, they replaced a rule-based system with AI-tuned thresholds, achieving a 94% fraud detection rate while cutting false positives from 68% to just 4%. This shift saved the company $18 million annually in fraud losses.

"Our AI fraud detection system catches 94% of fraud with only 4% false positives – compared to 52% detection and 68% false positives from our old rule‐based system."

- Jennifer Kim, Chief Risk Officer, DigitalBank

Consider implementing tiered response thresholds instead of simple block-or-allow decisions. For example:

- Transactions with low-risk scores (below 30) can be auto-approved.

- Medium-risk transactions (scores between 30 and 70) might require additional authentication, like 3D Secure or manual review.

- High-risk transactions (scores above 85) should be blocked immediately.

For high-value claims or risky products like gift cards, stricter thresholds are a good idea. On the other hand, trusted repeat customers might benefit from relaxed thresholds to reduce unnecessary friction. You can also set up velocity limits, such as blocking a card after three charges within an hour, to catch automated card-testing attacks.

Once you’ve configured these thresholds, it’s essential to establish clear protocols for handling different levels of risk.

Create Response Protocols

Use the insights from your initial fraud review to shape your alert response strategies. Define workflows for different risk levels: auto-approve low-risk transactions, add verification steps for medium-risk cases, and block or escalate high-risk ones.

For medium-risk alerts, consider step-up authentication methods like multi-factor or biometric verification instead of outright blocking the transaction. One global payments firm saw a 70% reduction in credential-based fraud after introducing biometric verification for high-value transactions.

Integrate your detection tools with case management systems to automatically route alerts. For instance, Amazon’s fraud prevention system escalates high-risk cases to investigators in under five seconds, stopping potential losses before they occur.

Establish internal communication channels to notify relevant teams – such as finance, IT, legal, and compliance – when fraud is detected. Clearly define escalation paths for sensitive cases. Additionally, create feedback loops where the results of manual investigations feed back into your AI models and detection rules. This ensures your system evolves to counter new fraud tactics. Regularly review your rules – monthly audits can help you adapt to changing conditions, like a shift from peak sales periods to normal traffic levels.

Step 4: Add Technology to Claims Workflows

Integrating fraud detection tools directly into claims workflows is essential for improving efficiency. The idea is to make fraud detection a natural part of the claims process – not an extra, cumbersome step.

Link Tools to Existing Systems

Use API connections or serverless functions like AWS Lambda to connect your fraud detection tools with your claims platform. This setup ensures that claims are evaluated in seconds as they enter your system. A modular approach allows you to update detection rules or integrate new services without overhauling the entire workflow.

A unified dashboard can streamline this process by displaying risk scores and reason codes as soon as claims are reviewed. Automation plays a key role here: low-risk claims can be fast-tracked, while high-risk ones are flagged for further investigation by the Special Investigations Unit (SIU). This approach has been shown to speed up claim approvals by 40–60% and increase SIU capacity by as much as 75%.

| Detection Result | Claim Routing | Adjuster/System Action |

|---|---|---|

| Clean | Standard Queue | Process normally; log for audit |

| Low Risk | Standard Queue | Review advisory note; may request additional evidence |

| Medium Risk | Priority Queue | Review forensic findings; assess for escalation |

| High Risk | SIU Referral | Immediate investigation; do not process payment |

Set Up Automated Processes

Automating evidence collection can save significant time. Secure portals and encrypted links allow for fast document uploads, cutting down on email exposure and expediting resolutions.

Real-time alerts further enhance responsiveness. For example, one auto insurer used analytics to uncover a staged accident fraud network, recovering $1 million in subrogation within a single month. Alerts like these ensure immediate action, preventing delays in resolving fraud.

"Fraud doesn’t wait. Neither should your defenses."

Service level agreements (SLAs) can define clear timelines for action. For instance, high-risk claims might be assigned to the SIU within two hours, while low-risk claims are processed within 24 hours.

Train Staff on System Use

Even the best technology won’t deliver results without proper training. Staff should be taught how to interpret risk scores, confidence levels, and flagged details. Role-specific training in a sandbox environment, using synthetic data, ensures security while building user competence.

Training should emphasize decision-making: when to approve a claim, when to request additional verification (like multi-factor authentication), and when to escalate for manual review. Establishing a feedback loop, where staff label outcomes as confirmed fraud or cleared claims, helps refine machine learning models over time. Investigators can also benefit from structured interview templates and fraud checklists to ensure consistency in their reviews.

"Fraud detection workflows are the insurer’s immune system."

- The Moxo Team

Step 5: Monitor, Improve, and Update Detection Systems

With your thresholds configured and workflows in place, it’s time to focus on keeping your fraud detection system running smoothly. Regular monitoring and updates are key to maintaining its effectiveness over time.

Track Detection Performance

Start by setting performance baselines before introducing any new detection rules. Metrics like issuer authorization rates and standard block rates help define what “normal” looks like for your system. When testing new rules, use shadow mode for at least two weeks. This approach lets you see how the rules would perform without affecting actual transactions or revenue.

Keep an eye on these four critical metrics:

- Detection Rate: Aim for 85% or higher.

- False Positive Rate: Keep it under 8%.

- Fraud Rate: Maintain below 1%.

- Chargeback Rate: Target below 0.9%.

AI-powered systems often outperform traditional rule-based systems, achieving detection rates between 85–98%, compared to just 40–60% for older methods. They also significantly reduce false positives, cutting them from as high as 70% down to 2–8%.

Use a combination of real-time dashboards and deeper forensic analysis to monitor your system. Dashboards offer quick insights, while forensic analysis helps identify why certain fraud cases slipped through. Be vigilant for model drift, which happens when your machine learning models lose effectiveness against evolving fraud tactics. Schedule regular reviews – monthly or quarterly – to update outdated rules that may be causing unnecessary friction or missing new fraud patterns.

Once you’ve assessed performance, it’s time to refine your detection models to tackle emerging threats.

Update Models for New Fraud Methods

Fraudsters are always finding new ways to exploit systems, so your detection models need to stay one step ahead. Regularly retrain your models – monthly at a minimum, or every 7–10 days in high-volume environments. Incorporate confirmed fraud cases into the training process to sharpen detection accuracy.

After any fraud incident, conduct a thorough audit to identify missed patterns and adjust your rules accordingly. Document the logic behind every detection rule, including the specific fraud pattern it addresses and the data supporting it. This ensures critical protections aren’t accidentally removed during updates.

Here’s a real-world example: In 2025, a mid-sized online retailer with $280 million in annual revenue implemented a custom gradient boosting model combined with device fingerprinting. Over 22 weeks, the system achieved a 94% fraud detection rate and reduced false positives to 5%. This led to an 81% drop in fraud losses – down from $4.2 million to $800,000 – and recovered $1.2 million in revenue previously lost to false declines.

While technical updates are crucial, don’t overlook the importance of staying compliant with regulations.

Maintain Regulatory Compliance

Your fraud detection system must adhere to regulations like Anti-Money Laundering (AML) and the Bank Secrecy Act (BSA), especially for transaction monitoring and sanctions screening. Build compliance into your system from the ground up by incorporating privacy frameworks like GDPR and CCPA into its design.

Implement strict data governance to manage access and ensure compliance with GDPR, CCPA, and PCI DSS 4.0 standards. For ambiguous cases, maintain human oversight to provide documented justifications – this is crucial during regulatory audits. Regular audits and system tests are essential to confirm ongoing compliance.

"The AI fraud system reduced our AML false positives from 95% to 12% while actually improving our detection of real suspicious activity by 42%. Our compliance team went from drowning in alerts to focusing on genuine risk – a complete transformation."

- Robert Chen, Chief Compliance Officer, Regional Trust Bank

Companies that embed compliance into their fraud detection systems often see a 65% improvement in regulatory reporting accuracy and a 40% reduction in duplicate processes. To strike the right balance between data collection and privacy, involve your legal and compliance teams early when adopting new fraud detection technologies.

Key Factors for Successful Implementation

Getting fraud detection tools up and running is just the beginning – the real challenge lies in making them work effectively in day-to-day operations. Here are some critical elements that ensure success after implementation.

Blending static rules with AI is a powerful way to improve detection accuracy. Static rules can catch straightforward, high-volume fraud – like multiple failed logins or transactions from blacklisted IPs – accounting for 15–20% of cases. On the other hand, AI excels at identifying more complex, evolving fraud schemes that static rules might miss. Together, this mix creates a system that balances precision with efficiency, setting the groundwork for even more advanced strategies.

Speed is non-negotiable. In the digital world, fraud decisions need to happen in under 100 milliseconds to prevent issues like cart abandonment or lost sales. The stakes are high – businesses lose around 5% of their annual revenue to fraud, with a median loss of $125,000 per case. False positives add another layer of cost, averaging $12 to $18 each when you include customer service and recovery efforts.

Automation paired with human oversight is the key to handling cases effectively. Automating simple, clear-cut scenarios – like blocking low-value transactions that raise obvious red flags – saves time. However, high-value or complex cases, such as those over $10,000, should be flagged for manual review. To fine-tune the system, run it in shadow mode for two weeks before going live. This approach allows you to adjust thresholds without disrupting actual transactions.

Collaboration across teams is another must. Fraud detection systems need to align with broader business goals, which means business leaders, fraud experts, data scientists, and IT teams all need to work together. Keeping customer service teams informed about the reasons behind transaction declines can also help them manage spikes in false positives more effectively. And don’t forget: continuous adjustments are necessary to tailor the system to your business’s evolving needs.

Conclusion

Fraud detection technology is in a constant race against ever-evolving tactics. The 95% year-over-year rise in identity-based attacks in 2023 is a stark reminder that fraudsters are always innovating. To stay ahead, systems must be continuously improved – retraining machine learning models every 7–10 days, monitoring performance metrics weekly, and updating detection rules to address emerging patterns. This isn’t a one-and-done effort; it requires ongoing attention and action.

The outlined framework – evaluating claims processes, selecting the right technology, fine-tuning detection rules, integrating systems into workflows, and committing to continuous improvement – offers a proactive way to prevent fraud before it escalates. By identifying fraudulent claims at the intake stage, businesses can stop issues before payments are made, rather than scrambling to recover losses after the fact. AI-powered systems have proven to be far more effective than traditional methods.

To validate your approach, test the solution on a high-risk product line for 30 days before expanding it across the organization. Time is critical – while you’re deliberating, fraudsters are already targeting your processes. With 20% of all insurance claims in the U.S. estimated to be fraudulent, the financial stakes are enormous, amounting to billions in potential losses.

For high-value or complex cases, involving skilled analysts ensures a balance of technology and human expertise. This "human-in-the-loop" model allows systems to learn from real-world decisions, improving accuracy over time.

Fraud detection demands constant vigilance and adaptability. Businesses that treat it as an ongoing priority, rather than a one-time task, are the ones that thrive. The investment in regular monitoring and refinement not only safeguards against fraud but also delivers long-term financial benefits.

For more guidance on proactive claims management and fraud prevention, visit Accounts Receivable Insurance.

FAQs

What data do I need before using AI fraud detection?

Before implementing AI fraud detection, it’s crucial to start with high-quality data about your transactions and activities. This data should be standardized, thoroughly cleaned, and verified to ensure accuracy. Pinpoint key fraud indicators that will help train and test your models effectively. Preparing your data properly is essential for AI systems to identify suspicious patterns with precision and reduce the chances of false positives.

How do I cut false positives without missing fraud?

To tackle fraud effectively while minimizing false positives, it’s all about finding the right balance between precision and a smooth customer experience. Start by regularly fine-tuning your detection models and adjusting thresholds to stay ahead of evolving fraud tactics. Machine learning plays a key role here, helping systems adapt to new patterns quickly.

Consider integrating advanced methods like supervised and unsupervised learning or graph analytics to enhance detection capabilities. Keeping your models updated with fresh data ensures they’re always relevant. Real-time monitoring is another critical piece – this helps approve legitimate transactions promptly without compromising fraud prevention. By combining these strategies, you can maintain security without frustrating your customers.

How long does fraud detection integration usually take?

The time it takes to set up fraud detection technology depends on how complex the system is. For simpler setups, such as real-time fraud detection, the process might only take 1–2 weeks. However, more advanced systems – especially those powered by AI that require data preparation and thorough testing – can take anywhere from several weeks to a few months. Factors like the size of the organization and the existing technical infrastructure also play a big role in determining the timeline.