Protecting your business against financial and operational risks is crucial. Two major insurance options – Trade Credit Insurance (TCI) and Supply Chain Insurance (SCI) – offer targeted solutions for different challenges:

- Trade Credit Insurance: Shields your revenue by covering customer non-payment due to insolvency or geopolitical risks.

- Supply Chain Insurance: Focuses on minimizing disruptions in sourcing, production, or logistics caused by supplier failures, natural disasters, or strikes.

Quick Overview:

- TCI: Protects accounts receivable, stabilizes cash flow, and supports growth in new markets.

- SCI: Mitigates supplier-related disruptions, ensuring smooth operations and timely delivery.

Key Difference: TCI safeguards your income, while SCI ensures operational continuity.

Trade Credit Insurance Explained: Safeguard Your Business from Payment Risks

sbb-itb-2d170b0

What is Trade Credit Insurance?

Trade credit insurance (TCI) is a tool businesses use to protect themselves from financial losses when customers fail to pay their invoices. Designed for business-to-business transactions, this type of insurance covers both domestic and international trade.

If a customer defaults on payment due to insolvency, bankruptcy, or prolonged non-payment, TCI reimburses a large portion of the unpaid amount – typically between 85% and 95% of the invoice value. This protection applies whether you’re working with a local client or an international buyer.

The scale of this market is impressive. In the U.S., over $600 billion in annual sales is backed by trade credit insurance. Globally, exposure under TCI policies reached €3.5 trillion in 2024. The market itself has grown significantly, from $9.39 billion in 2019 to a projected $18.14 billion by 2027, with an annual growth rate of 8.6%.

Key Features of Trade Credit Insurance

Here’s how TCI works to safeguard your receivables:

TCI addresses three main risk categories. Commercial risks include situations where customers face insolvency, bankruptcy (like Chapter 7 or Chapter 11 filings), or fail to pay within agreed terms. Political risks are specific to international trade and cover issues such as currency inconvertibility, trade embargoes, wars, or government restrictions that block payments. Lastly, financing risk comes into play by making insured receivables more appealing to lenders, helping businesses secure working capital.

Insurers also help by monitoring the financial health of your customers and setting pre-approved credit limits. Your coverage is tied to these limits, meaning your customers’ creditworthiness has already been assessed. Many insurers provide online platforms where you can track these limits, file claims, and manage your policy in real time.

TCI is flexible, offering options like full portfolio coverage or protection for specific transactions. Premiums are typically less than 1% of the insured volume, with minimum premiums starting around $3,500, depending on your business size and risk factors. These features make TCI an adaptable solution for managing financial risks.

Benefits of Trade Credit Insurance

One of the biggest advantages of TCI is the stability it brings to your cash flow. If a key customer defaults, you’re reimbursed instead of absorbing the loss. As Atradius explains:

"Trade credit insurance is your financial safety net and is a risk management tool that protects your business from bad debts".

Beyond direct protection, TCI can improve your relationship with lenders. Insured receivables are seen as secure collateral – similar to an insured property – making it easier to negotiate favorable financing terms, access higher credit limits, and secure working capital. Presenting your TCI policy to lenders shows that your receivables are protected, which can be a game-changer for business growth.

TCI also supports competitive growth strategies. With this coverage, you can confidently extend more attractive credit terms to larger clients or explore higher-risk markets abroad. Additionally, the buyer ratings provided by insurers help you assess customer reliability, reducing the chance of extending credit to risky clients. Many policies even include professional debt collection services, where the insurer works to recover unpaid amounts before processing your claim.

Accounts Receivable Insurance (ARI) specializes in tailoring TCI policies to fit specific business needs. They offer services such as customized coverage, in-depth risk assessments, and claims management support. With access to a global network of credit insurance carriers, ARI ensures your policy aligns with your unique risk profile and growth goals, whether you’re focused on domestic or international markets.

What is Supply Chain Insurance?

Supply chain insurance (SCI) is designed to protect businesses from financial losses and operational hiccups that can arise across sourcing, production, and logistics. While trade credit insurance focuses on safeguarding receivables by covering customer defaults, SCI zeroes in on disruptions in the supply chain itself. It ensures that businesses can weather unexpected interruptions caused by issues with suppliers, manufacturers, or logistics providers.

Here’s how it works: if a key supplier, facility, or transport partner can’t deliver due to a covered risk, SCI steps in to cover the financial fallout. This could mean reimbursing lost revenue or paying for extra costs, like expedited shipping when a supplier’s factory is hit by a flood, or covering delays caused by a port closure affecting inventory shipments.

SCI differs from standard business interruption insurance, which only covers disruptions to your own property. Instead, SCI is activated when a supplier’s operations are impacted, often through Contingent Business Interruption coverage. The importance of this protection cannot be overstated. According to the Business Continuity Institute, 75% of businesses experienced at least one supply chain disruption in 2020.

The COVID-19 pandemic underscored just how vital it is to maintain a steady supply chain. Sarah Murrow, President and CEO of Allianz Trade Americas, put it succinctly:

"As was demonstrated during COVID, trade credit insurance is vital to keeping liquidity in supply chains. It is the glue that keeps world trade going."

SCI aims to ensure operational continuity even when third-party disruptions threaten to derail your business. Below, we’ll explore the key features that make this coverage an essential tool for managing supply chain risks.

Key Features of Supply Chain Insurance

SCI covers a wide range of potential disruptions that can halt or slow operations. These include:

- Natural Disasters: Events like earthquakes, floods, hurricanes, and snowstorms can damage supplier facilities or disrupt transportation routes.

- Logistics and Transport Issues: Port closures, theft, road or bridge failures, and accidents can create costly delays.

- Supplier-Specific Problems: Challenges such as supplier insolvency, industrial accidents, or production breakdowns are also covered.

Beyond these, SCI also addresses geopolitical risks, including political unrest, armed conflict, and changes in trade policies or tariffs. It extends to operational challenges like cyberattacks, labor strikes, public health emergencies, and regulatory actions.

A standout feature of SCI is Extra Expense Coverage. This part of the policy reimburses businesses for additional costs incurred to keep operations running – like paying for expedited shipping or hiring extra labor after a supplier’s property is damaged. For businesses heavily reliant on a single supplier, Supplier Insolvency Insurance provides focused protection against financial failures of that key vendor.

Benefits of Supply Chain Insurance

SCI helps businesses minimize downtime by providing the financial resources needed to adapt quickly when disruptions strike. For instance, instead of absorbing the costs of finding alternative suppliers or fast-tracking shipments, businesses can rely on SCI to recover those expenses. This ensures delivery schedules and customer commitments stay on track, even when the unexpected happens.

This type of coverage is particularly valuable for companies with concentrated supplier bases. If your business depends on a single manufacturer or a supplier in a high-risk area, SCI acts as a safety net. It also allows businesses to tailor coverage to address specific regional risks, such as political instability or natural disasters.

In addition to covering immediate costs, SCI bolsters long-term resilience. It supports contingency planning and helps manage increased expenses during crises. As supply chains become more interconnected, companies are shifting from basic cargo insurance to SCI policies that address non-physical disruptions like regulatory changes or public health emergencies. With the rise of cyberattacks as a major supply chain threat, SCI is evolving into a more integrated solution to meet these modern challenges.

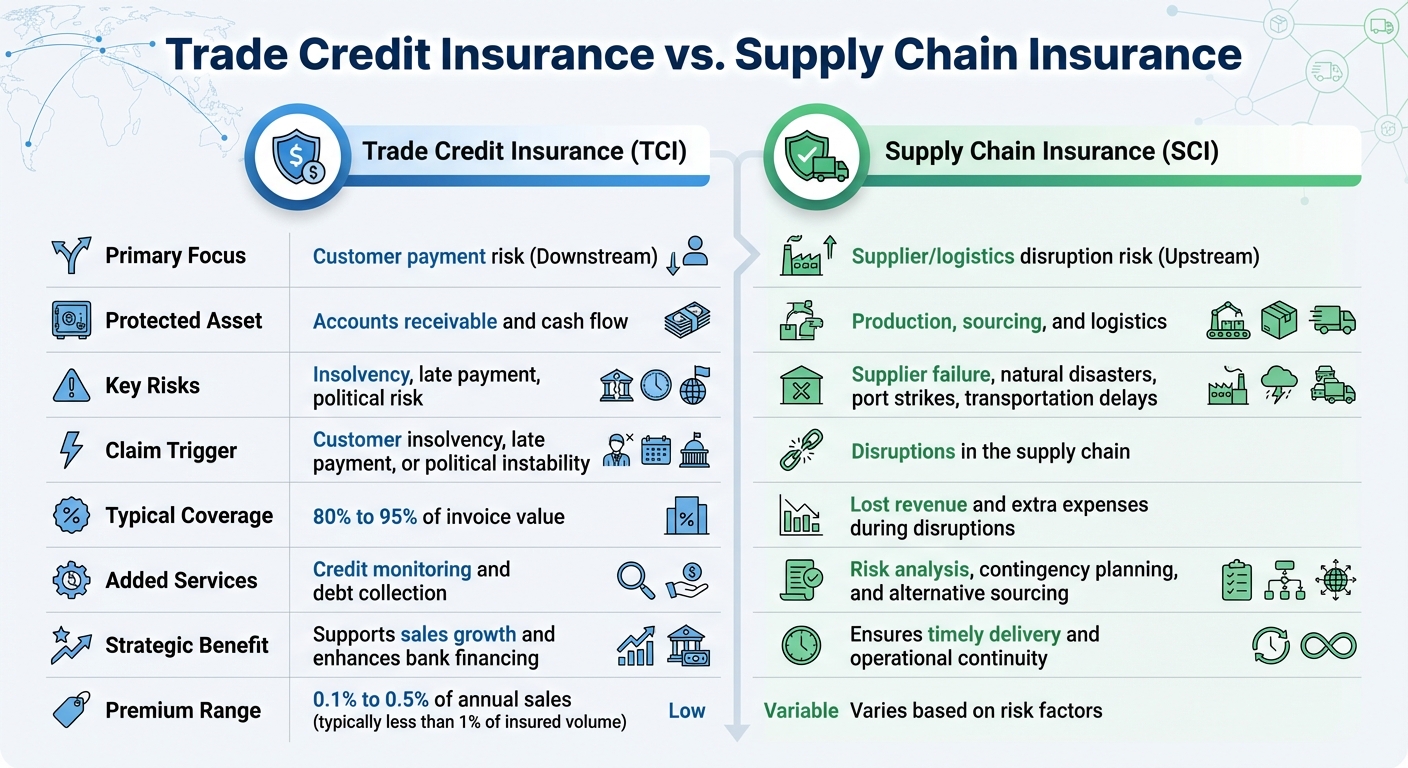

Key Differences Between Trade Credit Insurance and Supply Chain Insurance

Trade Credit Insurance vs Supply Chain Insurance: Key Differences Comparison

When comparing trade credit insurance and supply chain insurance, it’s clear that each serves a distinct purpose in safeguarding your business. While both aim to mitigate financial risks, their focus and mechanisms differ significantly. Trade credit insurance protects your revenue by covering customer non-payment, while supply chain insurance shields you from disruptions in sourcing, production, or logistics operations.

The primary goals of these policies set them apart. Trade credit insurance ensures cash flow stability by securing accounts receivable, guaranteeing payment for goods or services already delivered. On the other hand, supply chain insurance focuses on keeping your operations running smoothly, protecting your ability to source materials, manufacture products, and meet delivery schedules.

The triggers for claims also highlight their differences. Trade credit insurance comes into play when customers fail to pay due to insolvency, late payments, or political issues. Meanwhile, supply chain insurance activates when there are disruptions like supplier bankruptcy, natural disasters, port strikes, or transportation delays.

Each policy offers specialized support services. Trade credit insurance often includes tools like credit monitoring and debt collection services, while supply chain insurance provides risk analysis, contingency planning, and help in finding alternative suppliers. As Atradius explains:

"TCI is primarily concerned with customer payment risk… In contrast, SCI is designed to manage operational risks that arise from disruptions in the supply chain".

Comparison Table: Trade Credit Insurance vs. Supply Chain Insurance

| Feature | Trade Credit Insurance | Supply Chain Insurance |

|---|---|---|

| Primary Focus | Customer payment risk (Downstream) | Supplier/logistics disruption risk (Upstream) |

| Protected Asset | Accounts receivable and cash flow | Production, sourcing, and logistics |

| Key Risks | Insolvency, late payment, political risk | Supplier failure, natural disasters, port strikes, transportation delays |

| Claim Trigger | Customer insolvency, late payment, or political instability | Disruptions in the supply chain |

| Typical Coverage | 80% to 95% of invoice value | Lost revenue and extra expenses during disruptions |

| Added Services | Credit monitoring and debt collection | Risk analysis, contingency planning, and alternative sourcing |

| Strategic Benefit | Supports sales growth and enhances bank financing | Ensures timely delivery and operational continuity |

What Each Policy Does Not Cover

It’s equally important to understand what these policies exclude. Trade credit insurance does not cover physical loss or damage to goods, nor does it protect against losses caused by your inability to deliver products due to internal operational issues.

Supply chain insurance, on the other hand, does not cover revenue losses resulting from a customer’s refusal or inability to pay for delivered goods. While older supply chain policies required physical damage to a supplier’s property to trigger coverage, newer policies may also address non-physical events like pandemics or political unrest.

Additionally, neither policy covers pre-existing debts or disputes. For example, trade credit insurance will not pay out on a claim if the debt is under dispute until the issue is resolved. Both policies also require an active business relationship at the time of the claim.

When to Choose Trade Credit Insurance vs. Supply Chain Insurance

If you’re deciding between trade credit insurance and supply chain insurance, it boils down to your main concern: protecting revenue or ensuring operational continuity. Trade credit insurance focuses on shielding your business from customer non-payment, while supply chain insurance addresses disruptions in your supply chain and logistics. Below, we’ll explore when each type of coverage is most effective.

When to Use Trade Credit Insurance

Trade credit insurance is ideal for businesses that extend credit to their customers, especially in situations where there’s a higher risk of non-payment. For example, exporters venturing into new markets often face risks like customer insolvency, payment defaults, or even political issues such as trade embargoes or government interventions.

This type of insurance can be customized to cover specific high-risk buyers or large accounts in your portfolio. Premiums generally range from 0.1% to 0.5% of annual sales, and this coverage can even help improve financing options by increasing your borrowing power. Providers like ARI also offer tools like tailored endorsements and pre-claim interventions to minimize risks before defaults happen.

When to Use Supply Chain Insurance

If your primary concern is avoiding operational delays, supply chain insurance is the better choice. It is particularly valuable for manufacturers or businesses with complex logistics networks. For example, a delay in essential raw materials or a supplier’s bankruptcy could bring production to a halt – this is where supply chain insurance steps in to ensure your operations stay on track.

Companies that rely on a small number of critical suppliers, operate in disaster-prone areas, or face frequent issues like port strikes or transportation delays should strongly consider this type of coverage. Beyond financial protection, these policies often support contingency planning, risk assessments, and finding alternative suppliers when disruptions occur.

Decision Table: Choosing the Right Insurance

| Business Challenge | Best Insurance Fit |

|---|---|

| High-risk export markets or new customer credit terms | Trade Credit Insurance |

| Reliance on a single critical supplier for raw materials | Supply Chain Insurance |

| Frequent logistics volatility or port disruptions | Supply Chain Insurance |

| Protecting the balance sheet against bad debt or insolvency | Trade Credit Insurance |

| Maintaining production schedules during natural disasters | Supply Chain Insurance |

| Extending open account terms to new buyers | Trade Credit Insurance |

| High dependency on specialized raw materials | Supply Chain Insurance |

| Operating in politically unstable regions | Trade Credit Insurance |

| Seeking to increase borrowing power with banks | Trade Credit Insurance |

This table helps clarify which policy fits specific challenges. Many businesses find that using both types of insurance creates a well-rounded risk management strategy. Trade credit insurance provides financial stability by safeguarding revenue, while supply chain insurance ensures resilience in production and delivery. Together, they enable your company to protect current income and maintain future operations seamlessly.

Conclusion

Protecting your business requires tailored strategies that address its specific vulnerabilities. Whether you prioritize safeguarding revenue or ensuring operational continuity, choosing the right insurance is key. Trade credit insurance (TCI) focuses on protecting your revenue by covering risks like customer defaults, insolvency, and non-payment. On the other hand, supply chain insurance secures your operations by mitigating risks tied to supplier failures, logistical challenges, and production delays.

"For credit professionals and finance leaders, TCI is more than just a safety net. It is a strategic enabler of growth and stability." – Atradius

For businesses looking to build a comprehensive risk management framework, combining both types of insurance can provide a dual layer of protection. Trade credit insurance ensures financial stability and supports market growth, while supply chain insurance keeps production and delivery on track during disruptions. With the global trade credit insurance market projected to hit $18.14 billion by 2027, growing at an annual rate of 8.6%, more companies are recognizing the importance of protecting both revenue streams and operational processes.

When it comes to trade credit insurance, having expert guidance can make all the difference. Accounts Receivable Insurance (ARI) specializes in creating customized policies, offering pre-claim support, and connecting businesses directly with global credit insurance carriers. Their brokers work as advocates, securing maximum coverage at minimal cost – usually less than 1% of your insured sales volume. With 25 years of experience in both domestic and international markets, ARI empowers businesses to confidently extend credit, secure better financing, and protect their receivables.

Take a close look at your business risks and align your insurance coverage with your most pressing threats. Whether you need to shield your finances or your operations, the right insurance plan can do more than just prevent losses – it can open doors to smarter decisions and sustainable growth.

FAQs

Can I carry both trade credit insurance and supply chain insurance?

Yes, you can have both types of coverage, as they address separate challenges. Trade credit insurance safeguards your business against losses from unpaid invoices caused by issues like customer insolvency, bankruptcy, or political events. On the other hand, supply chain insurance focuses on protecting against disruptions such as shipping delays, damaged goods, or interruptions in manufacturing.

Using both together provides a more comprehensive safety net, reducing financial and operational risks. This is especially valuable for businesses engaged in international trade or managing intricate supply chains.

What documents are needed to file a trade credit insurance claim?

To file a trade credit insurance claim, you’ll need to provide documents that show proof of non-payment or insolvency. These typically include invoices, bills of lading, and, if relevant, export licenses. It’s crucial to adhere to the policy deadlines, which are often within 180 days of the invoice date. Missing these deadlines could result in your claim being denied. Keep your records organized and submit all necessary documents promptly to make the process smoother.

How do I decide which suppliers or buyers to insure first?

When deciding which suppliers or buyers to insure first, it’s important to assess your business’s exposure to risk and how much you rely on specific customers. Here are some key considerations:

- Prioritize high-risk buyers, especially those operating in unstable regions or industries.

- If your revenue depends heavily on a small number of customers, consider insuring those key accounts to protect your cash flow.

- If your customer base is more spread out, a multi-buyer policy can help distribute risk while keeping costs manageable.

Make sure your choices align with your overall risk management strategy and long-term business objectives.