Trade credit insurance protects businesses and banks from financial risks when customers fail to pay. For banks, it turns unpaid invoices into collateral, reducing risks and increasing lending capacity. This coverage ensures banks are safeguarded against customer defaults, including insolvency or political risks, while complying with regulatory frameworks like Basel III.

Key Takeaways:

- What It Does: Protects against non-payment risks (insolvency, defaults, political issues).

- For Banks: Enables higher advance rates, includes aged/international receivables, and reduces risk-weighted assets.

- Cost: Typically below 1% of insured sales volume.

- Market Growth: Expected to reach $18.14 billion by 2027, growing at 8.6% annually.

Trade credit insurance not only mitigates financial risks but also strengthens relationships between banks and businesses, offering a secure way to manage accounts receivable.

How credit insurance providers are adapting to evolving trade finance demands

sbb-itb-2d170b0

How Trade Credit Insurance Works for Banks

How Trade Credit Insurance Works for Banks: Coverage Types, Policy Options, and Claims Process

Types of Risk Coverage

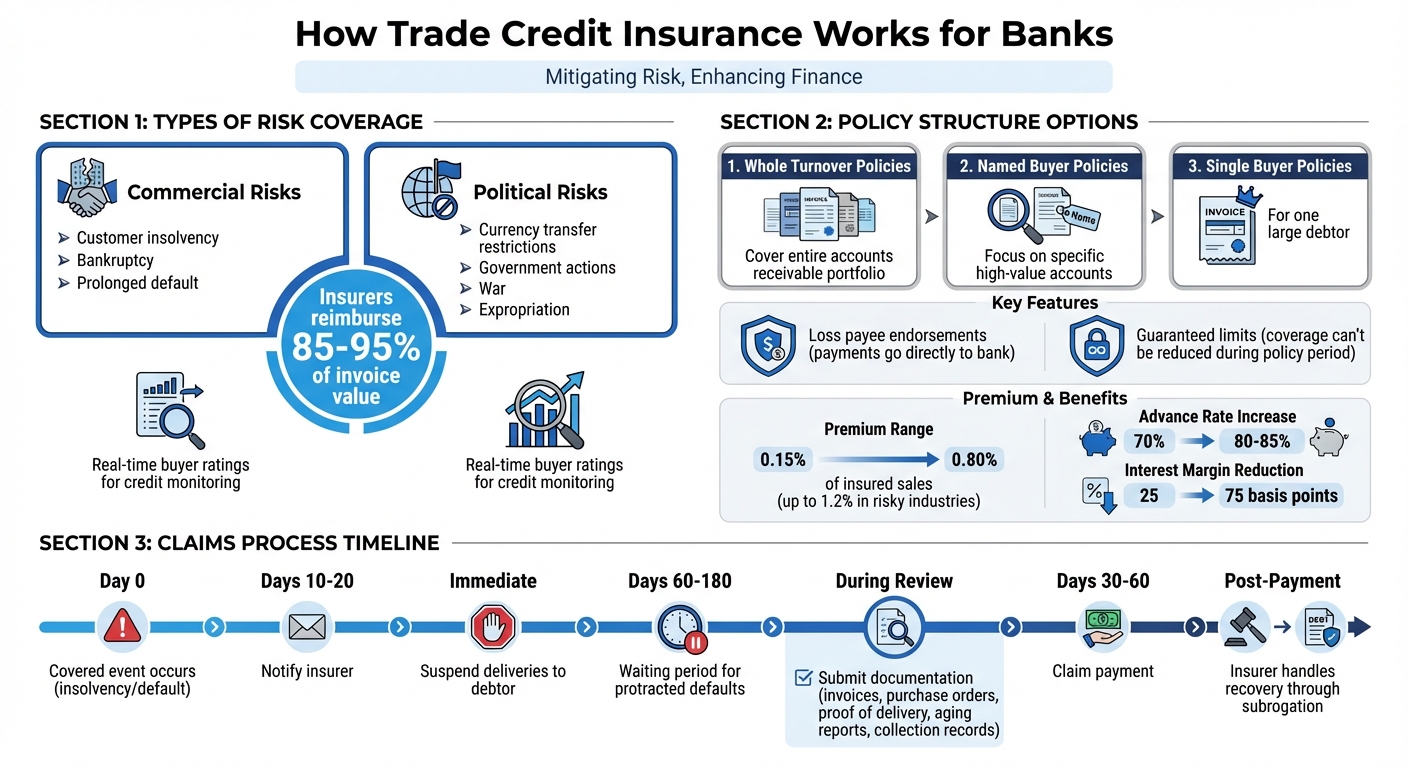

Trade credit insurance offers banks a safety net against two key types of risks: commercial risks and political risks. Commercial risks include scenarios like customer insolvency, bankruptcy, or prolonged default – basically, when a debtor fails to pay within the agreed terms. Political risks, on the other hand, are crucial for international transactions. These cover issues like currency transfer restrictions, government actions, war, or expropriation that might block payments from reaching the bank. Thanks to this coverage, cross-border receivables can be turned into assets banks feel confident lending against. In most cases, insurers reimburse between 85% and 95% of the invoice value.

Additionally, insurers provide banks with real-time buyer ratings, acting as an external credit monitoring service. This helps banks keep tabs on debtor health and adjust their lending strategies if any red flags appear.

Policy Structure and Customization Options

Banks have the flexibility to customize trade credit insurance policies based on their lending needs. Common policy structures include:

- Whole Turnover Policies: Cover an entire accounts receivable portfolio.

- Named Buyer Policies: Focus on specific high-value accounts.

- Single Buyer Policies: Ideal for situations where one large debtor dominates the relationship.

To further minimize risk, banks often opt for tailored features like loss payee endorsements, which ensure claim payments go directly to the bank instead of the borrower. Another popular provision is guaranteed limits, which prevent insurers from reducing or withdrawing coverage during the policy period – a critical factor for long-term financing.

Premiums for these policies typically range from 0.15% to 0.80% of insured sales, though in riskier industries, they can exceed 1.2%. By insuring receivables, banks can increase advance rates from around 70% to 80–85% and even lower interest margins by 25 to 75 basis points. Companies like Accounts Receivable Insurance (https://accountsreceivableinsurance.net) specialize in guiding banks through these options and connecting them with global credit insurance providers.

Once a policy is in place, understanding the claims process becomes essential.

Filing Claims: Process and Requirements

When a covered event, like insolvency, occurs, banks must notify the insurer within 10–20 days. If a debtor account becomes overdue, deliveries to the debtor should be suspended immediately.

For claims related to protracted defaults, there’s a waiting period of 60 to 180 days after the due date before finalizing the claim. During this time, the insurer evaluates the claim’s validity, requiring documentation such as invoices, purchase orders, proof of delivery, aging reports, and collection records.

Once approved, claims are paid within 30–60 days. Afterward, the insurer takes over recovery efforts through subrogation, sharing any recovered funds with the policyholder according to the policy terms. To avoid complications, banks should assign a dedicated staff member to oversee compliance with notice rules and filing deadlines, as missing these can result in denied claims.

Benefits of Trade Credit Insurance for Banks

Better Credit Risk Management

Trade credit insurance reshapes how banks manage credit exposure by allowing them to share risk with insurers rather than shouldering it entirely. This approach enables banks to support larger corporate clients without significantly increasing their own risk. It’s particularly useful when dealing with high-value accounts or industries prone to volatility.

What sets insurers apart is their access to extensive debtor monitoring tools. For example, Allianz Trade monitors around 83 million businesses worldwide. This wealth of data empowers banks with critical insights, helping them make smarter lending decisions and anticipate potential risks before they escalate. For global banks, the improved risk profiles of insured accounts receivable portfolios can also lead to capital relief on financing programs. With reduced risk exposure, banks can confidently extend credit more aggressively.

Expanding Lending Capacity

In addition to better risk management, trade credit insurance increases the collateral value of receivables. Insured receivables are viewed as reliable as insured physical assets, such as buildings. This assurance allows banks to offer higher advance rates in receivables and securitization programs, providing more liquidity to their corporate clients.

Moreover, banks can include receivables that might normally be excluded – such as international receivables, aged receivables, or accounts with high concentrations – substantially increasing the borrowing base. This expanded collateral value encourages credit underwriters to offer better terms, including higher advance rates and fewer restrictive covenants.

Stronger Client Relationships

Trade credit insurance doesn’t just mitigate risk – it also strengthens the bond between banks and their clients. By integrating trade credit insurance into their offerings, banks position themselves as strategic partners, not just lenders. They help clients tackle credit risk and plan for growth, delivering value beyond simply providing capital.

Banks can even be named as the beneficiary of a client’s policy, ensuring claim payments go directly toward covering funded invoices. This arrangement safeguards both parties and builds trust. On top of that, banks can share insights from insurers’ databases to help clients identify risky debtors before extending credit. Specialized providers, like Accounts Receivable Insurance, connect banks with a global network of credit insurance carriers, helping them navigate options and forge stronger partnerships with their clients.

Implementation Considerations for Banks

Banks looking to capitalize on the advantages of trade credit insurance must focus on practical strategies to enhance their credit risk management processes.

Selecting the Right Policy

Choosing the right trade credit insurance policy requires careful evaluation of several key factors. Policies with non-cancellable limits are particularly critical for long-term financing or securitizations. These limits ensure that insurers cannot withdraw coverage for new shipments during the policy term, providing the stability needed for borrowing bases that rely on consistent collateral values.

Indemnity levels, which typically range from 80% to 95% of the invoice amount, determine the portion of risk the bank retains. To streamline the claims process, securing a loss payee endorsement or assignment is essential. Without this, claim payments might go directly to the client, complicating recovery efforts.

The structure of the policy should align with the client’s risk profile. For instance:

- Whole Turnover policies work well for diversified portfolios.

- Named Buyer policies are ideal for clients with concentrated key accounts.

- Single Buyer policies suit large, specific projects.

Banks should collaborate with underwriting teams to ensure that policy wording meets assignment requirements. Properly implemented policies can boost advance rates from approximately 70% (uninsured) to 80–85% (insured). However, banks must balance these benefits against premium costs and the operational demands of managing the policy.

Working with Specialized Providers

Once a policy is selected, working with specialized providers becomes crucial. These providers bring expertise and access to global carrier networks, such as Allianz Trade, Atradius, and Coface, which can be difficult for banks to develop independently. Through these partnerships, banks can navigate policy options and customize solutions to meet specific client needs.

Specialized providers also assist in preparing lender-ready submissions, which often include:

- Audited financial statements

- A 12-month receivables aging report

- Top buyer exposures

- Historical bad debt data

This thorough preparation can lead to better terms and faster approvals. Some trade finance firms charge modest fees – around $500 – for reviewing submissions and crafting tailored insurance-backed proposals. This small investment can ensure the policy is structured to maximize benefits.

Staff Training and Risk Assessment Tools

Proper staff training is essential to minimize administrative errors that could lead to claim denials. Assigning a dedicated policy owner within the credit team ensures smooth management of limit requests, discretionary approvals, and overdue reporting.

It’s also critical for sales and credit teams to understand stop-shipment rules, as shipping beyond the allowed delay can void coverage. Documenting procedures for key areas – like limit requests, overdue reporting, and stop-shipment protocols – helps ensure compliance.

Jason Benson, Global Head of Structured Working Capital at J.P. Morgan, emphasizes, "Sellers should know their clients better than anybody. If a company isn’t doing its due diligence, it may be purchasing more insurance than is otherwise needed, or its insurance may be more expensive than it should be".

Integrating insurance data into the bank’s ERP system provides real-time visibility into buyer limits and receivables aging. Many modern providers offer web-based platforms, like Atradius Atrium, that enable real-time policy management, claim notifications, and tracking. Before implementation, banks should assess whether they have enough staff to handle the reporting and relationship management demands of the insurer.

Although trade credit insurance requires more oversight than standard receivables finance, its ability to mitigate risk often makes the extra effort worthwhile. With robust training and integrated systems, banks can fully harness the benefits of trade credit insurance in their daily operations.

Conclusion

Trade credit insurance has become a key tool for banks navigating today’s unpredictable market. By shifting the risk of customer non-payment to highly rated insurance providers, banks can lower their risk-weighted assets, better allocate capital, and increase their lending capacity – all while maintaining financial stability. In fact, the global trade credit insurance market, valued at $9.39 billion in 2019, is expected to grow to $18.14 billion by 2027, with an annual growth rate of 8.6%.

This approach provides tangible benefits for banks. Insured receivables allow for higher advance rates – typically 80% to 85% compared to just 70% for uninsured receivables. It also enables banks to include international receivables, aged accounts, and high-concentration exposures in their borrowing bases, expanding their lending options.

Beyond the numbers, trade credit insurance reshapes how banks interact with their clients. It positions banks as strategic allies, helping businesses stabilize their finances and confidently enter new markets. As Doug Konop, CFO of Specialty Forest Products, explained, "Having trade credit insurance allows us to have an entirely different – and much more comfortable – conversation with our financial partner".

Despite its advantages, the cost remains accessible, typically under 1% of insured sales volume. With record U.S. sales of $600 billion and global exposure reaching EUR 3.5 trillion, trade credit insurance is a vital tool for fostering growth and stability in the financial sector.

FAQs

Will trade credit insurance improve our borrowing base?

Trade credit insurance can strengthen your borrowing base by turning receivables into reliable collateral. This not only boosts your borrowing potential but can also help you negotiate better financing terms. By insuring receivables, financial institutions feel more confident lending against them, as it minimizes credit risk.

What paperwork do banks need to file a claim?

When filing a claim with a bank, it’s essential to include specific documents to ensure a smooth process. These typically include invoices, proof of delivery, signed buyer obligations, transport documents, and export licenses. Double-check that all paperwork is accurate and complete – any errors or missing information could cause unnecessary delays in processing.

How does trade credit insurance affect Basel III capital?

Trade credit insurance plays a key role for banks by helping lower the amount of capital they need to keep in reserve. By reducing credit risks, it directly influences Basel III capital requirements and calculations. This, in turn, aids banks in maintaining compliance while managing their capital more effectively.