Regional trade credit insurance safeguards businesses when customers fail to pay invoices. Here’s why it’s critical:

- Protects Cash Flow: Covers 80-95% of unpaid invoices, shielding businesses from financial losses due to insolvency, delayed payments, or political disruptions.

- Boosts Financing Options: Insured receivables are considered higher-quality collateral, leading to better borrowing terms.

- Affordable Coverage: Premiums typically range from 0.15% to 1.2% of insured turnover, making it cost-effective.

- Domestic vs. International: Domestic policies focus on local transactions, while international ones include added political risk protection, ideal for global markets.

- Customizable Policies: Tailored to business needs – covering entire receivables portfolios or specific high-risk accounts.

With the global trade credit insurance market projected to grow significantly, U.S. businesses can better manage risks, secure financing, and expand confidently in both domestic and international markets.

Trade Credit Insurance Explained

How Regional Trade Credit Insurance Coverage Works

Trade credit insurance operates through specific triggers and indemnity levels to address payment defaults. Policies activate when a buyer fails to pay due to formal insolvency, extended non-payment beyond a defined period, or political risks like currency restrictions, war, or government actions. When these situations occur, insurers typically cover 80% to 95% of the losses, helping businesses limit their financial exposure.

The framework also includes buyer limits and discretionary limits to manage risk with individual customers. Buyer limits cap the exposure allowed per customer and can be either cancellable (adjustable for new shipments) or non-cancellable (fixed for the policy period). While non-cancellable limits provide greater stability for businesses needing steady borrowing bases or extended payment terms, they tend to come at a higher cost. Discretionary limits, on the other hand, let companies approve smaller exposures without seeking the insurer’s approval.

One major advantage of trade credit insurance is that it transforms accounts receivable into secured collateral, reducing the financial impact of bad debts. Insured receivables are generally seen as higher-quality collateral by banks, often leading to advance rates of 80% to 85%, compared to roughly 70% for uninsured receivables. Insurers also rely on vast databases to assess risks; for example, Atradius monitors over 240 million companies worldwide. This extensive data analysis supports both domestic and international trade coverage strategies.

Domestic vs. International Coverage

Domestic trade credit insurance focuses on protecting sales within a business’s home country. For U.S.-based policies, this usually includes transactions with customers in the U.S., Canada, and Puerto Rico, covering commercial risks like insolvency and extended non-payment. Political risks, such as government interference or trade embargoes, are generally excluded since these are less relevant in stable domestic markets. This distinction is key for businesses looking to address region-specific risks.

International coverage, however, extends protection to foreign markets by including both commercial and political risks. Businesses operating abroad face additional challenges, such as currency restrictions, expropriation, war, or other government actions that can block payments – even when buyers are willing to pay. This dual-layer protection makes international policies more comprehensive but also more expensive due to the broader range of risks and longer payment cycles.

Adoption of these coverage types varies by region. In the U.S., private insurers predominantly offer short-term trade coverage. In contrast, European and UK markets combine private insurers with government-backed Export Credit Agencies. In emerging markets, adoption depends heavily on factors like country ratings, sanctions, and local legal systems for debt recovery. Policies such as "Whole Turnover" provide broad, cost-effective coverage, while "Single Buyer" policies help mitigate risks tied to individual customers.

Policy Customization and Tailored Solutions

Trade credit insurance policies can be customized to meet the unique needs of different businesses and industries. Customization begins with defining the scope of coverage – whether to insure an entire receivables portfolio or focus on key high-value accounts. Whole turnover policies generally offer better pricing per dollar and are easier to manage, while single-buyer policies are ideal for addressing risks tied to specific customers, though they can be more expensive. As Jason Benson, Global Head of Structured Working Capital at J.P. Morgan, emphasizes:

The policy coverage also needs to match how your business operates.

Industry-specific needs also influence customization. For instance, construction companies might require policies that address "pay when paid" clauses or progress billing, while wholesalers benefit from higher discretionary limits to streamline order approvals. Manufacturers often align "stop shipment" clauses with production timelines to avoid creating goods for buyers already in default. For international sales, factors like country ratings, sanctions, and currency controls are critical considerations.

It’s important for businesses to assign a dedicated policy manager within their credit team. This person oversees limit requests, overdue reporting, and stop-shipment rules to ensure smooth operations and prevent administrative errors that could void coverage. For companies using trade credit insurance to secure financing, it’s equally important to involve lenders early in the process. Policy wording and "loss payee" endorsements should be reviewed to align with financing agreements. As Benson advises:

Sellers should know their clients better than anybody. If a company isn’t doing its due diligence, it may be purchasing more insurance than is otherwise needed.

Increasingly, modern policies integrate with ERP systems, allowing real-time visibility of buyer limits and receivables aging for sales teams. This integration speeds up decision-making and ensures shipments align with credit limits. Accounts Receivable Insurance specializes in crafting policies tailored to meet these operational demands, offering solutions for both domestic and international markets through a broad network of credit insurance providers.

Regional Market Analysis for Trade Credit Insurance

Regional Trade Credit Insurance Market Comparison: Market Size, Growth Rates, and Coverage Preferences by Region

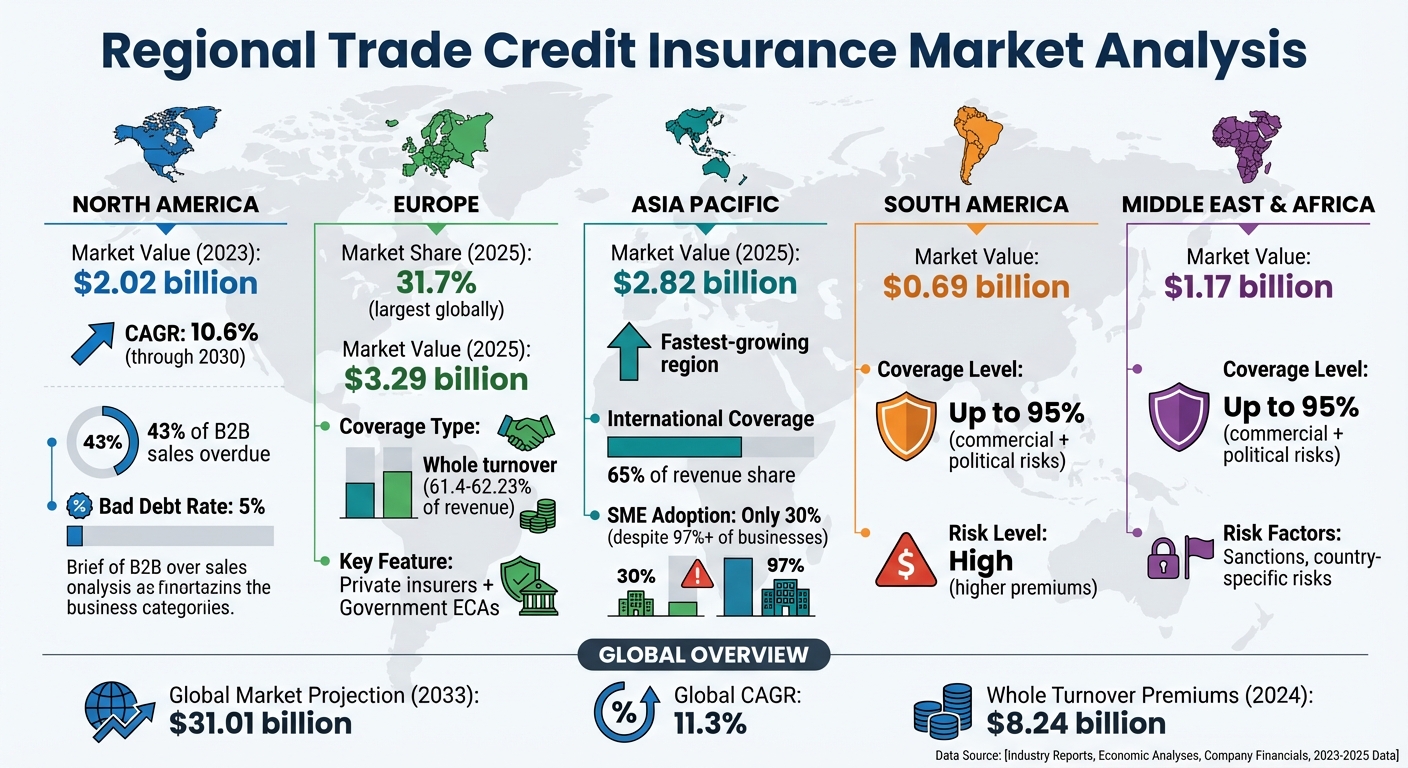

The global trade credit insurance market is projected to hit $31.01 billion by 2033, growing at an 11.3% CAGR. Economic conditions and payment risks vary by region, influencing how U.S. businesses choose to protect themselves domestically and internationally. Here’s a closer look at trends shaping major regions, starting with North America.

North America: Trends and Key Drivers

In 2023, the U.S. trade credit insurance market was valued at $2.02 billion and is expected to grow at a 10.6% CAGR through 2030. With 43% of U.S. B2B sales overdue and 5% affected by bad debts, the need for proactive risk management is clear.

The agri-food sector highlights this urgency, with 53% of U.S. firms anticipating rising insolvency risks, leading to stronger payment risk strategies. In 2023, the food and beverage industry held the largest revenue share, while the automotive sector is rapidly expanding due to risks like supply chain disruptions and plant closures. As Silvia Ungaro, Senior Advisor at Atradius, explains:

"While trade credit use is expanding, businesses remain cautious amid persistent concerns over overdue payments, bad debts and economic uncertainty."

Canada reflects similar concerns, with half of its companies expecting a worsening insolvency landscape. In the transport sector, 64% of B2B transactions are on credit. Meanwhile, in Mexico, although 45% of firms report better customer payment habits, 65% of pharmaceutical sector sales rely on credit, underscoring the need for robust protection.

Digital innovation is also driving growth in North America. For instance, Allianz Trade launched "Allianz Trade pay" in March 2024, integrating credit insurance into e-commerce checkouts. Additionally, its 2023 partnership with Flexport aimed to enhance services for U.S. clients.

Looking across the Atlantic, Europe offers a mature and diverse market landscape.

Europe: Market Trends and Coverage Preferences

Europe is set to maintain the largest global market share, reaching 31.7% by 2025. Concerns over bad debts and varying payment risks across countries drive adoption in the region. Businesses here benefit from both private insurers and government-backed Export Credit Agencies, creating a rich ecosystem of coverage options.

Key markets like the UK, Germany, and France often tailor policies to match specific trade patterns. Whole turnover coverage remains the most popular choice, contributing approximately 61.4% to 62.23% of market revenue. This approach reflects the region’s focus on comprehensive portfolio protection.

European insurers are also at the forefront of digital advancements. Coface, for example, launched an API portal in September 2023, giving financial directors access to data on over 188 million companies worldwide. This platform supports real-time credit decisions by integrating current risk assessments through 26 specialized API products.

Meanwhile, Asia Pacific presents a rapidly growing market with unique opportunities and challenges.

Asia Pacific: Growth and Emerging Opportunities

Asia Pacific is the fastest-growing region for trade credit insurance. The region’s expansion is driven by fragmented B2B payment risks and the rapid growth of corporate sectors in countries like China and India. These nations are pivotal growth engines as businesses increasingly prioritize protection against non-payment while scaling operations.

Small and medium enterprises (SMEs) in the region are adopting digital platforms and fintech solutions to streamline trade credit insurance processes. For example, in August 2025, M1xchange partnered with Tata AIG to integrate trade credit insurance into its TReDS (Trade Receivables Discounting System) platform in India, improving MSMEs’ access to secure working capital. International coverage dominates the Asia Pacific market, accounting for about 65% of revenue share.

Emerging Markets: South America and Middle East & Africa

Emerging markets face heightened insolvency risks and volatile payment conditions, making Export Credit Insurance an essential tool. In these regions, coverage often extends up to 95% of both commercial and political risks. Collaboration between Export Credit Agencies and private insurers is expanding access to protection in high-risk areas. This partnership model ensures businesses can secure coverage even in challenging markets, enabling new trade opportunities while managing risks effectively.

These regional insights provide U.S. businesses with the knowledge needed to craft tailored trade credit insurance strategies that align with their specific needs and goals.

sbb-itb-2d170b0

Regional Coverage Preferences and Comparative Analysis

Coverage preferences and premium costs for trade credit insurance vary significantly across regions, influenced by economic conditions, regulatory environments, and risk factors. For U.S. businesses, understanding these regional nuances is vital when safeguarding both domestic and international receivables.

In 2024, whole turnover coverage accounted for $8.24 billion in premiums. This type of policy, which insures an entire buyer portfolio, is designed to spread risk efficiently and offers premium rates typically ranging from 0.15% to 0.80% of insured sales. On the other hand, single buyer policies – often favored in high-risk industries or for large-scale projects – carry higher premiums, exceeding 1.2%, and are growing at a 12.0% compound annual growth rate (CAGR). These pricing structures reflect the distinct adoption patterns seen across different regions.

Regional adoption of trade credit insurance is shaped by market-specific factors. For instance:

- North America: The market is projected to reach $4.30 billion by 2025, driven by the integration of banks into factoring and supply chain finance programs.

- Europe: Expected to hit $3.29 billion in 2025, this region benefits from established credit management practices and a combination of private insurers and government-backed Export Credit Agencies (ECAs).

- Asia Pacific: With a market size of $2.82 billion, this region is experiencing the fastest growth. However, only 30% of small and medium enterprises (SMEs) – despite making up over 97% of businesses – currently use trade credit insurance.

Export coverage policies generally come with higher premiums than domestic ones, as they include political risk protection. This additional layer covers risks like currency inconvertibility, expropriation, war, and other commercial challenges. Emerging markets, such as South America ($0.69 billion) and the Middle East & Africa ($1.17 billion), face higher premiums due to tighter credit limits, sanctions, and country-specific risks. However, having an insured policy can lead to significant financial advantages, such as reducing bank financing margins by 25 to 75 basis points and increasing advance rates from 70% (uninsured) to between 80% and 85% (insured).

Large enterprises dominate the global trade credit insurance landscape, accounting for 60% of revenue in 2025, primarily due to bank requirements for insured turnover. However, the SME sector is expanding rapidly, with a 10.9% CAGR, thanks to digital platforms and fintech partnerships. A notable example is the M1xchange integration with Tata AIG in India in August 2025, which simplified access to trade credit insurance for SMEs. These digital innovations are breaking down barriers, particularly in high-growth regions where traditional insurance distribution has been limited.

For U.S. companies, recognizing these trends and regional differences is essential for developing strategies to protect receivables effectively, both at home and abroad.

Future Trends in Regional Trade Credit Insurance

The trade credit insurance landscape is evolving rapidly, shifting from reactive strategies to proactive risk management. Thanks to advancements in AI, insurers can now predict credit defaults six to eight months ahead by analyzing B2B transaction data, real-time news, and macroeconomic indicators. For instance, in 2025, AIG introduced a generative AI-powered underwriting assistant developed in collaboration with Anthropic and Palantir. This tool has significantly increased policy processing capacity without requiring additional staff. Similarly, Zurich Financial Services in Australia implemented AI solutions that reduced processing times from 22 days to nearly instantaneous.

Beyond AI, insurers are incorporating cybersecurity metrics into their risk evaluations. Cybersecurity is becoming a key factor in underwriting, as digital vulnerabilities increasingly serve as indicators of operational risks and potential defaults. Fraud detection is also advancing, with Zurich employing machine learning to identify anomalies in claims. This innovation is part of an effort to address the estimated $160 billion in potential industry-wide savings that AI-driven fraud analytics could unlock by 2032.

"AI’s ability to react to live information and make human-like decisions will accelerate the impact AI has on insurance in 2026 and beyond." – Ben Carey-Evans, Senior Insurance Analyst, GlobalData

These technological strides are particularly transformative in regions where digital integration is advancing quickly. For example, Asian markets like Singapore and Hong Kong are leading the charge with government-supported AI initiatives and regulatory sandboxes. In Brazil, the "Open Insurance" framework is enabling customers to share data across insurers via APIs, paving the way for more tailored policies and heightened competition. For U.S. businesses operating globally, these regional innovations translate to faster policy customization and more precise risk evaluations in diverse markets.

Rather than undertaking full system overhauls, the industry is leaning toward modular modernization. Insurers are focusing on targeted upgrades that integrate seamlessly with existing cloud-based systems, using Acord-compliant data standards to improve connectivity between brokers and carriers. This approach is particularly beneficial for embedded trade finance platforms, which weave insurance directly into B2B transaction workflows. As geopolitical tensions and tariff fluctuations continue to reshape global trade, trade credit insurance is increasingly seen as a critical tool for mitigating tariff-related risks.

These innovations create significant opportunities for U.S. companies to enhance their credit protection strategies. By partnering with providers like Accounts Receivable Insurance, businesses can tap into cutting-edge solutions that offer real-time adaptability – whether safeguarding domestic receivables or navigating the complexities of international trade.

Conclusion: Key Takeaways for U.S. Businesses

Trade credit insurance has grown into a vital tool for U.S. businesses, offering protection in an unpredictable economic environment where payment risks are a constant concern. It’s no longer just about minimizing losses – it’s about creating opportunities to thrive in both domestic and international markets.

The ability to customize policies is a game-changer. Whether you’re extending credit to one major client or managing a diverse portfolio across multiple regions, tailored coverage ensures you only pay for what you need. By combining this with thorough client research and using insurer-provided intelligence – like real-time data on over 240 million companies globally – businesses can make smarter credit decisions before signing contracts.

Beyond protecting against losses, trade credit insurance enhances borrowing potential by turning receivables into top-tier collateral. With coverage typically costing less than 1% of insured sales volume, and reimbursement rates of 85% to 95% for unpaid invoices, this tool provides a financial cushion that’s hard to ignore. For exporters, it also opens doors to offering competitive open account terms instead of demanding upfront payments – an edge that can make or break international deals.

In a world shaped by shifting geopolitics, tariff changes, and rapid digital advancements, U.S. businesses need to stay agile. Working with experts like Accounts Receivable Insurance ensures access to tailored solutions that align with your industry’s unique challenges and risks. Whether you’re protecting domestic receivables or venturing into emerging markets, the right policy delivers both financial security and a competitive edge.

FAQs

What is the difference between domestic and international trade credit insurance?

Domestic trade credit insurance is designed to shield businesses from non-payment risks within the United States, Canada, and Puerto Rico. It provides coverage for challenges like customer insolvency, delayed payments, or outright refusal to pay. This type of insurance helps businesses protect their accounts receivable, maintain steady cash flow, and even strengthen their borrowing power by improving collateral for lenders.

International trade credit insurance, however, goes a step further by covering sales to buyers in other countries. Beyond commercial risks, it also safeguards against political risks, such as currency restrictions, government interventions, or conflicts that could disrupt payments. Many policies also offer optional features like coverage for pre-shipment, consignment sales, or supplier pre-payments, catering to the complexities of global trade.

The key differences between the two lie in their geographic scope (domestic versus international), risk coverage (commercial risks only versus commercial and political risks), and additional options (broader features for international policies). These distinctions allow businesses to choose the coverage that aligns best with their trade operations and goals.

How does trade credit insurance help businesses secure better financing options?

Trade credit insurance transforms your accounts receivable into a dependable, low-risk asset, making it more appealing to lenders. By protecting against customer non-payment, insured receivables ensure steady cash flow. This stability allows banks and financial institutions to offer better terms – whether it’s larger credit lines, lower interest rates, or more flexible repayment options.

Providers like Accounts Receivable Insurance (ARI) assess the creditworthiness of your customers and shield you from risks such as insolvency, late payments, or even political upheavals. With this safety net, businesses can confidently extend credit to new or international clients, secure improved loan terms, and access additional working capital to support growth. By protecting receivables, trade credit insurance not only bolsters your financial standing but also opens doors to new opportunities while keeping risks in check.

What should businesses consider when customizing a trade credit insurance policy?

When setting up a trade credit insurance policy, businesses should begin by assessing their customers and geographic risks. Key considerations include a buyer’s credit history, financial health, and potential exposure to political instability. For instance, companies dealing with international clients might need policies that cover both commercial and political risks. It’s also important to determine buyer-specific coverage limits and decide whether the policy should offer flexibility, like discretionary limits, or remain fixed and non-cancellable.

Cost is another important aspect to weigh. Premiums typically fall between 0.05% and 0.6% of gross sales, influenced by factors such as the company’s industry, revenue, and loss history. Businesses should also account for deductibles, waiting periods, and optional add-ons like coverage for consignment sales or pre-payments. Finally, selecting a provider with strong underwriting expertise and reliable claims support is crucial to ensure the policy aligns with your financial objectives and risk management needs.